The sales pitch for American Express has always been that their cardholders are wealthy and thus big spenders, which in turn justifies their above-average transaction fees charged to merchants. The theory is a merchant won’t mind paying more in fees if it is offset by higher average receipts (and thus profits). This is why Tiffany & Co takes AmEx and my favorite Indian food truck does not.

The sales pitch for American Express has always been that their cardholders are wealthy and thus big spenders, which in turn justifies their above-average transaction fees charged to merchants. The theory is a merchant won’t mind paying more in fees if it is offset by higher average receipts (and thus profits). This is why Tiffany & Co takes AmEx and my favorite Indian food truck does not.

However, this recent Bloomberg article suggests that American Express is losing their millionaires because they are actually doing the math on their credit card rewards and finding the perks are better elsewhere. The title in the Businessweek magazine version is “Even Millionaires Count Their Miles“. To which I say, of course they do!

As less-affluent consumers cut spending during the recession and a 2009 law known as the CARD Act limited lenders’ ability to raise interest rates and charge late fees, banks revved up their pursuit of customers with top credit scores who pay their bills on time.

The article quotes hedge fund manager Whitney Tilson, who switched from using American Express for 30 years over to the new Barclaycard Arrival Plus World Elite MasterCard (my review). He states:

The difference between getting 1 percent and 2 percent cash back is thousands of dollars and for that amount of money, Barclaycard has a better offer […]

(I should mention that Tilson is well-known as a disciple of the Graham-Dodd-Buffett-Munger school of value investing. You would think value investors would know a good deal. 🙂 Of course, you could also flip that as the largest shareholder of American Express is… Berkshire Hathaway.)

The problem is that the American Express Platinum used to be “the” card for affluent travelers because it got you into any of the airport lounges from all major carriers. But now if you want access to all American lounges, you need the premium Citi co-branded credit card. To get access to United lounges, you need the premium co-branded Chase card. And so on. AmEx even started building their own airport lounges, but so far there are only four of them. Nowadays, unless you redeem Membership Rewards for frequent flier miles and use them wisely, it is hard to get even 1 cent of cash for 1 MR point these days. Even a plain-vanilla rewards card will pay you 1% cash back and more importantly their direct competitor Chase Ultimate Rewards will get you 1 cent back or 1.25 cents towards travel.

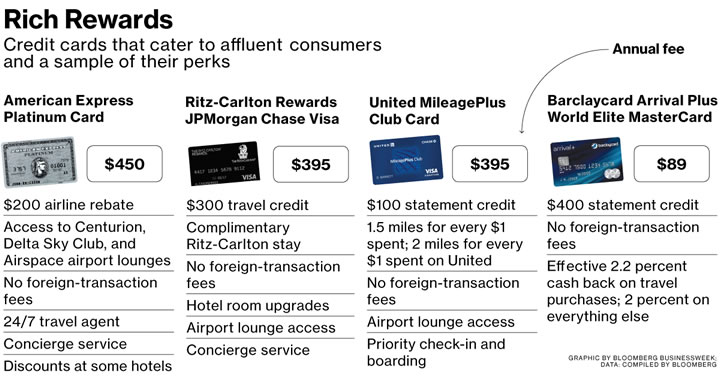

Here’s the Bloomberg graphic of credit cards that cater to “affluent consumers”:

I want to point out that the graphic is misleading because the AmEx gives a $200 travel credit every year while the Barclaycard $400 statement credit is one-time only. I do agree the Barclaycard at 2.2% back towards travel is good if you have travel charges that you redeem against, and the $400 upfront bonus counters the $89 annual fee.

Not mentioned in the article are two cards that I think are solid no-brainer cards for anyone. Both earn double the cash back from ordinary 1% cards and have no annual fee. Unless you are redeeming frequent flier miles for business class tickets or hotel points for luxury stays (which I try to do with part of my credit card rewards), it is unlikely you are getting more than 2 cents a point.

If you charged $100,000 a year, getting 2% instead of 1% would be an extra $1,000 a year back. Even if you charged $10,000 a year, that is an extra 100 bucks. You don’t need to be wealthy to appreciate simple cold, hard cash. Because there is no annual fee, I think everyone, including millionaires, should have one of these in their wallet.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I sometimes find it funny when people are surprised that millionaires want to save their money too! Thanks for sharing – this card seems like a genuinely good idea to grab.

Good observation! Completely agree! One of the main reasons they are millionaires is because they know how to save their money.

Got the Arrival card last year when they had the 40k miles after 3k spent and the double points, plus 0%. Great card. We used the hell out of it and got back about $800. We ended up putting a 17k purchase on it in addition to other purchases and trips.

My wife is going to open one this year and I moved mine down to the free card this year to avoid the annual fee (even with 30+k in spending they refused to waive the fee).

I love this card so I’m sad to hear they didn’t waive your fee (especially with that level of spending). They waived it for me last year. Hopefully they waive it again this year, otherwise I would just go ahead and cancel. The free version is not worth using.

Did you just ask them straight up to waive the fee? My approach was to just say that I want to cancel and then they sent me to the retention department, where they offered to waive.

Asked straight up as I do every year with Amex. Amex gives it to me with no fuss. I did not cancel the card yet but converted as I wanted to keep my credit utilization until after I decide if I’m going to refi our house or a rental property.

Barclays website says the $400 is travel statement credit. What does this mean?

You can apply the credit to any purchase related to travel.

You can get back $400 in travel.. hotels.. taxis.. subways..etc. I believe you choose which transactions you want to apply the $400 credit too

I just got an offer in the mail for Amex Platinum Card, if I spend 3k in the first 3 months I’ll get 100k bonus points. With the almost 500 annual fee, thats pretty much a 500 sign on bonus, but I have no use for the travel perks of the card