There is a lot of uncertainty in investing, and it always seems like especially now. Buy and hold has been called dead many times. However, if you look carefully, you’ll find that there are many people who have quietly grown their portfolio over the last decade using the boring principles of diversification, low-costs, and regular rebalancing. I would also add proper tax planning helps as well.

Here is some data from a WSJ article by Burton Malkiel (author of Random Walk Down Wall Street) that helps illustrates this. (Can’t view the article? Use this Google the title trick and click the first link.) The article is from several months ago, but the S&P 500 index back then was almost exactly the same as yesterday: 1,193 vs. 1,195.

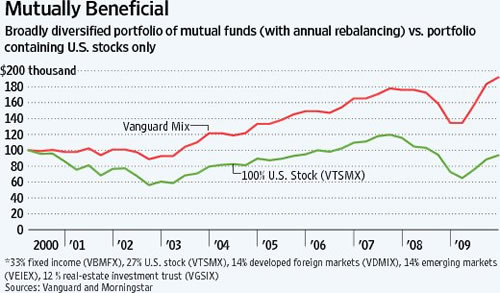

The chart below shows the growth of $100,000 invested at the start of 2000 until the end of 2009. As you can see, a 100% stock investment (in green) would have ended up at $93,717. Thus the term “lost decade for stocks”.

But what happens when you mix in some other assets, and rebalanced them annually? The red line is a portfolio consisting of 67% stocks and 33% bonds, all in low-cost index funds. The stock breakdown was 27% US, 14% Developed International, 14% Emerging Markets, and 12% REITs. The result was a ending balance of $191,859, which means an investor in 2000 could have, without special psychic powers, nearly doubled their portfolio over the same “lost decade”.

The diversified portfolio above matches rather well with my own asset allocation. For one, my AA also has 50/50 US/non-US split plus a chunk in REITs. Although I started out 85% stocks/15% bonds, I am now closer to 75% stocks. I have also rebalanced annually to maintain that ratio, but I do feel that my portfolio has still grown past my contributions even though I haven’t tracked my personal returns as well as I’d like.

Regular rebalancing is key. That is, keeping your target asset allocation by buying what is going down, and selling what is going up, in order to keep your desired risk profile. Both in early 2009 and last week, I was buying stocks. While there is debate on this, I believe that there is a reversion-to-the-mean effect that boosts your returns.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Have you tried tracking your portfolio with Mint? It will compare the growth of your portfolio with that of certain indices such as the S&P 500. (But I am not sure how “smart” it is in terms of tracking growth vs. contributions, etc)

Wow…I have a ROTH IRA all in cash at the moment. This has convinced me to get back into the market. I never understood the power of re-balancing, truly, until now…I don’t want SUPER returns, just stable ones until I retire. Thanks!

For some reason I can only read the first paragraph of the article (even with the google trick). But something seems very fishy about the above graph.

The part that really looks wrong to me is 2009-2010… a very good year for stocks. Now I can understand why the vanguard mix made more money that year… it had about twice as much money to begin with.

What I can’t understand is how the vanguard mix (by my rough calculations looking at your graph) seemed to do percentagely better too! What was their mix composed of that those bonds somehow scored better than pure stocks in 2009? This graph seems to suggest that there pretty much was never a time at all in the last 10 years where stocks did better than bonds since the spread between the two is almost always growing.

Also what happened in late 2000 that stocks got pummeled but the vanguard mix didn’t go down at all?

What am I missing?

I like the idea of rebalancing, but the whole premise is based upon an exploitation of a reversion to the mean. Stocks do particularly well one year, bonds do particularly poorly, so you sell stocks, buy bonds. The correlation between stocks and bonds is low-ish, so I guess this works.

The reversion to the mean part of the strategy has always perplexed me. Aren’t we inherently assuming exploitable inefficiencies in the market? In the example above, we’re assuming that we can exploit a temporary overpricing of stocks to buy temporarily underpriced bonds. It’s this portion of the argument that I fail to wrap my head around.

Maybe I should stop over-analyzing, face the music, and jump on the rebalancing bandwagon. Who am I to say that Malkiel is wrong when the data obviously support him?

David–

International and emerging markets equities are part of the answer why the red line did better than the green line in 2009. The Russell 3000 was up 28.3% in 2009, definitely a good year. EAFE was +31.8% and the MSCI Emerging Markets index was up 78.5%.

@David – The chart actually only runs until the end of 2009. 2010 isn’t even included. I don’t have the specifics, but check out the Callan Periodic Table of Returns on the bottom of this post:

https://www.mymoneyblog.com/2010-investment-returns-by-asset-class.html

In 2000, bonds went up 12%, and the S&P 500 went down 9%.

In 2001, bonds went up 8.5%, and the S&P 500 went down 11.7%.

For much of the decade, REITS were also doing quite well (obviously not 2008 and 2009). Emerging Markets also did well at times, as Andy mentions.

@Baughman – To me, I had to reconcile the fact that efficient markets doesn’t mean there aren’t asset bubbles. I don’t believe in perfectly efficient markets, but they are efficient enough that you can’t just read some 200 page book and make money. Efficient markets means you can’t time them. Look how many smart people lost money in 2008 and 2009. Even though every other person you meet will claim “it was obvious”.

full disclosure – I rebalance with +/- 5%/25% bands

that said, I do it for risk management, and take any ‘rebalancing bonus’ as a nicve surprise.

the reality is that there really is not or should not be a debate about reversion to the mean. the debate is about the time perod over which that reversion would be expected to occur, and of curse, what that’ mean’ truly is or should be.

if the reversion to the mean occurs over longer than your ‘safe’ investing timeline, rebalancing will hurt you, net-net, especially if you hit liquidation threshold/capitulation pricing. of course, you should have determined that first with your AA and risk tolerance and kept it out of the realm of possible outcomes.

if reverson to the mean occurs over a shorter time perod than your investing horizon, it should virtually always provide a ‘bonus.’

the debate is about the timeline relative to your investing timeline. The NASDAQ for instance, is still at about 1/2 of its all time high (again, its a sector, but some say REITs are sector – ful disclosure I have 10% REITs in my AA). Rebalancing into the NASDAQ faithfully, using a rebalancing system, for instance, would have led to larger losses than otherwise.

thus, risk control first, rebalancing bonus maybe, and second…

I rebalanced three times during the 2008-9 crash. Just rebalanced again last week. Unfortunately, I picked the Tuesday that everything shot back up. I thought I was safe at 3 pm with my bond funds still ahead of most stock funds and I placed my exchange orders for my index funds. Then somebody of some importance had to make a stupid announcement that rates would stay low for two years, and the stock funds I was rebalancing back into ended the day up 5-7%, erasing all the losses of the day before. Dang volatility!

Have you ever looked at savings-bond-advisor.com’s i-bond vs. the Vanguard 500 chart? Is it accurate in your estimation? If it is, I think I’m done investing in stocks outside of tax-protected retirement accounts.

Instead of always rebalancing; shouldn’t regular period investment produce dollar cost averaging and have the same effect? Most of my funds are in taxable accounts and hence I shy from rebalancing?

I’ve long believed that sticking to your strategy will grow your portfolio over time. The people that lose the most in the stock market are the ones who panic and pull out when the headlines say the market is bad.

I’ve pretty much lost faith in the “free market” for the moment. When the market starts to tank every time the quantitative easing cash runs out that says to me that the market is on life support. Fundamentally owning portions of many companies is a good idea but if the whole game is being rigged then I see no way to win.

I’m personally taking a hiatus from the market for awhile. I still think owning individual stocks can be a good idea if you know what you’re doing or have the money to pay people to know what they’re doing to share. I think the market is due for a major correction and I don’t want to be anywhere near it when it does.

Rebalancing your portfolio regularly is a very simple principle to grow your savings. My experience is that you can get even better results when you also rebalance when you get an objective indication that the long-trend in the asset classes that you are investing in has just changed direction.

Adjusting your asset allocation after these trend changes could provide even higher returns.

With today’s volatile market it is anyone’s guess which direction things will go in which is why that beautiful word “diversification” is even more important now than ever before.

It’s good to know good asset allocation helps you. Slow and steady wins the race.