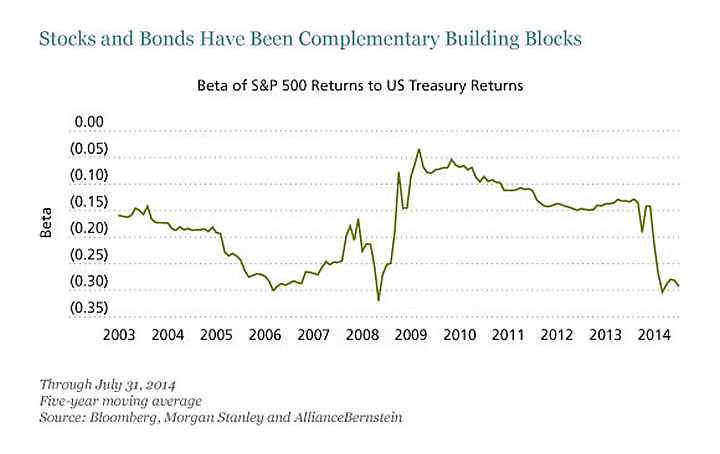

Inside this AllianceBernstein post about the more complex concepts of levering bonds and risk parity strategies, there was a reminder about simple portfolio construction. For a very long time now, holding both stocks and bonds has been considered a “balanced” portfolio. Why is this? Because stocks and bond returns tend to move in opposite directions.

This behavior can be summed up using the finance term Beta. The 5-year rolling average beta of the S&P 500 return to the 10-year US Treasury return has consistently ranged from negative 0.1 to negative 0.3 over the past decade. This means that when when stocks went up, bonds tended to go down (but not too far down). When stocks went down, bonds tended to go up (but not too far up).

Always good to have a reminder of the benefit of holding both stocks and bonds.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I’m having trouble understanding this. Why does this matter? If the mean and standard deviation returns for stocks and bonds remained the same as they are now, but the beta was instead +0.1 to +0.3, would you adjust your asset allocation?

Does holding assets with a negative beta make a portfolio “balanced”?

Balanced probably isn’t a good word. Yes though, you would adjust your allocation if the beta was different. The point of allocation is to generate the highest expected value or mean at a certain expected variance/standard deviation. You choose the acceptable variance based on your risk tolerance. Investing in any second position with a beta lower than 1 will lower your variance. The degree which beta is below 1 will lower the variance even greater.

So, if you were only buying the S&P 500 and a position with .2 beta you would need to put more of the money into the .2 beta position to maintain the same variance as could be obtained by putting a smaller amount of money into a -.2 beta position, which would leave you putting a larger amount of money into the S&P 500.

But, the negative beta doesn’t decrease the standard deviation (risk) of the alternative asset, right? So, what I don’t understand is why it matters whether both assets rise concurrently, inversely, or at random times with a given mean return and standard deviation.

Imagine this universe with only three possible investments:

Investment A: Mean 0.09, StDev 0.19, Beta +1.00

Investment B: Mean 0.02, StDev 0.02, Beta +0.20

Investment C: Mean 0.02, StDev 0.02, Beta -0.20

Are you saying that Investment C is superior to Investment B for all investors who hold some long position in Investment A? If so, why?

Here’s what your portfolio balance would theoretically look like if you had two assets with positive average return, some volatility, but perfect negative correlation:

http://investorsolutions.com/uploads/images/articles/2HypotheticGraph.gif

The two asset “balance” each other out and your total portfolio value goes up in a nice smooth manner.

That is true, but be careful–correlation is not the same as beta. Think of beta as the average correlation (although since beta can be above 1 and below -1 that’s not exactly true)

I like the explanation of beta from this link:

http://cpacfa.squarespace.com/beta-correlation-and-covarianc/

Jonathan, in a rising rate scenario where and how is your fixed income portfolio positioned?

I am trying to maintain an emergency fund for 1 year of expenses but am struggling where to place these funds (bonds, cash, CDs, iBonds, Emergency fund, etc).