The WSJ has a nice introduction to dynamic withdrawal methods and managing your portfolio in retirement. They outline a few of the more popular variations – Adjusted 4%, Floor-and-Ceiling, and Guardrail. I like learning about dynamic strategies because I think they are more applicable to the real world and involve good ole’ common sense. When my portfolio is crashing and my dividends are getting cut, I think I’ll be fine with pulling back a bit as everyone else will likely be doing the same. If your investments have a good run and your income stream grows, and then you can spend a bit more.

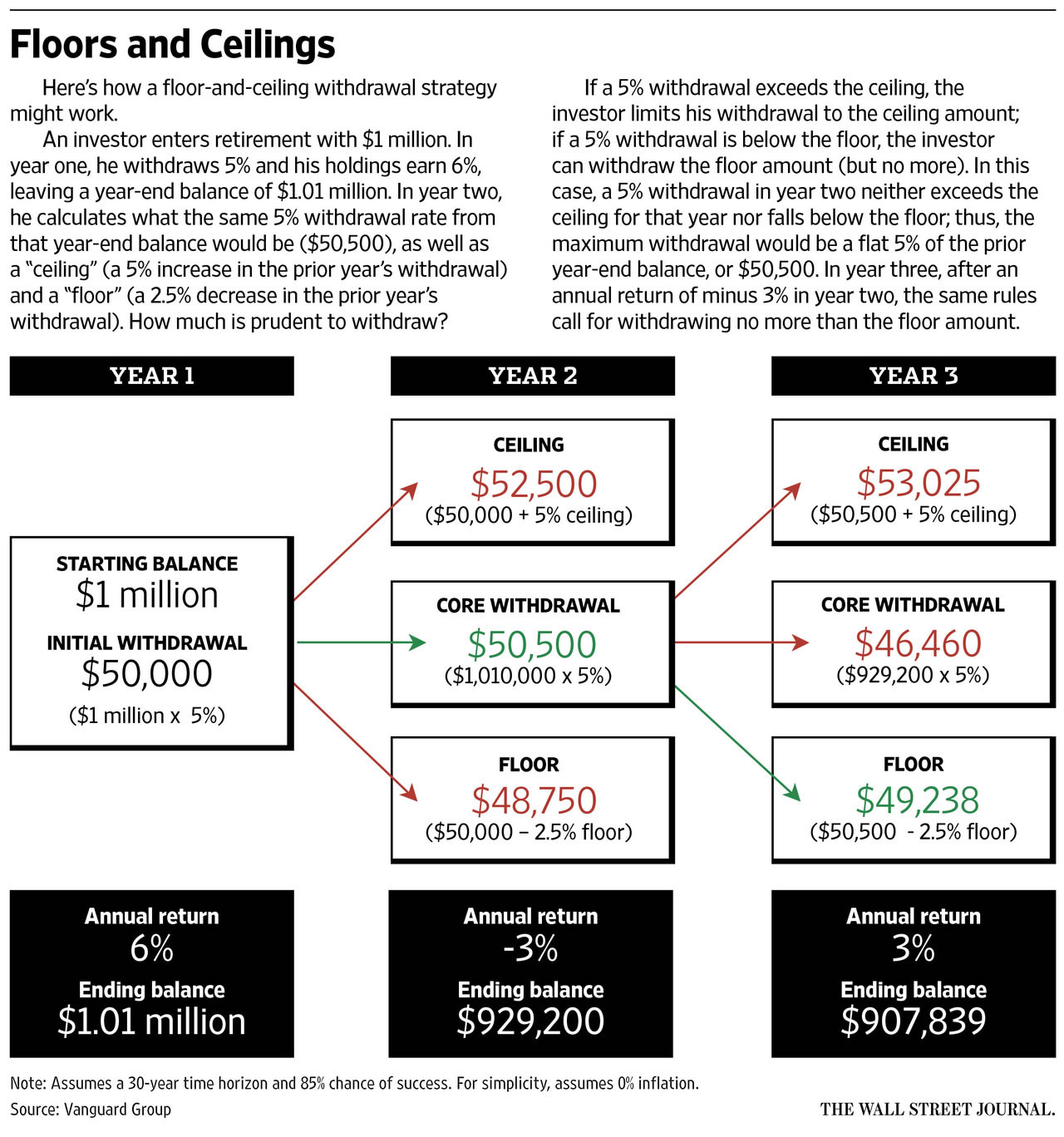

Here’s an infographic they put together to help visualize one type of dynamic strategy called “floor-to-ceiling” (click to enlarge):

Vanguard’s Managed Payout Funds are also designed to aid in portfolio withdrawals, using dynamic methods but adding in a smoothing component so that your income won’t swing as wildly from year-to-year. I don’t plan to buy those funds, but I might use their smoothing idea.

I am a conservative investor, so I don’t know about using dynamic withdrawals to justify a 5% average withdrawal strategy, though. It would just make 4% for 30 years less scary. In my case, I’m considering 3% dynamic for 50 years.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Jonathon,

If your just looking to pull out 3% a year.

aren’t there “safe enough” bond funds, where you can invest your whole retirement nest egg, and just live off the dividend?

VBLTX is currently yielding 4%

VLGSX is currently yielding 2.93%

thats just treasuries

there are investment and below investment grade with higher yields

i know theres risk there, but it would seem like if you just pulled out the dividend, you could seemingly go longer then 50 years

Be careful! Fixed Income ETFs like you list don’t work like regular bonds. You do not necessarily get your principle back. You could buy the fund at 15$ and it could drop to 10$ (which it has done). Rest assured, when interest rates start rising these funds will go down significantly in value.

Collecting 3% a year helps offset any loss to principle, but getting 3% per year, even over a couple decades, does not really yield 3% a year if you’ve lost half your principle.

I think the concern is inflation

Ideally, the dividend income would grow as fast or faster than inflation over time, hopefully enough to offset interest rates if they aren’t high enough.

I like the idea of only spending the dividend as a rough rule of what is a safe withdrawal, but for example it could be that dividends drop 20% as they did for the S&P 500 in 2008. If you had a more concentrated dividend portfolio, it could have dropped even further. That would be a pretty big spending shock.

Having a pre-determined floor/ceiling or some smoothing method would give you a concrete reason to adjust your spending by maybe 5% or less without involving emotions.

Yeah, I wonder why you are even worrying about this. The point for someone like you should be to get to a portfolio size where you can live off the dividends and never have to touch the principal.

Living off dividends is nice and I would love to do that, just have to be careful not to stretch too far for dividends or other high-yield products and know that all dividends can be a bit volatile. See my previous comment.

Yes, but doesn’t Jonathan have 2 children? That costs a lot.

interesting. glad to someone putting out that this perspective. Love vanguard. May not invest in those specific funds but adopt similar strategy.

Jonathan,

KItces and Wade Pfau have done lots of research in this area. On a related note have you read about the rising glide path and what are your thoughts?