Update: Schwab has suspended/ended this “Up to $6,000” transfer promotion as of October 2024. The referral offer appears to still be available, which is up to $1,000.

Brokerage firms constantly compete for “assets under management”, and many are willing to give you cash to move over your existing portfolio from your existing broker over to them. Unfortunately, many of these offers are for new app startups with questionable customer service. How about a traditional firm with telephones connected to knowledgable humans working inside physical branches in major metro areas?

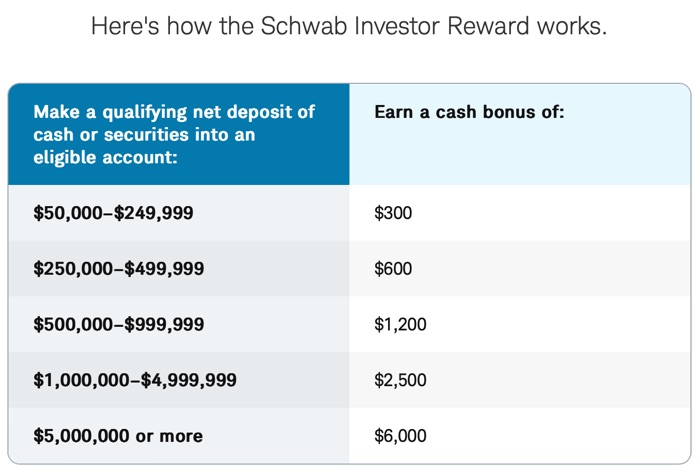

Charles Schwab is currently offering up to a $6,000 cash bonus depending the value of assets that you move over (qualifying net deposit of cash or securities) within 45 days of enrollment. The minimum hold period is one year for taxable brokerage accounts. The percentages aren’t the best, and the tiers are relatively high, but this is actually a brokerage I wouldn’t mind leaving my assets at for the long run. It’s also available to existing Schwab customers.

- $200 with $50,000–$99,999 in new assets

- $300 with $100,000–$249,999 in new assets

- $600 with $250,000–$499,999 in new assets

- $1,200 with $500,000–$999,999 in new assets

- $2,500 with $1,000,000-$4,999,999 in new assets

- $6,000 with $5,000,000+ in new assets

Note: New-to-Schwab clients should compare this with the Schwab Referral Offer, which may offer a slightly higher bonus at specific asset levels (ex. $100 bonus on $25k in new assets, $300 bonus on $50k in new assets, $500 bonus on $100k in new assets). At the higher tiers, the offer above is better. That’s my referral link, thanks if you use it (although please let me know if you have issues with it; I’ve never actually gotten a bonus from Schwab so I’m not sure if it really works).

The easiest option is often to perform an in-kind ACAT transfer of existing securities, which takes less than a week and all of your tax basis information should also move over after another few days. Your old broker may charge you an outgoing ACAT fee about about $75, although you should ask Schwab if they will reimburse you for

this fee.

Both taxable and IRA accounts are eligible. From the fine print and FAQ:

Accounts that are eligible for the Schwab Investor Reward include: Schwab retail brokerage accounts and individual retirement accounts (IRAs), including accounts enrolled in Schwab-sponsored investment advisory programs such as Schwab Intelligent Portfolios®, Schwab Managed Portfolios™, Schwab Managed Account Select®, Schwab Managed Account Connection®, and Schwab Wealth Advisory™.

Schwab Bank Investor Checking™ accounts do not qualify for this promotion whether they are linked to a brokerage or are stand-alone. If you make a deposit in a Schwab Bank Investor Checking™ account, you will not receive the award. The offer also does not apply to the Schwab Global Account™, ERISA-covered retirement plans, certain tax-qualified retirement plans and accounts, education savings accounts, Schwab Bank accounts, or accounts managed by independent investment advisors.

Can two clients in the same home get the award?

Yes. As long as both clients have individual accounts and separately qualify for the Reward, provided that each makes a qualifying net deposit.

Schwab appears to still be offering their $101 Starter Kit promo. But the FAQ says “Can this offer be combined with other offers? No. This offer can’t be combined with other offers.” I’m not sure if it counts as combining if you first open the new account for the Starter Kit bonus, wait, and then participate in this transfer offer.

One major drawback with Schwab is that the default cash sweep is not good. Still just 0.48% APY as of 7/16/24! Boo. You need to take proactive steps to avoid lost interest if you plan to keep significant amounts of cash in their default sweep account. Consider buying Treasury bills, brokered CDs, or Treasury Bill ETFs like GBIL (still possible to lose value). See my separate post on the best alternative Schwab cash sweep options.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Is there a similar bonus for new money deposit for existing accounts? I have an account created for work but I can pull in personal funds to meet the bonus.

Jonathan, I’m confused when you say “I will get a referral bounty as well, so thanks if you use it.” When I look at the bonus FAQ’s for this I see the following:

“Who gets the Bonus Award, and when do they get it?

The Bonus Award goes to the referred new client when they make a qualifying net deposit within 45 days of opening an eligible account and becoming a Schwab client. We’ll deposit up to $1,000 in their account about a week after the 45-day qualification period.”

It does not say anything about a bonus also going to the referring current client. Is there something I’m missing?

Schwab is fantastic, but alas, I am already there. Wish there was some bonus for bringing in new money to these places. I feel like Marcus is one of the few that consistently offers existing clients bonuses for bringing in cash.

Does anyone have experience with both Schwab and Fidelity? I know they’re both acceptable, but I’m trying to decide if I should consolidate an account at Fidelity or try out Schwab.

In case anyone else was curious, I decided against Schwab due to their practice of accepting payment for order flow.

3 years ago before I retired I tried all of the big 3 platforms and I am so glad I did. You can buy any funds on any platform so that is not even a concern. But I chose Fidelity because the platform is so easy to use to buy and trade. Also their retirement software is free to use and is just as good as those you have to pay for. Plus once you get set up you can meet on the phone with a CFP for free. Now 3 years later I am so happy with that decision to go with Fidelity. I only have 1 Fidelity fund and a few funds with Schwab and 1 with Vanguard……….all on the Fidelity platform. There are a host of other reasons as well. You just have to get on there and try it out. You can open an account with them and just not fund it……that way you can have all the benefits of Fidelity……..sort of a test drive.

hi, do you have a current referral code you can share? the posted link has since expired. thx

I called Schwab and they said they are having some technical difficulties and recommended to proceed with your application and then call them to apply the referral code “REFERAAFETFRZ” in the link manually.

after speaking in their web chat I was referred to local branch – after they reached out to me and I provided links to competitor offer they said yes to matching Citi wealth management on for one of the higher tiers, which is better than one in this post. Please reach out locally to see if they can incentivize you better.

Your last paragraph is the best reason for NOT using Schwab. They are stealing money from unknowing customers by so generously giving them a whopping 0.48% yield on idle cash. Whereas my idle cash at Fidelity is automatically invested in SPAXX (Federal Government money market) that yields 4.97% as of today (7/26/24). Enough said.

There’s a pretty easy solution to that, which is to not keep cash in the account…

To each his or her own, but I purposely avoid doing business with businesses that obviously don’t care a hoot if their customers get a square deal. It would be easy for Schwab to fix this inequity, and they might even attract more business if they did. To me, it signals poor management and the public be damned.

And as to why I keep idle cash at Fidelity, it’s in a checking account in my brokerage account earning nearly 5% – a checking account that I use to pay all of my regular bills. How many tens of millions of people keep idle cash in checking account at Bank of America or Citi Bank or whatever large bank where it earns exactly nothing, zip, zero, zilch. So my cash is hardly idle.

Excellent response David. Fact is that Schwab generates most of its profits from its cash (sweep) account (where so little interest is paid). All transactions settle in that account, which Schwab is quick to exploit. In contrast, Fidelity’s sweep (core) account pays a competitive money mkt interest rate (they don’t try to nickel and dime their customers – unlike Schwab). Great article in Barron’s (bout a year or so ago) exposed just how cheap Schwab was being in this manner.

Recent chat with Schwab rep says bonus is no longer available.

Thanks for the update.