Here’s a mid-year update on my investment portfolio holdings for 2015. This includes tax-deferred accounts like 401(k)s and taxable brokerage holdings, but excludes things like physical property and cash reserves (emergency fund). The purpose of this portfolio is to create enough income to cover all of our household expenses.

Target Asset Allocation

I try to pick asset classes that will provide long-term returns above inflation, distribute income via dividends and interest, and finally offer some historical tendencies to balance each other out. I don’t hold commodities futures or gold as they don’t provide any income and I don’t believe they’ll outpace inflation significantly. In addition, I am not confident in them enough to know that I will hold them through an extended period of underperformance (i.e. don’t buy what you don’t can’t stick with).

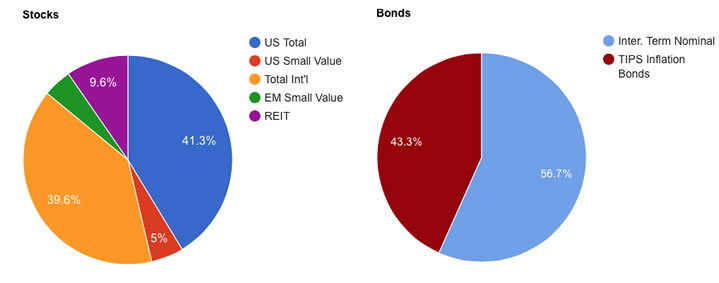

Our current ratio is roughly 70% stocks and 30% bonds within our investment strategy of buy, hold, and rebalance. With a self-directed portfolio of low-cost funds and low turnover, we minimize management fees, commissions, and taxes.

Actual Asset Allocation and Holdings

Stock Holdings

Vanguard Total Stock Market Fund (VTI, VTSMX, VTSAX)

Vanguard Total International Stock Market Fund (VXUS, VGTSX, VTIAX)

WisdomTree SmallCap Dividend ETF (DES)

WisdomTree Emerging Markets SmallCap Dividend ETF (DGS)

Vanguard REIT Index Fund (VNQ, VGSIX, VGSLX)

Bond Holdings

Vanguard Limited-Term Tax-Exempt Fund (VMLTX, VMLUX)

Vanguard Intermediate-Term Tax-Exempt Fund (VWITX, VWIUX)

Vanguard High-Yield Tax-Exempt Fund (VWAHX, VWALX)

Vanguard Inflation-Protected Securities Fund (VIPSX, VAIPX)

iShares Barclays TIPS Bond ETF (TIP)

Individual TIPS securities

U.S. Savings Bonds (Series I)

Notes and Benchmark Comparison

There has been very little portfolio activity over the last 6 months. No major market movements (the S&P 500 hasn’t moved more than 2% in day so far in 2015). No mutual funds added or removed. I continued to invest in the same funds through 401k auto-contributions and the occasional fund purchase from saved income. Things are little off, but I’ll just wait and rebalance with new money. Some of my usual savings has been diverted to college savings. Mostly, just keeping my head down and moving forward. 🙂

A simple benchmark for my portfolio is 50% Vanguard LifeStrategy Growth Fund (VASGX) and Vanguard LifeStrategy Moderate Growth Fund (VSMGX), one is 60/40 and one is 80/20 so it also works out to 70% stocks and 30% bonds. That benchmark would have returned about 3.5% YTD for 2015. I haven’t bothered to calculate my exact portfolio return, but it should be roughly around this number.

I like tracking my dividend and interest income more than overall market movements. In a separate post, I will update the amount of income that I am deriving from this portfolio along with how that compares to my expenses.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I would be interested in knowing what you hold in pretax retirement vs post tax retirement vs regular brokerage account? Do all three of the accounts have identical holdings?

My tax-deferred accounts (Roth, Traditional IRA, 401k, Roth 401k) mostly consist of the acronyms… TIPS and REITs. Stocks, muni bonds are in taxable.

MMB,

I would be interested in seeing the trend in your passive dividend and interest income over time. I know you won’t talk about numbers, but the trend would be pretty amazing to check.

Instead of numbers, you can for example use what percentage of expenses has been covered by dividends. For example, if you earn $500/month in dividends and your expenses are $1000/month, you just put 50%.

Best Regards,

Dividend Growth Investor

So, you’ve increased your saving for college. Details…details?

Working on it, don’t have a cohesive investment plan yet, still considering all the investment choices including DFA funds, etc.

Why only 5% in International Emerging stocks. In India, the returns are good in last few years with target growth rate between 7-8%.

Technically he has more than 5% since he’s also 40% in the total world ex US… so there’s some duplication there.

FTSE Global All Cap excluding US Index is roughly 20% Emerging Markets.

I’m curious if you have enough $ by the 33x spending rule… I’ve been reading your blog since 2007 — rooting for you!

JR, what is the 33x spending rule? I googled it but didn’t find anything definitive. The first result was about some 4% spending rule.

33x spending is equivalent to 3% withdrawal rate. I’m pretty close; tomorrow is my income update.

With the strong academic support and the now cheap access to ETFs, have you considered adding a momentum component to your portfolio?

I’ve read some of the research on momentum and agree there is something there, but it also seems to be hardest to stick with due to long periods of relative underperformance. I have no imminent plans to try and take advantage of momentum effects.

Is there a free website that is similar to Mint.com but tracks your asset allocation? I have so many accounts (my 401k, 401a, roth IRA, 529, wifes 401k, roth ira, taxable) and several of my funds from earlier in my investment career are in things like vanguard target retirement 2035 (which has a changing balance of stocks/bonds. I just want to plug in all the accounts and have it spit out the asset allocation. i don’t think mint does this for me. What does?

Vanguard’s website will let you manually add funds from other firms.

You can try Personal Capital. Here’s some info from an older post, although it may be a little dated:

https://www.mymoneyblog.com/personal-capital-investment-portfolio-management-tool-10-bonus.html

Jonathan,

I’m curious as to why you don’t add int’l REITs to your allocation, since you seek diversification, income, and growth potential. Seems to me the VG ETF is relatively cheap and the yield is attractive.

I think international REITs are a reasonable choice to add to a portfolio. I suppose that I am less comfortable with them as I don’t have a full understanding of how REITs are structured in outside countries vs. the US. The costs are reasonable but still higher than domestic, so in this case my allocation to REITS is small enough that I choose simplicity over any diversification benefit. Maybe that will change in the future, but these days I am loathe to add complexity. I’m even thinking about ditching my small value ETFs for simplicity but I’d like to wait and make that decision over a longer timeframe.

Nicely picked assets. Below you find an optimally allocated portfolio that increases the expected returns for a certain amount of risk.

Yearly expected return: + 7%

Yearly expected risk (volatility): +/- 5%

20 % VTIVanguard Total Stock Market ETF

10 % VXUSVanguard Total International Stock ETF

16 % DESWisdomTree SmallCap Dividend ETF

6 % DGSWisdomTree Emerging Markets SmCp Div ETF

7 % VNQVanguard REIT ETF

6 % TIPiShares TIPS Bond

7 % VMLTXVanguard Ltd-Term Tx-Ex

6 % VWITXVanguard Interm-Term Tx-Ex Inv

17 % VWAHXVanguard High-Yield Tax-Exempt

6 % VIPSXVanguard Inflation-Protected Secs Inv

You may choose to take some more or less risk. You can compute the optimal portfolio on https://swanest.com

Wondering why Jonathan is so high in int. stocks. If you believe in American businesses (best in the world), shouldn’t you be putting more into US stocks? Even Jack Bogle says one should only keep about 20-30% in international stocks. I’m a newbie, so take what I say with a grain of salt.