The Citi® Double Cash Card is a popular rewards credit card as it offers 2% flat cash back on all purchases, not just specific categories. As of March 2022, $1 in cash back rewards is also 100 Citi ThankYou points for potentially even better reward redemptions (details below). For example, if you value a Citi ThankYou point at 1.5 cents per point (by using the Citi Premier card and redeeming them as airline miles for free flights), then that is effectively get 3% value back! I’ve had this card for years.

The Citi® Double Cash Card is a popular rewards credit card as it offers 2% flat cash back on all purchases, not just specific categories. As of March 2022, $1 in cash back rewards is also 100 Citi ThankYou points for potentially even better reward redemptions (details below). For example, if you value a Citi ThankYou point at 1.5 cents per point (by using the Citi Premier card and redeeming them as airline miles for free flights), then that is effectively get 3% value back! I’ve had this card for years.

- Earn 2% on every purchase with unlimited 1% cash back when you buy, plus an additional 1% as you pay for those purchases.

- To earn cash back, pay at least the minimum due on time.

- No annual fee.

There is a 0% APR balance transfer offer available, but I must warn you that if you transfer a balance, interest will be charged on your purchases unless you pay your entire balance (including balance transfers) by the due date each month.

- Balance Transfer Only Offer: 0% intro APR on Balance Transfers for 18 months. After that, the variable APR will be 18.99% – 28.99%, based on your creditworthiness.

- Balance Transfers do not earn cash back. Intro APR does not apply to purchases.

- There is an intro balance transfer fee of 3% of each transfer (minimum $5) completed within the first 4 months of account opening. After that, your fee will be 5% of each transfer (minimum $5).

Cash back details. Imagine you make a $100 purchase. 1 point per $1 spent is 100 points. You pay the $100 bill from your bank account, and get an additional 100 points. Final tally: 200 points = $2.00 back on $100 in purchases. In other words, still 2% cash back.

There is no longer a minimum redemption amount of $25 for direct deposits into your bank account or statement credit ($5 minimum for paper check). You can redeem as little as 1 point for 1 cent, cashing out down to the penny.

You can redeem for cash via statement credit, direct deposit to your bank account, or a paper check. The direct deposit works with any Citi bank account or verified non-Citi bank account. In the past, this just meant that you made two successful credit card payments from your non-Citi bank account.

Citi ThankYou point details. Since $0.01 in cash back rewards is the same as 1 Citi ThankYou point, it is very valuable that Citi lets you combine Citi Thankyou points across cards. From their FAQ:

Can customers combine points from multiple Citi accounts?

Absolutely, as long as all the Citi Accounts are owned by the same person. If they have one (or more) Citi credit cards participating in ThankYou® Rewards, Citibank consumer checking account and other linked banking products and services, an enrolled Citi Corporate Travel & Entertainment Card, they can combine the associated ThankYou® accounts into 1 ThankYou® Account. Please note that if they combine their ThankYou® Accounts, points are not separated based on which Citi Account they were earned and are displayed as a total among all Citi Accounts.

If you have the Citi® Double Cash Card AND the Citi Premier Card:

- By having the Citi Premier Card, you can transfer the ThankYou points earned on the Citi Double Cash to participating airline mileage programs on a 1:1 basis including JetBlue TrueBlue, Virgin Atlantic, Singapore Airlines, Cathay Pacific, EVA Air, Etihad, Flying Blue by Air France and KLM, and Thai Airways.

- By having the Citi Double Cash, you can cash out the ThankYou points earned on the Citi Premier Card (which has the special feature of paying 3X points at Supermarkets, Restaurants, Gas Stations, Air Travel, and Hotels).

If you have the Citi® Double Cash Card AND the Citi Rewards+ Card:

- By having the Citi Rewards+ Card, you get 10% Points Back for the first 100,000 ThankYou® Points you redeem per year. For example, if you earn and redeem 20,000 ThankYou points, you’ll get 2,000 points rebated back to your account.

- The Citi Rewards+ Card automatically rounds up to the nearest 10 points on every purchase, so for example a $1 parking charge or $2 cup of coffee can earn 10 points. ).

If you have the Citi® Double Cash Card AND the Citi Custom Cash Card:

- By using the Citi Custom Cash Card, you get 5% cash back (5X Thank You points) on your top eligible spending category up to $500 spent each monthly billing cycle. (The Citi Double Cash card does not have any special categories.)

- By using the Citi Double Cash, you get 2% cash back (2X Thank You points) on all other purchases. (The Citi Custom Cash card only earns 1% cash back on all other purchases.)

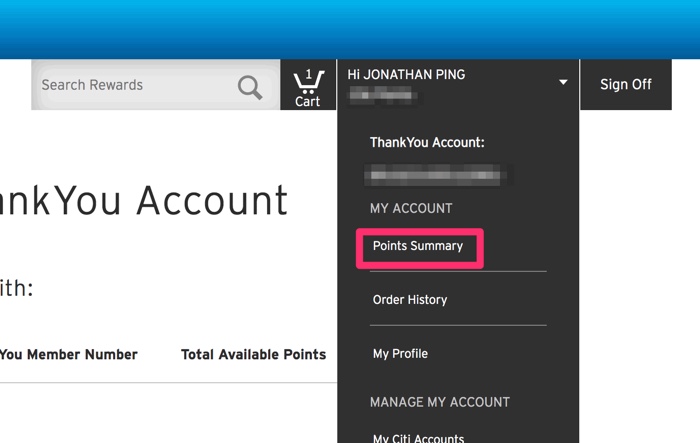

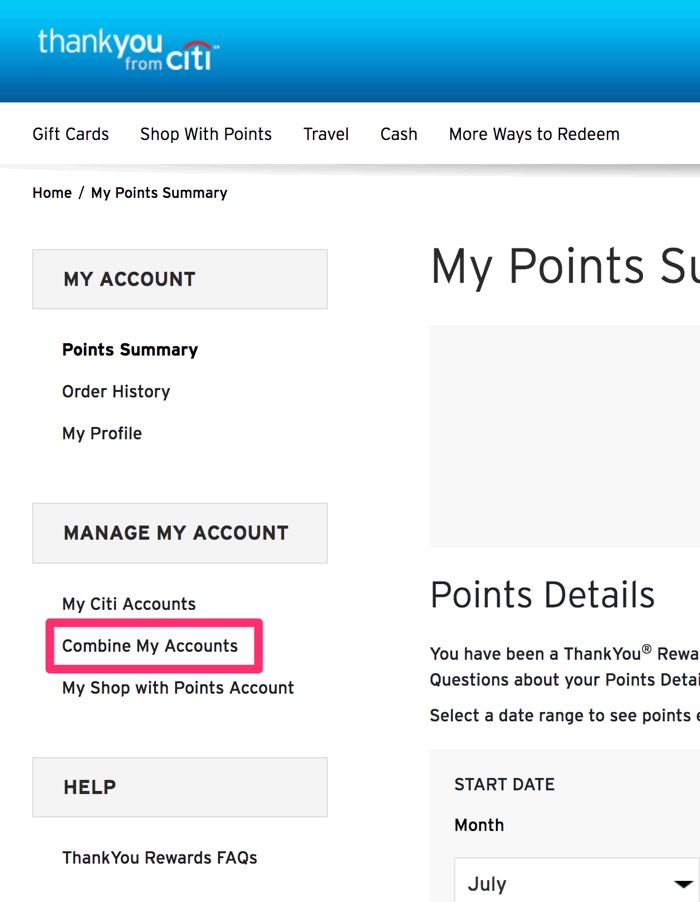

You can combine all of your various ThankYou points account into one account by calling Citi ThankYou at 800-842-6596 or the number on the back of your card. Alternatively, you can try it online by logging into your ThankYou account and clicking on “Points Summary” in the top right corner where it says “Hi [Your Name]”. See below:

As you can see, Citi has been steadily improving their ThankYou point program to make it more rewarding to hold multiple Citi credit cards. It is good for the consumer to have competition with Chase Ultimate Rewards, American Express Membership Rewards points, and Capital One Miles.

Bottom line. The Citi® Double Cash Card lets you earn 2% cash back on all purchases: 1% when you buy plus 1% as you pay. Everyone should have a 2% cash back card in their purse/wallets, even if they have other cards with higher cashback in specific categories. I’ve had this card for several years now. You can also convert $1 in cash back into 100 Citi ThankYou points, which offers additional flexibility and potentially more valuable redemption options when combined with other Citi rewards cards.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I have a Citi Dividend MasterCard, think they’ll let me convert to the Double Cash?

I just called and converted my citi dividend mastercard. It took less than 5 minutes.

I have had the Priceline 2% card for ten years. Any new accounts that are opened now only get 1%. But I have been GrandFathered and still get 2% cash back. I also have the Citi Double Cash card, but I carry a balance on it….so I use the Priceline card now for the 2%.

For restaurant and fast food I use US Bank GO card and get 4%. For grocery stores, I use American Express and get 6% back.

Cool, but one question: in the past (or even currently for some customers) Citi runs a tiered point system in that it considers some of its cards (often those with annual fees) to be “premium” cards that give you the standard 1% cash redemption options at 1 pt = 1 cent, and other cards non-premium cards that only provide a devalued 1 pt = 0.625 cent. Does that tiered system apply here?

This is a cash back card Cody, not a rewards card; so you’ll earn the 1% cash immediately after the purchase posts, and another 1% after you make the payment on your statement.

No ThankYou points of any kind.

This card doesn’t give you thank you points. It is cashback, like the Dividend card.

This beats the Fidelity AMEX and the hoops I’m jumping through for their 2%. As soon as I cancel this BarclayCard the week before the free year ends and the annual fee begins, this will be my card. Thanks for the info.

Which hoops? You mean the fee-free checking account it requires to redeem the full value of the points? I agree that this new Citi card is easier to use since it’s a MasterCard but on the flip side, Citi is known to categorize certain transactions as cash advance which no other card does…

My priceline.com card gives me 2% back on all purchases but you can only do a statement credit or get giftcards with it. This one sounds a little easier to get your money back. However, I just wanted to put it out there that there are other options as well.

@Eric – The Priceline.com 2% cash back card is no longer available for new applicants/customers, and hasn’t been since early to mid 2013.

Oh really? I didn’t know that… I think this card might be easier to get your money anyway as that one you have to have so many points and a charge that it works with etc. – still a good card though. I might grab this one too since good cards are hard to come by. Thanks for the info though as I didn’t know that about the Priceline card.

Where does it say Mastercard? It doesn’t say any thing Visa or any thing

I just converted a ThankYou Preferred card and the phone rep said it was MasterCard only. She initially offered Visa and Amex, but then corrected herself.

This was also my concern that the card does not say it is a VISA or anything else. How do vendors know it is a Mastercard and therefore would or would not accept?

If it is not on the front, the Visa logo will be on the back.

Also, the first digit of the 16 digits will tell them which network it processes on . (3=AmEx, 4=Visa, 5=MasterCard, 6=Discover.)

This is why I come here. Great news!

If you have a Chase Ink card, you can purchase Visa GC online and earn about 2.7% cash back on everything you spend.

$200 VGC with $6.95 Fee but you get 206.95*5 = 1035 Chase UR points or $10.35 plus you get 1% back on every purchase $200 or more at Staples from signing up for Visa Savings Edge program.

So $10.35 + $2.07 – $6.95 = $5.42

$5.42/$200 = 2.71%

My oldest credit line is with Citibank, but I rarely use it anymore. If I call to convert the card to this one would I keep the original opening date?

Applied and got approved. 4500 CL with 12.99% interest. I already have a grandfathered 5x Citi Forward card with 10k CL.

I called to convert my divdend card to the new double cash. “Oh the product is too new, and our systems are not updated. Sorry, I cannot convert it now. Call us in a few months.” Really?

You can call to verify, but I believe everything stays the same except for the name change along with new terms and conditions, which include rewards/cash back.

OK. 1% back on purchases and 1% back on payments. Could the statement credit option negatively affect your total cash back since you are reducing the amount of your payments toward the credit card bill?

Funny you should ask that, Citi just contacted me and said it shouldn’t be called a 2% cashback on everything because if you ask for your cash back by statement credit, you actually get 1.99% cash back. Imagine you put $100 on the charge, 1% is earned so you have $1. Then you redeem that $1 (ignore minimums for this example) for a statement credit which means Citi actually “paid” for $1 of the $100. So you pay the remaining $99 and get an additional 1% or $0.99 back. Final tally: $1.99 back on $100 in purchases, or 1.99% back.

If you ask for your cash rewards in the form if a statement credit, you’ll get 1.99% effective cash back.

If you ask for your cash rewards in the form of a check, you’ll get the full 2% total cash back.

Just FYI but your math is wrong, it is actually less than 1.99%.

Month 1) You spend 100$. You get back the 1$ and apply it. When you pay the bill you get back .99$

Month 2) You spend 100$. You apply the .99$ from last month bill pay AND the 1$ from the purchases for this month. That gives you 100-1.99=98.01$. Then when you pay the 98$ bill you only get back .98$ cents. So the rewards for that second month of 100$ spend is only 1.98%.

Thank you! Wonderful tip. I have to currently carry not just the Fid 2% card but also the CapOne QuickSilver 1.5% card for the many times AmEx is not accepted. Now I can carry one fewer card and get 2% always. 🙂

Chip

@ Danh & Jonathan Ping

I have the ink and am aware of the 5% back at staples but not of the 1% extra for $200 purchase . Is that form Staples or chase ? Can you provide me a link.

Bill,

It’s only working with a Visa Ink card. You can sign up here

https://www.visasavingsedge.com/members/home.php?sid=92XXdKrlo92&popup=t

Sounds like a great card but I’ll wait until they come out with a signup bonus

Jonathan, any thoughts/predictions on if/when there will be a sign up bonus for this card?

I don’t have any info on that, but my guess would be that (1) if there is a sign-up bonus, it won’t be for a least 6 months and (2) if there is one it will be on the order of $50 to $100. Usually these high cashback % cards with no annual fee offer smaller sign-up bonuses, like the Capital One Quicksilver with 1.5% cash back. The Fidelity American Express didn’t offer any sign-up bonus at all for years, then after a few years there was a brief $75 offer. So it could be a while (and it might never come) and you’ll be losing % back while you wait, so it depends on your patience, spending amounts, and what existing cards you have as backup.

783 credit score.. Got DENIED.. funny imagine that.

My recommendation would be to call the Citi reconsideration line at 800-695-5171 to see exactly why they denied you and see if you can do something to change their mind. Perhaps you already have more than 3 Citi cards, as they do have a limit on the number of simultaneously open Citi cards at a time. You may just have to close an old card and maybe reallocate some credit limits.

I know people could get net 4% cash back with the old blue from Amex if buying $500 giftcards from groceries and drugstores (after spending 6.5k that year on them) and using them everywhere else. And then there is that ink card…

Honestly, I would rather get only 2% and make things a lot more simple and secure -( I. E. What if someone snatches that gift card from you in the parking lot for example? ) . Also being able to track transaction details in mint (you can’t auto import transactions from GCs) is priceless.

This is the only website to recognize that this is not a 2% cash back card. If you collect 1% on charges and 1% on payments for 11 months and then apply the 11 months of rewards to reduce your payment in the 12th month, the cash back return is 1.982% for the twelve month time period. A similar calculation over a 4 month time period yields 1.985% return. Interesting that the advertised card terms imply achieving the actual 2% return with a higher cost mailed check. It will be interesting to see the final details.

If only it weren’t with Citi. I loathe their customer “service” reps…

Hmm… Here’s the thing.

I can almost always get 5% back on gas with one of the rotating cards. (Though good luck figuring out how much you spent on gas at the end of the year…)

I also get 5% on Restaurants (Grandfathered Citi Forward) and I eat out A LOT.

I have another card to get 3% back all the time on groceries from BBVA Compass. (They let you choose a few categories to get 3%).

So my 3 main categories (Gas, Groceries, Restaurant) each require their own card. I also have to carry the CostCo Amex for when I go there, Target Red and Lowes card also give 5% back….

I’m up to 6 cards! Adding this card to get an extra 1% on other purchases is a bit cumbersome.

That said, it would be nice to scrap it all and just have one 2% card for everything… I’d be leaving some money on the table, but tracking spending would then finally be possible. (I’m not even attempting to track spending with so many rotating categories on different cards..) I’d still probably use Costco, Red card, Lowe’s etc for the added benefits they provide.

Oh for a simple solution… Alas it doesn’t look like my “coin” card will get here anytime soon. (And even then it might not work for long with chip and pin around the corner.)

Why not just track your expenses with mint.com?

Mint always puts things in weird categories. I’ll spend hundreds of dollars on a medical bill and then get worried when mint emails me saying my spending on “shopping” is unusually high.

You can apply for Fidelity 2% card still right? I see their AD all the time when I login to my 401k account at Fidelity…

Fidelity used to have a Mastercard that offered 2% flat cash back with no tiers. That card is not longer available, but existing users have been grandfathered in for many years, not sure how long that will last though.

The current Fidelity AmEx is still 2% as they have higher merchant fees, but the current Fidelity Visa is 1.5% until you reach $15,000 in purchases for the year and then 2% on purchases over $15,000.

This is unrelated but its the first time I saw the Math regarding statement credit. Very interesting!

For this card its clear that you get 1.99 as opposed to 2%, but what about other cards like Spark Business and Barclay that also let you redeem for statement credit. I would think they are still fine and would net you full 2% as those cards flat out earn 2% and NOT 1% + 1% (for what you pay which is already reduced by 1%).

Am I right in assuming that? I have never really paid attention to redeeming for a check vs statement credit cuz its always easier to get a credit than go to bank or use banking app to deposit the check, until NOW.

Thanks,

@ Prince Barclay Card when redeemed for cash or statement credit is only worth 1/2 of the reward value, ie 5000 points is worth on 25$ unless redeemed for travel.

@ Sconi my wife also denied the card with score in the 780’s also, the letter said information provided could not be verified, whatever that means. We have been using the same info for 20 years. We could call as Jonathon suggests and I am sure get approved but with no bonus I dont think we feel like the effort, I might apply

Just called and converted my ThankYou card into this one, so I guess they’ve gotten their act together since KD tried a couple of weeks ago.

Mary Anna,

Were they able to retain your original Thank You opening date? I have a Citi card that I’d like to convert, but it’s my oldest credit line and I need to retain that date.

Ethan,

It appears so. It’s actually the same card number, and I just checked and it still appears as the same item on my credit report, with the same opening date. I think it’s just an internal change of type, doesn’t change the way it reports.

Thanks!

Thanks for the updates. I’ve also read other reports from outside blogs and forums and edited my review to include that information.

This is my experience. I have been a 10+ years customer for Citi cards. I called and asked to convert, and the lady was cordial. Since mine was Dividend visa card, she said number will change. She suggested that if I convert my dividend mastercard, number will stay the same. I wasn’t interested in 0% so I did not check. But, I asked about any incentives or cash for spending $X in Y months and she said that any promotions are not available for conversion. I was assured that my cash rewards pending balance would transfer over.

@Saagar, you’re not able to keep your existing Dividend Visa account number because the first four digits indicate what type of card it is (VISA or MC) and you’ll be changing interchange companies to Mastercard for this account. I called a couple days ago to convert my Citi Dividends MC to DoubleCash MC and no problem. Changeover was instantaneous, but new card will take 10-14 days to arrive.

My Citi AAdvantage card was due for annual fee/renewal and I wasn’t interested in renewing so I converted it to a Double Cash card end of Sept or beginning of Oct.

I just converted my Citi Dividend American Express card (which has been collecting dust) to the Citi Double Cash card over the phone.

Just converted my Citi Dividend Mastercard to the Double Cash. No credit check required, will get a new card and number, and can keep my unredeemed rewards dollars. I have to wait for the new card to arrive to start getting the benefits. Super easy!

just called Citi to convert my Mastercard Platinum Dividend card. Unfortunately my credit card number will change. Looking forward to the 1.99% (or 2%) cash back though, from the flat 1% (I rarely use the rotating categories)

Quick question, do you still get the 1% back on the payment if you pay down a portion of your balance before the statement is generated?

Yes.

@Ross, I just called to convert my Citi Dividend MasterCard to Double Cash and they said it could not be done and a new account would be necessary. What did I do wrong?

You probably didn’t do anything wrong, I just called and the guy checked if I could convert. Not sure why they wouldn’t let you convert. How long have you had the card? I would call back, sometimes getting a different CSR helps you get what you want…

I’ve had my card since 2005. You would think they would want to get me into a new, shiny card so I start actually using it again. But I long ago stopped trying to reason with Citi using business logic. I’ll call again here shortly and see if I have better success.

Well, I’m not sure if it was who I talked to or something I said that made the difference, but my call today got the card converted no problem. Good to go now!

Good deal, I had a feeling talking to someone else might do the trick

If you convert a dividend card to the double cash card do you keep the history? I would like to convert my dividend card, but it’s the oldest credit card I have and I don’t want to lose it on my credit report.

I would like to get the double back Citi Card but I do not want to post my social security online…please advise

Betsy

If you’re saying you don’t want to apply for it online – just call them and apply for it that way. You will have to give them your SS number, however, it’s how they’ll check your credit.

It should also be mentioned that you can get your cash back by Direct Deposit after two payments, instead of a check. They payments have to be form the same bank account, but I see no reason not to get the full 2%.

I didn’t know about this cash out option – thanks for sharing! Seems like an easy way to get that 2% instead if 1.99%.

As Nobody mentioned, direct deposit of the rewards is available as an option. Works great – the amounts are cleared in two business days from when I request them on the website.

Thanks for confirming what I’ve suspected all along! (So citi is in communication with you?) I’ve wondered for a while if the cash back percentage changes with whether the customer uses cash back as statement credit vs electronic fund transfer to bank account. To be safe, I’ve always gotten cash back as electronic deposit to bank account rather than statement credit. I think CITI is a great card for misc charges (utilities, dry cleaning, USPS etc) that aren’t covered by other special categories in cash back reward cards.

Hi Jonathan,

I am great fan of your blog and pretty much read all your articles. How does this beat the Amex Blue Preferred which gives 5% cashback on grocereis, 3% on gas , 2% on travel and 1% everything else? Ofcourse its has 75$ annual fee, but i feel its worth it

Thoughts?

There are definitely better cards for specific spending categories, but I’m saying that these cards are great to put a 2% baseline when other cards always give 1% for “everything else”. I have an AmEx Blue Cash Preferred for groceries too, but I also have the Citi Double to get me 2% on the rest. People spending $200,000 a year on their cards definitely have a lot of “everything else” and so do the rest of us.

Just a note that I called to convert my Citi Dividend card to the Citi Double Cash and had no problems… I picked the option to close my account and then explained my goal to the attendant. I can confirm:

1. My current rebate of $3 will be moved to my new account

2. New account number

3. Some various changes mostly in favor of the new card

4. My history as far as credit bureaus etc. are concerned will show that I’ve been a member all along since the opening of the source Divident card.

Very easy 5 minute phone call here. Good luck-

i converted my card also last week. Came from the Dividend World MasterCard, to the Double Cash card. Anybody know if you can get the PayPass added to this card, along with the chip it comes with? I requested it, but the card that arrived did not have it. I called back and they reordered it, but im waiting for it to arrive.

Card was awesome and the rewards were unmatched for my purchases. I am a business owner and used this card for several thousands of dollars a month. THEN….. MY CARD WAS HACKED! It has been 14 months since the unauthorized activity was spotted on my account. I have not even received a call from their fraud department. There have been many excuses but the main frustration is that there is no way to get a hold of the fraud department. You can fax them papers and information, but there is no number or email in order to talk to anyone. Worse yet, they did not report the fraud case correctly on my credit report. Therefore, I have had to call all 3 credit bureaus in order to correct the problem because you can’t talk to anyone at CITI Bank Fraud Department. I will never get a credit card or anything from this company.

Passing along a comment to watch all Citi cards for unexpected cash advance and interest fees, with no warning, if you use certain apps like Jpay & Venmo to make “peer to peer” payments. Gave my son a card who linked it to Venmo and in addition to paying Venmo a 3% upcharge on everything, I’ve been hit with 50$+ in charges so far for a few relatively minor transactions. Going to to call and lower my cash advance limit down to zero to stop this. Does not happen with other banks like Synchrony, another 2% back card.

BTW, my Citi 2% card is hacked twice per year, easily, and it is a major hassle each time but at least they are quick to issue a new card. Synchrony is horrible and took 2 weeks to resolve and re-open an account. The price you pay for 2% I guess…

Oops, spoke to soon about Synchrony Banks, was hit with fees and interest because of Venmo. Otherwise can be another good 2% cash back card on everything and the give the credit back on the statement IMMEDIATELY at the close of the month. Small signup bonus of $100 IIRC. Does not play well with Quicken, manual downloads possible only at the end of the month.

Best card for simplicity. Yes not technically 2% with the statement credits but not a material difference. Jonathan you rock!

I disagree with the conclusion, “By having the Citi Double Cash, you can cash out the ThankYou points earned on the Citi Rewards+ Card.”

It simply is not possible. I have both, and the ThankYou points for each card are walled off from each other, and cannot be combined into a Double Cash redemption.

Thanks, I guess it is a one way cash rewards to Thankyou point conversion, and doesn’t work the other way. Will update the post.

Upon some further research, have you called Citi to “combine” your card into one pooled ThankYou points account? It seems that many times each card starts out with its own TYP account, but you can merge them into one account. However, it may require a few phone calls to get a Citi customer service rep that knows how to help you. Once it is combined, your ThankYou points should all go into the same account.

The poorly designed Thank You redemption sub-site shows all we need to know: there is a merge page that presents sections for the origin Thank You account, and the destination one, and the origin section is always blank no matter which selected account either way. Yes, it’s always possible to beg customer service to make an exception, and pray that someone does something against policy, but that is certainly not a card feature to rely upon.

Not sure how you’re able to “value a Citi ThankYou point at 1.5 cents per point”. I’ve always redeemed them at a rate of 1 cent per point, so 5000 points = $50.

If you have a Citi Premier credit card, you can transfer 1 ThankYou point into 1 Singapore Airlines miles or 1 JetBlue TrueBlue point. Many people can easily redeem those frequent flier points at 1.5 cents or higher.

Posting his under “you can’t make this up” category.

Apparently WALMART can trigger an offer for a dollar off TY points redemption coupon at store checkout when your authorized user (wife) uses the Citi Double Cash card (maybe others with TY points). At conversion rates 25% less than the penny a point no less.

She has no idea about the reward game except to spend my money and thinks she is getting a free coupon from Walmart because of her good looks (I have to imagine there were SOME sort of disclosure somewhere using jargon on a tiny screen she won’t care to understand.

A few hours later (at work), I get an email about my account being used to buy GIFT CARDS. I’ve been the victim of this before with AMEX points (but at least they caught it.) So THREE hours total on the verification/chat/multiple phone calls with Citibank, filing fraud, changing user name, passwords, alerts, new credit card numbers, account no frozen, etc. This will mess up my Quicken for weeks afterwards. And they won’t reverse any of this when I called after coming home after getting an “oh by the way…”

Beware. This card is great but real fraud hits it twice a year. Hope this helps someone else out.