Nearly 30% of covered workers are now enrolled in a high-deductible health plan (HDHP). This means a lot more people are also eligible to contribute to a Health Savings Account (HSA). HSAs have the unique feature of triple-tax-free savings when used as designed:

Nearly 30% of covered workers are now enrolled in a high-deductible health plan (HDHP). This means a lot more people are also eligible to contribute to a Health Savings Account (HSA). HSAs have the unique feature of triple-tax-free savings when used as designed:

- HSA contributions are tax-deductible,

- HSA investments can grow tax-deferred, and

- HSA withdrawals are also exempt from taxes if spent on qualified medical expenses.

(Penalties: Funds withdrawn for non-healthcare expenses are taxable. If withdrawn before age 65, there is an additional 20% penalty.)

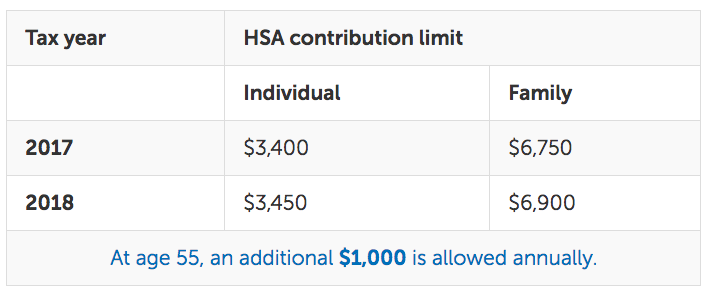

HDHPs have lower premiums in exchange for higher deductibles and higher out-of-pocket maximums. As of 2017, in order to qualify for an HSA, an HDHP must have a deductible of at least $1,300 for individual coverage or $2,600 for family coverage. Many people will use their HSA balance to cover current health expenses. However, if you can manage to pay for your current expenses out-of-pocket while also contributing to the HSA, you have the opportunity to maximize the tax advantages by investing the funds into long-term vehicles like stocks. Here are the annual contribution limits:

You can then use the future balance to pay for Medicare premiums or other eligible healthcare costs in retirement.

We personally don’t have an HDHP/HSA option from our employers, so I don’t have much first-hand experience. However, Morningstar just released an HSA research whitepaper by Leo Acheson that examined 10 of the largest HSA plan providers:

- Alliant Credit Union

- Bank of America

- BenefitWallet

- HealthSavings Administrators

- HealthEquity

- HSA Bank

- Optum Bank

- SelectAccount

- The HSA Authority

- UMB Bank

In terms of using an HSA simply as a way to grab the upfront tax break on contributions, you really just want to find an HSA provider that offers a checking account without monthly maintenance fees. Earning 0.50% APY on a $2,000 balance will earn you $10 a year, but a $4 monthly fee will cost you $48 a year. The top plans listed by Morningstar for this short-term purpose were Alliant Credit Union, SelectAccount, and The HSA Authority.

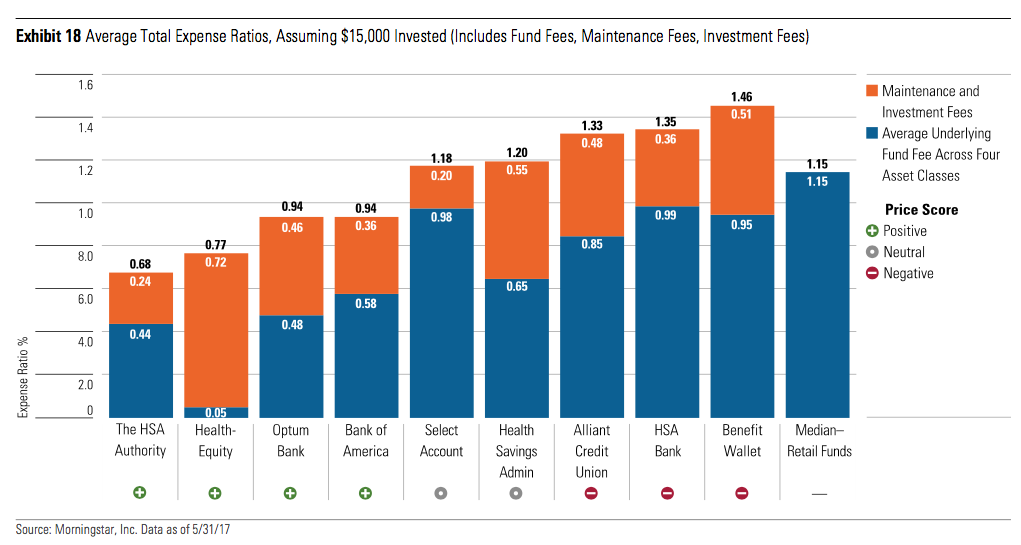

In terms of using an HSA as a portable, long-term investment vehicle (think “Healthcare IRA”), the top plans listed by Morningstar were Bank of America, HealthEquity, Optum, and The HSA Authority. However, as a firm believer in the “Costs Matter Hypothesis”, I would personally narrow it down based on the lowest overall expense ratios (underlying fund + manager fee). Here’s a chart comparing costs for a $15,000 balance (click to enlarge):

The same cost chart but for a $50,000 balance:

The two cheapest plans recommended by Morningstar are HSA Authority and HealthEquity. You can see that overall HSA costs are still higher than what you can get in a IRA or better 401(k) plan. At least the selection is pretty good. See HSA Authority investment options and HealthyEquity investment options [pdf]. Below is a sampling from the HealthEquity menu.

Keep in mind, this is not my list but what Morningstar recommends. One option not listed here is Saturna, which may make sense if you only plan on making a single lump-sum max contribution each year and buy an all-in-one Vanguard mutual fund with one transaction per year.

Please feel free to share your own experiences in the comments below.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

In my limited experience, some of these fees can vary based on your employer. My employer covers costs of setting up the account and all monthly maintenance fees. Investments are made through TD Ameritrade, and as long as I stick to commission-free ETFs, I can keep costs to a minimum.

In general how much flexibility is there in choosing an HSA administrator?

I use HSA Bank and I’m very happy. By keeping $5000 in their savings account I pay no fees. Everything above the $5000 goes into a TD Ameritrade account where I buy Vanguard ETFs commission free. The HSA Bank web site is clumsy but workable. But overall this is to me the best option.

HSA Bank allows transfer of HSA assets to a TD Ameritrade account where you can buy most Vanguard ETFs commission free. If you leave behind 5k in the HSA Bank account, there isn’t even any account fee. Not sure how any of these can beat that.

The study looks flawed. For HSA Bank, they only included the funds available in the self-directed mutual fund option with DEVENIR, which has very high fees. There is a self-directed brokerage option with TD Ameritrade which has access to all of the low-fee ETF’s and funds that was not included in the study.

“When evaluating HSA plans from an investment-vehicle standpoint, we focused on their menu of mutual funds. Some plans offer investment capabilities beyond the investment menu, such as robo-advisors that build portfolios for users, or brokerage windows. These features were outside the scope of this paper and did not influence the investment-vehicle assessments.”

+1 I use HSA bank with fee free ETF’s through a TD Ameritrade account. I think section on HSA on Bogleheads is a much better comparision of actual cost, if you are willing to use a self-directed account. I picked HSA Bank over Saturna Capital b/c I did not want to pay transaction fees and I was contributing to my HSA every paycheck. https://www.bogleheads.org/wiki/Health_savings_account

My wife has had HSA eligible options for years, we’ve built up the balance, then rolled them over into one of the recommended “low fee” providers (Health Equity). We’ve been paying eligible expenses out of pocket, keeping the receipts, planning to let the balance grow tax free for later us. However, I am starting to reconsider if it is worth the fees and hassle of yet another account. Even the “low fee” account seems to ding us with pretty regular maintenance fees in addition to high underlying expenses on the investments. In order to keep some fees lower, we still have to maintain a relatively large cash balance within the HSA so not all the money is invested. I’ve been contemplating using our built up receipts to cash out the HSA, and just keep the money invested in a taxable accounts. If we are holding a relatively efficient index fund, I don’t think there will be a huge tax hits. Dividends are manageable , and capital gains can be deferred until later. More than anything, I’m at the point that I want less accounts, not more, unless there is a HUGE advantage.

The Saturna account you listed is interesting, so I will look into that. Thank you.

At HealthEquity, the admin fee actually is waived if the cash balance and the investment balance combined is over $2,500. So if you wanted to keep $2,000 in the balance account and invest $5,000, then the admin fee will be waived!

I think that Saturna is probably the best HSA for long-term investors. It requires a ton of forms to be filled in, mailed in etc. Too much paper pushing is a turn off. The annual cost will be something like $15-$25/year.

I would think Select Account is a second best, particularly if you want to also have the option of using the money for health expenses ( the Morn study disagrees, but I think it is flawed). It looks like the SelectAccount would charge you $12/year for the HSA account and $18/year for the investment account, for a total of $30/year. The lowest cost fund for the menu is VFIAX on S&P 500 at 0.04%/year. I would say that is pretty neat.

I am using HealthEquity for the employer match, and frankly, paying 0.40%/year on the investment front seems like too much.

Another think to consider is that if your employer can automatically deduct your HSA contributions from your payroll into the HSA they recommend, you don’t pay FICA tax on that income. That is a 7.65% return from the get go. While unfortunately my company doesn’t match HSA contributions, I know some do. If your company matches, between a 7.65% savings on FICA, and the match, and the triple tax advantage, there is definitely an argument to be made that HSA should be your first priority to invest in assuming you have good investment options within your employer-sponsored HSA provider. (Make sure to save all your receipts whenever you pay cash out of pocket for health expenses in the meantime in order to ensure that you can pull as much of your money out tax-free as possible whenever you need it… there is no year restriction on how old receipts can be to have a tax-free withdrawal)

Even if the fees are a little higher than those in a HSA you could open on your own outside your company, the 7.65% annual FICA tax break might make it worth it to stick with your employer-sponsored plan. A simple math equation to figure out which would be better would be in most scenarios would be .0765 / (difference in fees & expense ratios between outside HSA provider and company sponsored provider) = number of years it takes for fees & expenses to matter more than the FICA tax break. From there, you have to determine if the breakeven number of years if greater or less than the amount of years until you are going to pull it out (65 at earliest, but it could be later if you want).

If you want to get real frugal, you are allowed one rollover a year (full or partial). So in theory, every year, you could roll over all your funds that you saved 7.65% from your employer sponsored provider into the low-cost HSA provider you chose on your own. You do need to consider though both the opportunity cost of how long you will be out of the market during this rollover and if the nuisance of doing so is worth the little bit of extra money.

Just some food for thought.

I was thinking the same thing about avoiding FICA if you use your employer-sponsored HSA, so long as they do direct deductions from your paycheck. In many cases (like mine), the employer also covers the account fees. You make the point that you can take out money any time so long as you have the receipts to match and haven’t otherwise been reimbursed for the expenses, but also keep in mind that if you have claimed any of those expenses as deductible (i.e., if you have more than 7.5% of your income as medical expenses in some year), you cannot also reimburse for them from your HSA. Also, you can only do this for expenses that occurred after the start of your first HDHP.

Due to change of employers and change of medical plans, I find that if I am not on an employer sponsored HDHP plan, these HSA accounts start charging maintenance fees, fees can be high especially for low balances. Anyway to avoid the monthly maintenance fees? Or any recommendations for no-fee HSA?

I’m with Adam, an HSA Bank account linked to TD Ameritrade HSA brokerage account is a great option if you want to set up a “Healthcare IRA”. I’m cash heavy in these accounts, but it is nice to have a lot of flexibility in the Ameritrade account.

In regards to the related topic of whether or not to immediately reimburse yourself for medical expenses or to delay reimbursement to allow funds to grow tax-free, I have come up with some reasons why I am leaning towards going ahead and reimbursing myself. I would love your guy’s take on this:

1. As you mentioned, HSA fees are expensive. Health Equity charges me 0.40% annual fee on my invested HSA. Investing in the VTI ETF would cost me 0.05% per year.

2. Despite the fees, yes, you would likely still end up with more total dollars at retirement if you delay reimbursement. HOWEVER, a much bigger chunk of money would be restricted to medical expenses.

If you delay reimbursement, only what you can withdrawal from past medical expenses are truly liquid dollars that can then be spent on anything. All the rest is restricted to medical expenses (including all this tax free compounded growth).

If you instead immediately reimburse yourself for medical expenses and invest that money in a brokerage account, that money can compound grow and be used for anything at retirement. Yes, you would lose out on some tax savings, but the liquidity difference needs to be taken into account here.

3. Per some quick spreadsheet calcs, I think you could easily get into a scenario where by delaying reimbursement, you could easily accumulate way more dollars that are restricted to medical expenses beyond what you could possibly ever use.

4. Tax laws around HSAs could easily change with no grandfathering of being able to reimburse past year’s medical expenses.

5. Who wants to try to keep track of receipts for decades? Digital copies may make this a little easier, but still, it’s a hassle.

1. Doing the math .15 (capital gains rate) / .0035 (difference in the fees you mentioned above) = about 43 years. Therefore, from a pure mathematical standpoint, if you’d pull the money out in less than 43 years, you’d be better off in HSA, more than 43 years, you’d be better off in the VTI ETF. (Note that this calculation is excluding the 7.65% FICA benefit mentioned above as I’m assuming you are investing this money once being “reimbursed” for health expenses from your HSA and then moving them into a brokerage. If you aren’t doing that, (i.e. you’re just taking the money from your paycheck and investing in VTI ETF versus ever putting into HSA) the same math would result in about a 61 year breakeven.)

2. And I agree with your point, but once you reach 65, you can withdraw the money and pay tax then, essentially turning your HSA into a traditional IRA but with no mandatory withdrawals. Further, if God forbid something major medically happen to you, it would obviously be very advantageous to have had it in the HSA and get that triple tax benefit. So, obviously hoping that nothing will ever happen tragically that would bust through a lot of your HSA funds, you still basically had an additional 3400 or so (for an individual) every year that you could keep tax advantaged from capital gains plus if you are lucky enough to get an employer match you are increasing free money plus you get the extra 7.65% FICA benefit not found in any other investment vehicle.

3. See above.

4. True, but I’d hope (and expect… though Congress’ competence does not inspire confidence) that there would be a specific time period to cash all remaining outstanding receipts. If not, I for one would be raising a storm. But, you are correct this is a risk that one ought to consider.

5. Agreed and fair point. You have to ask yourself if your time is worth the marginal benefit of doing so. But I could counter and argue that reimbursing all expenses immediately requires more time since you’d be having to file receipts reimbursements requests every time something comes up versus just stuffing everything in a drawer (preferably fireproof haha) or through a digital scanner. (Admittedly, this is only true if your HSA provider does not provide checks or a debit card you can use, so this might be a mute point…even it is, I still think some people will find the extra worth the extra tax benefit. Plus, side point, for expensive medical procedures, if you can put on a rewards credit card to earn points/cashback, it might make sense to do a reimbursement form instead of paying with the HSA provider’s debit card or checks.) Then, you can pay some college or high school kid who needs a little extra cash to add up all your receipts while sip mojitos on the beach thinking about that extra 15% you have from not paying capital gains tax.

You bring up good points, and it’s definitely not for everybody, especially for someone who values simplicity or automation, though my guess is the majority of those people who value those two things to the extreme aren’t readers of this site. Maybe when I’m a little bit older and/or make more income, I will stop doing this, bur for now my strategy is HSA IRA.

I do contribute into my HSA through my paycheck, so I do get the FICA tax savings.

I get that you could withdrawal from your HSA for non-medical reasons and pay the income taxes if you end up having more money than you can use for medical reasons or if you just need the liquidity, but I don’t think that would be financially savvy. I still think it makes more sense to get the majority of the compound investment growth through a non-HSA account. Then, the bulk of your money in this situation is in a fully liquid account that is not taxable for non-medical expenses.

To throw some numbers around this (from some spreadsheet calcs…), assuming an 8% return, 0.40% investment fees for HSA, 0.05% investment fees for brokerage, 15% capital gains tax, $6,750 in contributions in 2017 (family coverage) and $5,000 in expenses in 2017 with each of these amounts growing 3% annually, after 30 years, on a pure dollar basis, delayed reimbursement nets you $1,038k while immediate reimbursement nets you $947k. So on a pure dollar basis, delayed reimbursement gains you $91k from the tax savings. But the problem is, of the $1,038k in the delayed reimbursement scenario, $238k is liquid (being able reimburse from the last 30 years of medical expenses) and a whopping $801k is stuck in the HSA, either to be used for future medical expenses or withdrawn and having to pay income taxes on it (yuck). Of the $947k from the immediate reimbursement scenario, $623k is liquid (withdrawing as the past 30 years of medical expenses have happened and letting that money compound grow taking into account the capital gains tax implications) and just $324k is stuck in the HSA.

As far as the possibility of having large, unforeseen medical costs, that is a valid point. But most health plans have an out of pocket maximum, so hopefully any huge health expenses would be mitigated.

Hi Jonathan,

This is a well-researched article. But the only think that I can think of, HSA is not perfect as it seems. And the only thing that struck me in this post, was the Saturna you’ve posted. It provides us option.

Nick, Great point. I think I will start doing that; I’ve never considered that third option. Genius. Using an HSA as I described except redeeming receipts right away is genius assuming you are immediately putting that money into a Brokerage account (i.e. keeping it invested). Then, you are only paying capital gains tax on the earnings and not income tax rates. This would definitely work out better for you assuming you aren’t going to day trade with the funds and will have long-term capital gains. Thanks for the tip.

I have no experience with HSAs either and have read this article and these posts in terms of my general interest in all things investment related. With that in mind, I’m going to express an opinion that is probably unpopular in light of the comments I’m seeing here. It seems to me that the primary purpose of an HSA should indeed be covering anticipated and emergency health care expenses not covered by insurance. Although my memory is fuzzy on the issue, it seems to that the creation of HSAs was a response on the part of policy makers to address healthcare and insurance costs for those workers who did not have the best of coverage. That the investment industry — and many consumers — have seized upon HSAs as way to bring more assets under management and offer another tax-advantaged investment option seems to be a matter of things gone awry. Indeed, the tactic talked about in the article — pay for healthcare expense out of pocket so as to keep HSA assets growing — suggests this has become a product for those with an investment perspective rather actually needing for healthcare expenses. Granted, the assets may eventually be withdrawn to cover medical expenses, but I would say these are the types of consumers who have saved these assets anyway in some other type of investment account. I suppose I can’t fault anyone for taking advantage of tax-savings options they have available, but I would not be surprised that if at some point in the future policy makers or regulators take a second look at this product and rein it in — possibly requiring actual distributions for healthcare expenses every year, restricting contributions for certain balance size accounts, etc.

HSA Authority (ONB) – I’ve been trying to establish the account and 2017 deposits. It’s one hurdle after another…..deposits coming out of the source bank almost immediately but not cleared at HSA Authority for weeks. Max mobile deposit of 2000 and then the max changes to 1000 without notice AFTER the first couple check amounts finally become available. Want to open the account – you’ll need to get a form notarized first. I read everything on their site before opening the account and not one of the frustrating and antiquated processes was mentioned. My mistake was thinking they operated the same as any other financial institution. When I used customer support to ask how I might have been able to tell this was going to be such a hassle I was told…”None of these processes are discussed or made known on the web site” so their is no way to know what you’re up against until the process is underway and you can’t cancel/close the account or return the money to the source institution without paying a penalty as well as making your taxes and financials overly complicated. Steer clear…if this is how hard it is to start up the account I can only imagine the frustration at trying to use it. I’m planning on funding the account for 2017 just so I can file my taxes and close it. It’ll be worth paying the penalty.