There used to be a series of ING commercials where people would carry around their “Number”, which was usually over a million dollars. I think such large numbers actually discourage most savers, so what if we had an alternative goal that was both more achievable yet realistic?

I’m currently reading a new book called Charlie Munger: The Complete Investor by Tren Griffin because, well, I like to read anything about Charlie Munger. There is a lot of good stuff related to investing inside, but it didn’t mention one of my favorite personal finance quotes from Mr. Munger. I can’t seem to find an exact reference anymore, so here are two paraphrased sources…

First, here is an excerpt from the 2003 book Damn Right!: Behind the Scenes with Berkshire Hathaway Billionaire Charlie Munger by Janet Lowe (my review):

Munger has said that accumulating the first $100,000 from a standing start, with no seed money, is the most difficult part of building wealth. Making the first million was the next big hurdle. To do that a person must consistently underspend his income. Getting wealthy, he explains, is like rolling a snowball. It helps to start on top of a long hill—start early and try to roll that snowball for a very long time. It helps to live a long life.

Second, here is another version of the quote credit to Munger, per Conservative Income Investor:

“The first $100,000 is a bitch, but you gotta do it. I don’t care what you have to do—if it means walking everywhere and not eating anything that wasn’t purchased with a coupon, find a way to get your hands on $100,000. After that, you can ease off the gas a little bit.”

$100,000 is certainly a nice, round number. But is it a worthy goal? Consider these points:

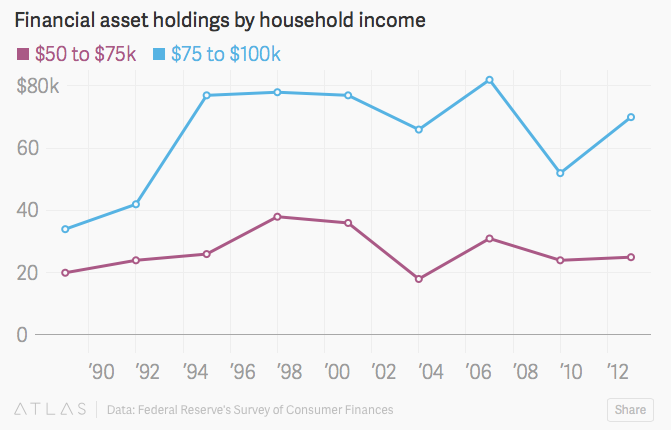

Most people will never achieve $100k in portfolio assets. Forget a million bucks. Consider this chart from the Quartz article America is full of high-earning poor people. On average, even a person earning close to six figures will struggle to reach $100k in financial assets by age 55.

The figure below plots financial assets held by the upper middle class (household income from $50,000 to $75,000, and $75,000 to $100,000) aged 40 to 55. Financial assets are any assets a household owns that isn’t a house, car, or business, which means it includes all retirement funds.

If you reach $100k quickly, that means you have high earning power. Let’s say you start a successful small business or are in a well-paid professional field. Well, you have the saving potential to reach the millionaire level, you just have to keep it by not increasing your spending accordingly.

If you reach $100k gradually, that means you have built up a strong habit of spending less than you earn. Let’s say it takes you a decade of steady saving to reach $100k. That’s okay, as you’ve shown that have both consistent earning power and spending restraint. You’ll be able to save another $100k over the next decade for sure, meanwhile your first $100k is going to keep on growing.

At the $100,000 level, compound interest become significant. At 5% return, your $100,000 will grow by $5,000 in just one year. That’s $5,000 for doing nothing but waiting around for a year. The year after that, you won’t just have another $5,000. You’ll have $5,250 due to compound interest. At the end of five years, that $100k is already $127,628.

Add in the additional money from your continuing habit of saving, and things start to improve quickly. Your snowball is growing. I no longer automatically reinvest my dividends from my taxable mutual fund and ETF holdings because I love seeing the money show up in my cash account. A few clicks and I’ll reinvest them, but I like the feeling of “cashing my dividend checks” and knowing that one day I’ll be waiting for them to arrive instead of my paycheck.

Now, I still think savings rate is a better measuring stick than portfolio size, because someone who can earn $60k and spend $30k every year is going to be able to retire much sooner than someone who earns $180k and is stuck in a lifestyle spending $150k. But if you are in the phase of your life where you love watching your account balances grow every day, even by a few dollars (been there, done that), $100k is the biggest goal you need.

Related: Munger: Work For Yourself An Hour Each Day and Munger on Parenting and Childhood.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

There’s a few places here that has left me scratching my head — this statement alone:

“The figure below plots financial assets held by the upper middle class (household income from $50,000 to $75,000, and $75,000 to $100,000) aged 40 to 55. Financial assets are any assets a household owns that isn’t a house, car, or business, which means it includes all retirement funds.”

First of all I am happy I have achieved upper middle classdom, but I don’t think I really have (these salary ranges look pretty low for that, don’t you think?). And, is he saying that Most People with never achieve $100K in assets, including what’s in your retirement fund? That doesn’t seem right on the face of it. People in the workforce for 20-30 years are bound to have 100K in their 401K. Even people who save very little. Everyone wants to retire (and 100K is not enough anyway!) Am I missing something?

Yes, it is the sad reality that many people will essentially work as long as they can and otherwise live on Social Security, SSDI, Medicare, Medicaid, and other government programs. If you live in “upper middle classdom”, it can be easy to not notice that something like 30% of people age 55 and over have zero retirement savings. Of the other 2/3rds of people who do have some sort of retirement savings account, the median value for all folks 55+ is roughly $100k. I take that to mean that most (more than half) people will never have $100k saved in non-housing/car assets by age 65.

I think Munger is the right track, i see so many people getting hung up on how many millions when in truth they won’t attain 100K. With a typical job, you can only save what you can save so the actual balance is irrelevant. I always tell young people, save as much as you can, live below your means and stay disciplined about your investing. At retirement, you adjust your life style to the money you have.

I often come across “upper middle class” people who have 5 digit retirement accounts, a couple thousand dollars in what they call “emergency” funds, and a 6 digit credit card debt. These people tend to struggle with high mortgage payments and have home equity loans as well. If I were them, I would work on paying down some of the debt before I put money away for retirement. Would the amount in these people’s accounts be considered “assets” despite the debt?

Oops. I meant 5 digit credit card debt, not 6.

In my own experience, it took me and my wife 4 years to save the first $100,000. The next $100,000 should take less than 18 months. The next $100k after that should be about a year, but we’ll see how it goes. I think 100k of invested assets and no debt is an awesome initial goal and builds the habits and skills necessary to reach financial independence.

I remember those commercials! I was probably too young or just lacked the financial knowledge at the point to even understand what they meant by the “number” at the time, I just remember the numbers were huge. I am personally hoping to hit the halfway mark to $100,000 by the end of the year and it has been slow going. The snowball analogy is a good one, as my current portfolio barely moves with the market while my contributions have a huge effect. I think once you hit that mark is when the market starts do more of the “work” for you.

I can remember the time when I was struggling to reach my first 100,000. Living the normal lifestyle with a ton of debt was definetly counterproductive to this goal. Ten years passed and I never broke the 50,000 mark. Fast forward to today being debt free I have not only reached this goal in four years but now without consumer debt and living below my means have a good chance of hitting my new goal of 1 mil before I retire. I would have to agree with the stats in this articles. Most of my colleges earn a middle class income some as high as 200,000 per year and have no savings with literally a ton of consumer debt. Most of these folks lack the belief that they can change there finacial life. They have fallen victim to the consumerism lifestyle. It’s articles like this and the books I forced myself to read at first that have helped me to wake up and see the money. Now I can’t get enough and look forward to growing my portfolio. Truly what you save is important cause no matter what you earn if you spend it all it really doesn’t matter.

I remember hitting $100k and the unbelievable satisfaction that came with it. It was way more satisfying than $500k. Just felt like it took a lot more time and effort and was a big achievement. Now that I know what I am doing it’s not quite so hard so it doesn’t seem like as big of accomplishment when I hit other levels, but seeing six-figures, that was awesome.

Hi how many hours a week did you work to save and for how many years ? Also did you start a side business to make the rest or was it or purely just from your job ? ( 1 or 2 jobs ?)

I have actually said this exact statement to my friends. The savers know its true and agree and my non saver friends grumble and think its impossible, It took me about 8 years to get the first 100k and then about 6 to get to 200k. Now 6 years later I’m at 600k and 1 million in 5 years by the time I’m 52 looks very attainable on a good but not great salary.

Great article, I find it inspiring.

I am a dance teacher, earning less than 30,000. It took me about 10 years to arrive at $100,000. I hope to get to $200,000 in less than 5 years.

I just crossed $100k in 2015. It’s definitely the hardest as some people (like myself) actually start off with a negative net worth. The only way to get there is by living below your means and saving/investing the rest. Big fan of Mr. Munger, and that book is on my to-read list.

Yes, the first $100k is not a piece of cake and you would need a definite set of strategies and most importantly you need to think about the asset.

It’s still a valid article, I love it!

I haven’t achieved 100k yet in 12 years, but I’m quite close now: next year I’ll be there! I had very small salary in the beginning, now I have developed and have an average pay.

For 8 years ago I paid 30k as a down payment for our apartment and without that I’d have reached the 100k goal for years ago.

Btw, I never had any credit card debts and I spend my hard earned money wisely. I also do yearly comparisons of insurances, loan margins and so on – I recommend that for anyone!