As you’ve probably heard, the Square IPO was completed last week. For a while, I didn’t understand how a company could have a $4 billion valuation when they basically offer a simplified merchant account. They let small businesses accept credit cards, which means they skim a tiny bit off the 2.75% they charge while most of it goes straight to the networks. (Add in their other expenses, and Square has never made a profit.) Wouldn’t you rather own Visa or American Express directly?

As you’ve probably heard, the Square IPO was completed last week. For a while, I didn’t understand how a company could have a $4 billion valuation when they basically offer a simplified merchant account. They let small businesses accept credit cards, which means they skim a tiny bit off the 2.75% they charge while most of it goes straight to the networks. (Add in their other expenses, and Square has never made a profit.) Wouldn’t you rather own Visa or American Express directly?

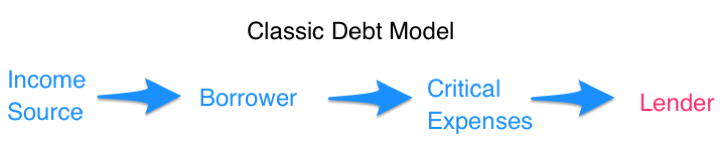

Then I read this Bloomberg Businessweek article How Two Guys Lost God and Found $40 Million (And sold Wall Street on a shady new kind of finance). Although I try my best to avoid carrying any debt, I do try to keep up with the industry. With a normal credit card, you are waiting around for the borrower to pay you back your principal + interest. The borrower gets their paycheck, pays for rent and food and whatever else, and hopefully gets around to pay you some interest. Here’s a cashflow visual:

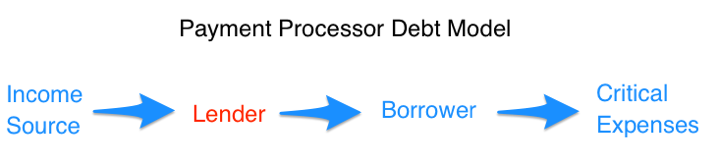

What these guys profiled in Businessweek did is give struggling small businesses a merchant account, and also lend them money. The key difference of their “merchant cash advance” service is that they would take the loan payments (including interest) directly from their gross credit card receipts! They were lending to horrible credit risks at sky-high rates (because nobody else would lend to them), but they knew they’d be fine because were first in line to snatch any incoming money before the business owner could even touch it. Here the modified cashflow visual:

Hmmm… if Square can pull something like that off on a big scale, maybe they can be worth billions. It turns out that both Square and Paypal do this same sort of lending. They lend to small businesses and taking money out from the incoming transactions. From a WSJ article dated May 2015:

Paypal said it has doled out $500 million in loans in the first year-and-a-half since it introduced the lending program. And rival Square recently said it had extended more than $100 million in cash advances in the year since it started its own version. […] PayPal, like Square, deducts money from merchants’ accounts based on their receipts, so that they aren’t on the hook if business slows.

From another WSJ article dated September 2015:

At both PayPal and Square, payments are taken as a portion of transaction volume, meaning merchants repay more when sales are high and don’t pay on days without sales. That allows for easier repayments, but makes it difficult to calculate an annual interest rate.

Wow. Ingenious or evil genius? It would be like lending to everyday people but being able to intercept their paychecks before they even landed in their bank accounts. You’d get the money before people could even have the chance to default (or pay for food). Some banks already have something called “direct deposit loans” allow them direct access to bank accounts, taking payments almost immediately after your paycheck arrives. It is possible for motivated people to switch off their direct deposit or move banks, but you’re giving the lenders a built-in advantage.

(A problem for Square is that competitor PayPal also does the free credit card swiper thing, but PayPal can avoid paying Visa and Mastercard whenever a user buys something with their existing PayPal balance. They just move some money around internally and pocket the savings.)

So what’s my point? For one, Square may have a growing profit source from these first-in-line loans to small businesses. Second, as a smart consumer, you should be careful to stay in control of your cashflow. I’d never give a lender permission to withdraw money at any time from my bank account. They should have to wait for me to pay them.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Regarding your comment, “I’d never give a lender permission to withdraw money at any time from my bank account. They should have to wait for me to pay them.” This is basically how all modern lending works. Lending Club, Prosper, OnDeck, everyone… they debit your bank account. The borrower doesn’t have a choice in the in the matter.

As for Square’s plan being “Ingenious or evil genius,” this model of withholding a percentage of card sales right from the source is 17 years old. Hundreds of funding companies just like Square, many of whom are much bigger than Square do this. It’s a $10 billion/year industry. It enables non-creditworthy businesses to obtain capital since the risk of non-payment is reduced.

Good article though. :]

True about LendingClub and Prosper, but I also don’t borrow from them. It is interesting though to look at their high rate of defaults when lending to sub-prime borrowers. People can apparently shut off even automatic withdrawals quite easily. If it was like merchant cash advance, they wouldn’t even be able to spend a penny before the lender got their cut. How long until this “direct deposit intercept” comes to retail consumers?

The first time I’d heard of “merchant cash advance” was the BusinessWeek article linked above. I’m more interested in the consumer view than the small business view. But we agree that such lending is an important part of Square’s future 🙂 Now, what if Visa or MasterCard wanted to get into the game?

Visa and MasterCard are unlikely to get involved because their strengths are in being payment networks. Their bread and butter is being removed from the liability of payment transactions altogether and just taking a cut off the top for facilitating them. They have the best model in the world.

As someone who has underwritten and sold merchant cash advances, I can tell you it’s very easy for businesses to circumvent the process that Square and other merchant cash advance companies have in place to collect. Since the collection happens at the credit card processor level, all someone needs to do is have a second merchant account. So if i got $10,000 from Square and then started accepting credit card payments through PayPal, First Data, or something else, no percentage is withheld and Square would be screwed out of their money. While a material breach of contract, it’s an extremely common practice for small businesses to employ. Often times, they’ll “split” the card transactions between both so as to slow down collection and not make the breach obvious.

There is no perfect way to collect from someone that doesn’t want to pay you.

“PayPal also does the free credit card swiper thing, but PayPal can avoid paying Visa and Mastercard whenever a user buys something with their existing PayPal balance.”

You can’t use your paypal balance obviously in an offline transaction where a card is swiped. The funding source is clearly the card (either card present & swiped, or card not present and entered into app). PayPal avoids interchange/network fees on online transactions when a the purchase is funded via ACH or an existing balance.