Platinum Savings now at 4.10% APY. CIT Bank (not to be confused with Citi Bank) is an online-only bank that I keep open and going back to due to their multi-year history of competitive rates. They have a checking account, but their specialty is a variety of savings and CD products with high interest rates. I have used their No-Penalty CD for maximum optionality while maintaining a high interest rate (details below). Here are the highlights:

- 11-Month No-Penalty CD at 3.50% APY with $1,000 minimum to open. The 11-month CD keeps a fixed rate, but has no withdrawal penalty seven days or later after funds have been received. This means (1) high rate now, (2) interest rate will never go down during the term, (3) interest rate can still go up, and (4) all funds stay fully liquid. (If you have an existing No Penalty CD that you want to close and open up a new one, please see my instructions below.)

- Platinum Savings Account at 4.10% APY if you maintain a $5,000 daily balance or higher. 0.25% APY if your daily balance is under $5,000. No monthly fees. If you have any other savings accounts at CIT and can meet the minimum balance, you should consider moving funds over to this account. You can also open this new account without having to open another bank or credit union account.

- Savings Connect Account at 4.00% APY if you open with $100. No minimum balance and no monthly fees.

- 13-month Term CD at 3.50% APY.

Check out my rate chaser calculator to see if it makes sense for you to move money over.

New customer? Opening process overview. Here’s my review of the opening process if you are a new customer.

- The application process was completely online. You provide the usual personal information.

- You must submit to a credit check, but in my experience it was a “soft” pull which did not harm my credit. None of my various credit monitoring services showed it was a hard pull.

- You may fund via (1) electronic ACH transfer, (2) wire transfer, (3) mobile check deposit via CIT Bank mobile app (iOS and Android), and (4) mailing in a paper check. There was no option for credit card funding. I picked online ACH funding and you need to provide routing and account numbers, followed by manual verification via micro-deposits after a day or two. There was no instant linking option via login information.

After deposit verification, then your funding will go through.

You have successfully verified your external account. Please allow up to 5 business days for your funds to appear in your CIT Bank account.

No further action is required for this account. Thank you!

Existing savings or money market customer? Check your rate. If you already have an existing High Yield Savings account, it may remain at a lower interest rate than this money market account. If so, take a minute and upgrade yourself to the better interest rate. Click on “Open an Account” here, then “I have a CIT Bank account”, and then login with your username/password. You can do everything online and even fund your new Money Market account with an instant transfer from your existing Premier High Yield Savings. I wish I didn’t have to do this, but at least it literally only took a minute to complete.

How to transfer your money from an existing No Penalty CD into an new, higher-rate No Penalty CD (or any other new account). You have the option of moving the funds (with no penalty of course) over to a new CD with a new 11-month holding period if the current rate is higher than your existing rate. Here’s the easiest way to do so:

- Start a new online application for the 11-Month No-Penalty CD. Click on “Get Started” and sign-in as an existing CIT customer.

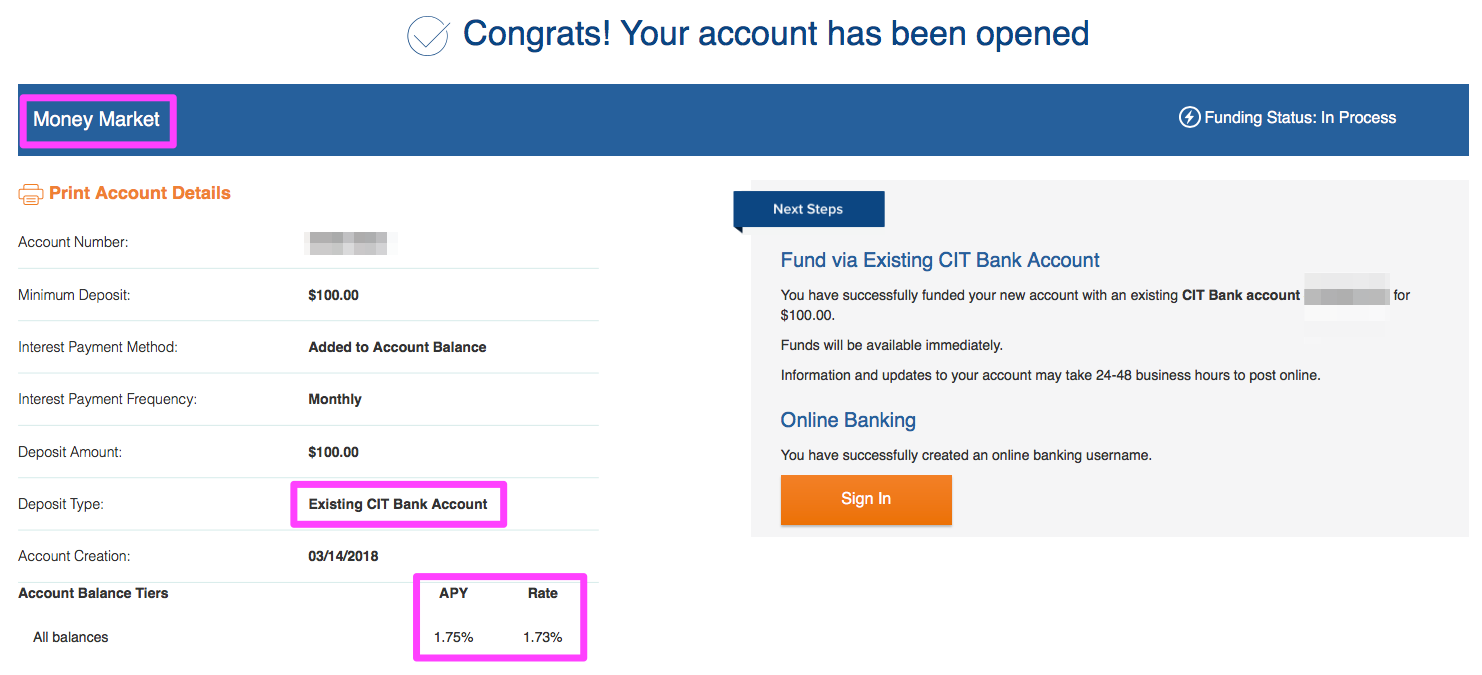

- After signing in, go through the opening process but look for “Existing CIT Bank Account” under “Funding Source”. You should see a list of your existing accounts, including any No Penalty CDs. (Screenshot below.)

- Note that online, your only option will be to have the entire CD balance (including accrued interest) moved over into the new CD. If you want a different amount, you’ll have to call CIT Bank customer service at 855-462-2652, open M-F 8a-9p ET, Sat 9a-5p ET, Sun 11a-4p ET. Press “0” for operator. Tell them you opened up a new No Penalty CD and you wish to fund it by closing out your old No Penalty CD.

- That’s it. The online option says it will take 2-3 business days to complete. Your new accounts will show up online.

User interface. While the front-facing website is pretty slick, after you login the backend is run by Fidelity National Information Services (subdomain ibanking-services.com). This is a popular backend software system used by many smaller banks and credit unions who don’t want to create their own software from scratch. It is better than before, but remains more functional than flashy. Similar story with the iOS/Android app.

Bottom line. CIT Bank is a lean bank offering targeted products for folks looking to get higher interest rates on their cash balances. They don’t maintain physical bank branches or fancy apps. However, I have been pleasantly satisfied with their customer service on my accounts with them. Their most compelling products are their Platinum Savings accounts and their 11-month No Penalty CD (thought not very competitive at the moment). The No Penalty CD is unique in that you are always able to move out to a higher rate, even within CIT bank itself, all while maintaining a floor if rates drop (yes, it is still possible for rates to drop!).

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Any reason not apparent to me why you would want to do this over ALLY’s 11 month no penalty paying 1.50% with similar terms other than having more than $250K in cd’s?

One possible factor is that the Ally CD does not allow partial withdrawals, so if you break it you’ll have to take out the entire balance of $25k+. As this CD has a $1,000 minimum, you can make multiple smaller CDs so that if you need money, you don’t need to withdraw everything. For example, you could take out 5x $5,000 CDs and just take out $5k at a time. It basically makes the No-Penalty CD closer to a regular savings account.

I don’t know why anyone would do these over brokered CDs. See Jonathan’s previous post on buying them. Rates are much higher there.

Back when fed was raising rates in 2017, I chased CD’s at banks and it was a hassle. I didn’t know about the existence of brokerage cd’s and being able to buy them at higher rates with two clicks. I am grateful though that Navy FCU has a feature which allows you to withdraw dividends so you can now take the dividends out of the 3% CD I opened back then and roll them into higher paying brokerage CD’s.

Unless Jonathan says otherwise, get your brokerage CD’s. Opening memberships in far away credit unions is a hassle and the rate is worse. Unless it comes with an opening bonus, I don’t get these.

Coincidentally, I just got a mailing for $100 bonus for a minimum 3 month $100,000 balance at 1.3% “FALL17” good til 12/21/17. bankoncit.com/premier17

Hopes all y’alls can use.

Oops, this review was published accidentally while still a working draft. I’m still working on gathering some information about their interbank transfers and adding screenshots, etc. Ah well, it’s up so I’ll leave it up and edit it later.

No problem, I’m glad you did as I have to spread some money out anyway to avoid FDIC limits. It’s now 1.35% online plus the $100 so that kicks it up to 1.45% for me (full year, simple interest).

CIT seems to be great on raising their No Penalty CD rates. As stated, the current 1.55% rate was recently 1.45%, but it was also as low as 1.25% as recently as about the middle of this year. Happy to see this keep rising.

Recently moved an IRA account from CIT to ALLY as CIT got out of the IRA business but offered to keep existing accounts at a terrible renewal rate. Process went from tedious to incompetent. Finally got it done after multiple phone calls and faxes. Have had accounts with them since 2013 and was happy with rates and ease of website. Maybe because it was an IRA account but moving everything back to ALLY for simplicity and better customer service.

These rates are great but for those of us who froze our accounts at all the credit reporting agencies, is there any easy way to start one of these accounts without removing the freeze everywhere for a few days??

Well, I suppose you could try and apply for an account, they ask you to give permission to do a soft credit check, but I’m not sure if they actually do it. If the application is denied, I don’t think any harm is one. Otherwise, I would say this is simply on of the hassles that come with credit freezes, and a major reason why I chose not to do one.

Suzanne,

9 month brokered CD’s at Schwab are paying 4.35%. If you want something more liquid, you can get a one month, 3 month, and 6 month CD all paying more than this. If you go out to a year, you can get 4.35%.

It’s 2 clicks to buy them on Schwab, Fidelity or Vanguard. You don’t have to unfreeze your credit or go through the hassle of opening an account somewhere. And the interest rate is much higher. And will probably be going higher. You can roll into one month CD’s paying 3.196 if you want to hold back until more interest rate rises come in before the end of the year.

Jonathan has a previous post about buying brokered CD’s. Look into it before you go through the hassle.

callable or not?

Does any one know which beareau it soft pulls from? I have a credit freeze so want to check.

Also how many external Banks does it allow to link?

I checked my Credit Karma and Credit Sesame and unfortunately those monitoring services don’t report soft pulls. I can only confirm no hard pulls from CIT Bank.

Dollar Savings Direct offers at 1.6% with similar easy T&Cs.

https://www.dollarsavingsdirect.com/

Thanks, that was quick, looks like they raised right after. Wonder which other banks will participate in leapfrogging in future months.

Why is 11-Month No-Penalty CD at 1.55% APY is preferred over Premier High Yield Savings at 1.55% APY when both of them offer the same 1.55% APY?

I wouldn’t say one is preferred necessarily over the other. Each have pros and cons. Savings accounts can go up and down with rates, but you can move money in and out easily. No Penalty CD will never pay you less than the given rate within the 11-month term, but you will have to break the CD to get your money out.

I just renewed a 2 year term at Pentagon Federal for 2.3%. There normal savings rate still sucks at .05% though.

What an unfortunate name. I immediately confused it with Citi, and after having a bad experience with them, initially did not read the article. I wonder how many others confuse them with Citi.

I am a customer of CIT Bank. Great rate on the No Penalty CD, however I get slightly frustrated with CIT as the process of closing and opening CD’s is not a simple process for them and seems to take forever. They need to game up their efficiency.

Took 8 days to open my account. Funded today.., finally.

Jonathan, I don’t think the PHY Savings acct has the 6 transactions per statement cycle restriction. As I’m looking at the “Overview” tab on CIT Bank site I don’t see that restriction on the PHYS, only on the new MM. That may be the main difference between the accounts.

I’m pretty sure that the 6 withdrawal limits applies to all savings and money market accounts due to “Regulation D”:

https://en.wikipedia.org/wiki/Regulation_D_(FRB)

I’m not sure why CIT Bank only points it out for the money market account, but my guess is that people are more likely to be confused by the term “money market account” as “money market mutual funds” have a similar name but with important differences like no FDIC-insurance.

Suzanne,

9 month brokered CD’s at Schwab are paying 4.35%. If you want something more liquid, you can get a one month, 3 month, and 6 month CD all paying more than this. If you go out to a year, you can get 4.35%.

It’s 2 clicks to buy them on Schwab, Fidelity or Vanguard. You don’t have to unfreeze your credit or go through the hassle of opening an account somewhere. And the interest rate is much higher. And will probably be going higher. You can roll into one month CD’s paying 3.196 if you want to hold back until more interest rate rises come in before the end of the year.

Jonathan has a previous post about buying brokered CD’s. Look into it before you go through the hassle.

how many external accounts can be linked in CIT? Trying to see if it can be my new “hub” account

I currently have 6 different accounts linked at CIT, and it lets me try to add another. I’ve read elsewhere that there is no official limit, but don’t know for sure.

Great, thanks. Sounds like my money is moving from Ally to cit !

Since Ally increased their rate on online savings accounts to 1.85% recently which matches my CIT No Penalty CD rate I just called CIT asking them to close my CD and transfer funds out. They offered me to reopen a new 11-month No Penalty CD at 2% APY. This rate is not advertised, it was offered to me by a CSR on the phone as a retention bonus. CSR guided me over the phone to open a new CD with “mail-in check” as funding source and then transferred the funds from the old CD to the new one. Process was quick and simple. Just an FYI.

Nice, thanks for sharing.

If I withdraw from the No Penalty 11-month CD after only two months, will I still get the 2.05% interest I acquired over that period — or do I forfeit interest since I withdrew before the 11-month period?

The 2.05% rate is an annual rate (as with all stated APYs), but you will earn interest on your money for those two months.

you don’t have to transfer it from existing CD via the phone… at least right now – there’s an option to do it online

Cool, you can now fund with an existing CD during the online opening process. That’s new! Thanks for pointing that out. I will edit the post.

I was lucky to have scored the 2.5% rate on a 12 month CD before they bumped the time frame up to 18 months on the same rate. And with rising rates I’m hesitate to lock up my money for more than a year.

Very good information. Thanks for writing this article, really appreciate it!. I used this to fund my new penalty CD with existing no penalty CD.

Thanks Jonathan! I had money sitting in a CIT Money Market account earning 1.39%. Just slid everything over to my new No Penalty CD account (per your recommendation). Btw, when I logged into my CIT account I was unable to find information about the No Penalty account. I had to use your link to find it!

You should check out brokered CDs and treasury bonds – easy 4% already!

So you converted/upgraded your no-penalty CD mid-month. Did they credit you partial month interest on the old CD, or should you have waited until Oct 1?

why not do 12 month tbills offering much higher rates?

Looks like Dollar Savings Direct savings account APY is now 3%.

2 things Jonathan:

1) The new no-penalty CD rate has increased once again, and is now 2.75%.

2) You state “You should see a list of your existing accounts, including any No Penalty CDs.” Only Money Market shows up for me. Does this mean I have to first sell the old CD?

As I mentioned, why not treasury bonds (3-month 4%, 1-yr 4.5%)? LOL.

aa,

I don’t think jonathan is touting this as a superior investment. He’s just describing this as one of many options, and I appreciate it, since it is far superior to Chase, as an example. Until the end of this month, I Bonds are at 9.62%, so your comment isn’t touting the highest available rate either 😉

We all know about iBonds but there’s a limit! And it’s locked like a 1-yr CD, come on, be liquid!

Not pleased with this CD. I’ve had it for about a month it does not give the option to withdraw or close the account without calling them. If you go to “Transfer” it just says you have to call them. I emailed them a couple days ago about this and still no response. I was actually thinking about opening up another CD with them but now I just want to get the money out.

Has anyone funded a new CD recently? If so, may I ask how long did it take to fund?

I opened a new CD and did the instant pull and CIT pulled the money from my bank, but the CD doesn’t show as funded. When I called CIT, they said they see it, but it takes them 5 days to process. I asked why it takes 5 days when they pulled the money already. They said that’s just how long it takes. I would understand if I “pushed” the money from the other bank that there would be a lag, but I’ve never seen it when the money is pulled.

I’m just wary since CIT isn’t inspiring a ton of confidence. I had problems logging into my old account to open the CD. CIT support said they had updated their system a while back and some accounts that didn’t have activity didn’t come over correctly. The system wouldn’t let me reset, so the rep asked me to create a new account, but their system wouldn’t let me create a new profile because it thought I had an account already. She had to escalate to her manager who said they would have IT fix and to give it a day.

I’m kinda in the same boat. I pulled money on 1/19 into my Money Market account, with the intent to buy a 4.75% CD, and although the transfer took place, the funds aren’t yet available?? (7days later).

Just opened a Marcus 10 month CD @ 5.05%