Long-term US Treasury bonds are often considered a good asset class to own due to their historically low correlation with stocks. When stocks go down, long-term bonds tend to go up (and vice versa). While the 30-year is not specifically included here, you can infer this based on the Treasury bond data from this Morningstar table:

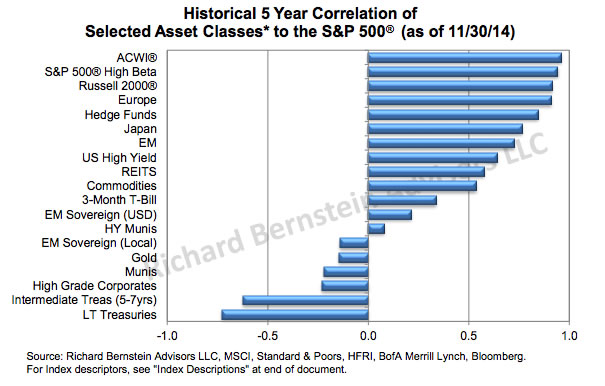

For example, here is an older 2015 chart with correlations agains the S&P 500:

While doing some additional research on adding long-term US Treasuries to a portfolio, I came across the concept of bond convexity. It’s a relatively complicated topic… I mean here is the very first sentence of the Wikipedia entry:

In finance, bond convexity is a measure of the non-linear relationship of bond prices to changes in interest rates, the second derivative of the price of the bond with respect to interest rates (duration is the first derivative).

Yikes! Thankfully, the next sentence is easier to digest:

In general, the higher the duration, the more sensitive the bond price is to the change in interest rates.

Yet, if you truly want to understand convexity, that sentence is quite incomplete. This is especially the case in low-interest rate environments like we have now in 2021.

After reading through some seriously tedious explanations mixed with college calculus flashbacks, I thankfully found the article High Profits and Low Rates: The Benefits of Bond Convexity at PortfolioCharts.com. I recommend reading the full post for an approachable explanation with no greek letters. The prize at the end is this excellent graphic:

As of this writing 8/23/2021, the yield on the 30-year US Treasury is 1.87%. Let’s round this to 2%. Based on this graphic:

- If interest rates were to drop by 1%, the 30-year bond would increase in value by roughly 27%.

- If interest rates were to rise by 1%, the 30-year bond would decrease in value by roughly 18%.

You may have though that since rates are so low already, any changes at this point won’t matter much. Turns out, they matter more. Long-term bonds can still pack quite a diversifying “punch” even at these low rates, both on the upside and downside (though not symmetrical). Those are some wild swings for “safe bonds”. This is definitely an interesting asset class, but be sure you know what you are getting into before purchasing.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Great column! And thanks for linking to portfoliocharts; I’ve never read such an easy to understand article on convexity and duration,

The problem is I trust my crystal ball that says rates are more likely to rise than fall… and it is quite a wallop.

I agree, the potential hurt is bad. Is the potential benefit worth the potential risk? I think this depends on the investor’s understanding and unique response to extreme events. I also worry about the possibility that both rates rise and the stock market goes down, as one day the Fed may find that they ran out of bullets.

I agree on the likelihood, but my larger issue is the asymmetric potential for rates to rise vs small. At 2 percent there’s not much room to fall. I’m sure they won’t go below -1 percent. (People will just hold cash). But there’s nothing preventing them from going up to 7 or 10 percent again

This is excellent! What does this understanding of convex ivory counsel we do when rates are likely to rise over time? Is this a good time to invest or only if you think rates will drop further?

The question is whether you want this behavior in your portfolio. I could easily see the rates go up 1% OR down 1%.

If something happens and the stock market tanks and the Fed does QE again and the rates drop 1%, now you have something that went up 27% when the stock market went down some big number.

If an economy boom happens and and the rates go up 1%, then you might have something that goes down 18% but hopefully when the stock market also goes up some big number.

Do you want the “smoothing” effect of such less-correlate asset classes? It would make either scenario less extreme. I’m always trying to learn more, but for now I am still happy with short and intermediate-term high quality bonds. I still get some smoothing effect, but like you said, I’m not as exposed to a long-term increase in interest rates.

They went so much into detail explaining how investor may benefit when rates fall… The key items is that

– longer dated bonds will have larger risk and hence larger potential reward

– returns on bonds with different maturities are not linear. i.e 30yr T-Bond is more than 3x risky comparing to 10yr T-Note

– what was explained applies to non-callable bonds. Callable bonds, like MBS, may have negative convexity and you may loose money when rates fall

Lastly, I think it is important to mention that investor’s return will be equal to bond’s yield at time of purchase if that bond is held to maturity.