Here’s a (late) Q3 2015 update on my investment portfolio holdings for 2015. This includes tax-deferred accounts like 401(k)s and taxable brokerage holdings, but excludes things like real estate and cash reserves (emergency fund). The purpose of this portfolio is to create enough income to cover household expenses.

Target Asset Allocation

I try to pick asset classes that will provide long-term returns above inflation, distribute income via dividends and interest, and finally offer some historical tendencies to balance each other out. I don’t hold commodities futures or gold as they don’t provide any income and I don’t believe they’ll outpace inflation significantly. In addition, I have doubt that I would hold them through an extended period of underperformance (i.e. don’t buy what you don’t can’t stick with).

Our current target ratio is 70% stocks and 30% bonds within our investment strategy of buy, hold, and rebalance. With a self-directed portfolio of low-cost funds and low turnover, we minimize management fees, commissions, and taxes.

Actual Asset Allocation and Holdings

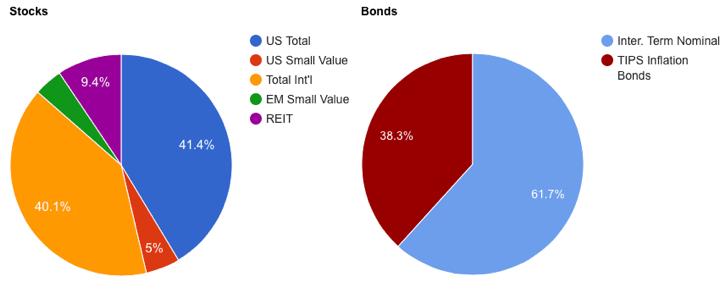

Stock Holdings

Vanguard Total Stock Market Fund (VTI, VTSMX, VTSAX)

Vanguard Total International Stock Market Fund (VXUS, VGTSX, VTIAX)

WisdomTree SmallCap Dividend ETF (DES)

WisdomTree Emerging Markets SmallCap Dividend ETF (DGS)

Vanguard REIT Index Fund (VNQ, VGSIX, VGSLX)

Bond Holdings

Vanguard Limited-Term Tax-Exempt Fund (VMLTX, VMLUX)

Vanguard Intermediate-Term Tax-Exempt Fund (VWITX, VWIUX)

Vanguard High-Yield Tax-Exempt Fund (VWAHX, VWALX)

Vanguard Inflation-Protected Securities Fund (VIPSX, VAIPX)

iShares Barclays TIPS Bond ETF (TIP)

Individual TIPS securities

U.S. Savings Bonds (Series I)

What’s New? Commentary

Things are still sticking pretty close to my target asset allocation. Before the year ends, I would like to relocate my “spice it up” holdings of WisdomTree SmallCap Dividend ETF (DES) and WisdomTree Emerging Markets SmallCap Dividend ETF (DGS). Mostly because a big chunk of their dividends are unqualified and thus subject to higher income rates. I can also do a bit of tax loss harvesting. But where to move them? I could squeeze them in my Fidelity Solo 401k plan that lets me buy ETFs (displacing either TIPS or REITs), buy similar mutual funds in my Schwab 401k brokerage window (displacing TIPS), or even buy some similar DFA funds in a Utah 529 account and consider it part of my portfolio (smart?). Or I could just liquidate them and just stick with total stocks funds (boring).

As for bonds, I’m still underweight in TIPS mostly due to lack of tax-deferred space as I really don’t want to hold them in a taxable account. My taxable bonds are split roughly evenly between the three Vanguard muni funds. The average duration across all of them is roughly 4-5 years.

A simple benchmark for my portfolio is 50% Vanguard LifeStrategy Growth Fund (VASGX) and Vanguard LifeStrategy Moderate Growth Fund (VSMGX), one is 60/40 and one is 80/20 so it also works out to 70% stocks and 30% bonds. That benchmark would have returned about 1.47% YTD for 2015 (as of 11/4/15). I haven’t bothered to calculate my exact portfolio return, but it should be close to this number.

I like tracking my dividend and interest income more than overall market movements. In a separate post, I will update the amount of income that I am deriving from this portfolio along with how that compares to my expenses.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

As an investing newbie, i am curious why such a heavy weight on the int funds. If American businesses are the best and most stable in the world, why don’t you put more into US stocks? I believe even Jack Bogle said the same thing to his kids. Again, just a newbie…but that made sense to me. As for me, I just have Vanguard Target funds (2045/50).

Please refer to this post regarding domestic v. international stock split. You’ll see my reasoning but also how I don’t think it is the biggest deal in the world. Keep in mind that your Vanguard Target fund is already 60/40 US/Int; it used to be 80/20 when it started. 50/50 isn’t far off.

https://www.mymoneyblog.com/us-international-stock-diversification.html

Why did you choose iShares instead of Vanguard for the TIPS portion of your bonds?

I have both Vanguard and iShares. I hold the iShares ETF in my Fidelity Solo 401k where the TIP trades commission-free while VIPSX would incur something like $50 per trade.

US stocks may be more stable than other countries but I don’t know that you can say that they are the best. Investors have been shown to have a home country bias just because they were born in that country. Bogle is right that US stocks have had a good track record. Some of that is better rule of law in the U.S.. The other part of that was natural resources available in the U.S. and then the benefits from a post-war (WWII) economy. A lot of that advantage has disappeared over the last decade. I think the allocation Johnathan has is a good way to take advantage of the potential growth the entire rest of the world can experience. If you read the bogleheads forum you will find people using similar portfolios.

I’ve been reading the Bogleheads forums too. John Bogle said to get rid of International stock funds last month. I have about 40% in domestic and 40% international (this is after tax money, not retirement) and I was going to move most of it to domestic. Hmmmm….

What happened to moving to 60/40 stock bond ratio?

60/40 is still my ultimate target in retirement.