Update April 2017. Digit is now a paid service. After a 100-day free trial, Digit will charge a $2.99 monthly subscription. If you are a current user, you also get another 100 days free but after that they will start taking $2.99 out of your linked checking account automatically. If you don’t want this to happen, you need to close your Digit account at this link. All your Digit balances will be moved back into your linked checking account.

I am disappointed Digit couldn’t make their business model work by simply earning interest off people’s savings balances. While some people criticized that aspect, I thought it was a fair trade-off. Although transparency is good in theory, my prediction is most people will balk at paying $3 a month. Digit has increased their Savings Bonus to 1% annualized (previously it was 0.20%). However, you can earn that at online banks elsewhere.

Updated full review:

Want to save more, but don’t want to actually think about it? Digit is a fintech start-up that combines a FDIC-insured savings account that want you to give it permission to tuck some of your own money away for you. There’s mindless eating, mindless spending, and now mindless saving.

How does it work? Instead of rounding up your card purchases or getting you to commit a regular savings schedule, Digit is like a helicopter parent sneaking into your wallet/purse and taking out money when it thinks you won’t notice. Okay, so it’s more about an algorithm that tracks your income and spending patterns… and then takes out money when it thinks you won’t notice. It keeps on depositing that money into a savings account until hopefully one day you have something substantial Here’s a slick video about it:

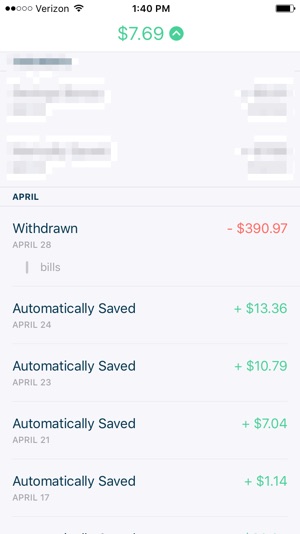

SMS Text-based interface. After you link up an existing checking account, ongoing interactions with Digit can be done almost completely by text message. If you prefer apps, Digit now has an iOS app that offers a little bit of extra polish to your normal text message program. I thought it might be redundant, but I actually prefer using the app now. A few screenshots:

Free. $2.99 a month. Digit used to make money by keeping any interest that might be earned on your savings balance. As of April 11, 2017, they now offer a 100-day free trial and then will charge a $2.99 monthly subscription fee. The good news is that you now earn more interest, currently a 1% annual Savings Bonus (details below). They still promise not to sell your transaction data.

Minimum balance protection. I actually started using Digit a few months ago, but turned it off when I found out they didn’t (at the time) have a minimum balance protection feature. For example, you might have a bank account that requires a $1,000 minimum daily balance to avoid a $10 monthly fee. Digit used to have no way of knowing that, although they did promise to refund any overdraft fees. Now, you can set a minimum value that Digit will not allow your account to go below.

Savings Bonus. Essentially, Digit pays you interest on your balances with them including your Rainy Day balance and any Goalmojis. Every 3 months you will receive a Savings Bonus from Digit based on your average total balance over the previous 3 months. Currently Digit pays a annual 1% Savings bonus. So for example if your average balance was $4,000 over the last 3 months you would get a $10.00 savings bonus that quarter.

My personal experience. Every few days, random amount like $5.22 or $11.35 would be debited from my checking account. Honestly, for some who likes to be in control, having all those extra entries on my bank statements got to be a bit annoying. After a couple months though, I had over $300 saved up. Was this amount more than I would have saved anyway? Would I be better off with a formal budget? It’s hard to say. I can imagine some people really liking the feeling of “found money”, though.

Recap. Digit offers mindless automated saving, which is definitely a unique proposition. After a 100-day free trial, Digit will charge a $2.99 monthly subscription fee. You’ll have to balance that fee with their ability to save you money that you wouldn’t otherwise. You might prefer giving someone else the steering wheel. You might not. If previously-reviewed Qapital was “set-your-own-rules”, Digit is more “leave-it-up-to-the-robots”. You could even use both apps at the same time.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

When I originally heard about this I assumed they sold your transaction info without bothering to find out. It’s good to hear that they don’t and hopefully they don’t surrepticiously change their privacy policy in the future.

I might just try this (or Qapital) out now because I always end up saving money on purchases but don’t have the desire to go through the process of an ACH transfer or budget adjustment to reclaim that savings. This might give my savings rate an additional boost.

The privacy policy very clearly states that they will share your information with third parties.

“We may use Personal Information for the purposes described elsewhere in this Privacy Policy and internally for our general commercial purposes, including, among other things, to offer our products and services and products and services of third parties that we think you might find of interest, but only Digit and our third-party service providers involved in distributing the offers or providing the products or services will have access to your Personal Information. Our third-party service providers will only be permitted to use Personal Information for that intended purpose.”

I read that three times and still don’t understand what it says. I think it says that they use your info internally to market stuff to you, and that they may use a third-party tool in that regard. I do wish it was less legal-ese.

Their FAQ makes a much more clear claim:

“Does Digit sell my information to third parties?

No, Digit does not sell any of your information to third parties.”

So basically now it only makes sense to do this if

1) You suck at saving on your own

and/or

2) You want to keep a large balance there.

Keeping $1000 wouldn’t make sense.. 1% interest would give you $10 and you would end up paying $3×12 = $36 in subscription fees.

Keeping $10000 would at least give you $100 in interest.

A.K.A break even point of keeping $3600 to nullify the $36 fee.

A smarter way of doing this would have been charging a % instead of a flat-fee but hey i dont own stock in this 😀