If you are into podcasts and enjoy long conversations about higher-level personal finance topics (put that in your dating profile!), check out the Radical Personal Finance podcast. I’ve only listened to a few, but I enjoyed Episode 181 on The Impact of Your Savings Rate on Your Time to Financial Independence. If you make $50,000 a year and spend $40,000, then your savings rate is 20%.

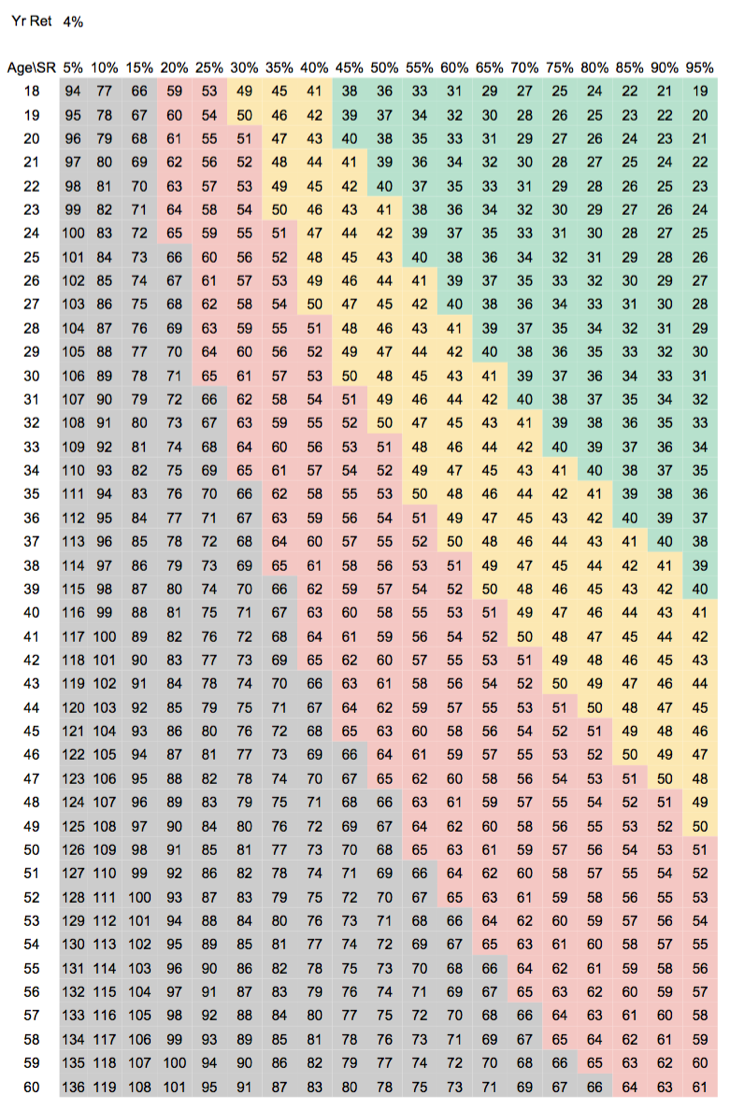

Based on math formulas mentioned in the podcast, a commenter named Philip Frey created a “heat map” Google Docs worksheet with starting age, savings rate, and age at financial independence. Green means you retire by age 40, yellow by age 50, red by age 65, and grey… means you’ll be heavily reliant on Social Security. 😉

I believe the assumptions include (1) both income and spending numbers are after-tax, (2) once you reach 25 times expenses you reach financial independence (4% safe spending rate), and (3) outside pensions and Social Security are ignored. It’s not perfect and I wouldn’t take hard numbers from this chart, but it’s still a neat visualization.

Savings rate is a great way to measure your velocity towards financial independence. Treating the components of income and expenses as separate, as opposed to intricately linked as most people assume, is the key takeaway.

Achieving financial independence is quite difficult no matter how you do it, but my bet is that at least 10x more people have achieved early retirement through high income and average spending, as opposed to average income and very low spending. This is based on our own observations, including having household income that varied between slightly below average and well above-average. I could be wrong; I’d love to see some good data on this.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I see on the top of the chart “YR Ret 4%”. I assume that means your returns are calculated at a 4 percent annual real return (after adjusting returns for inflation) each and every year. In our present investment environment that may sound very good considering what fixed income investments are returning. But unless one is willing to risk a significant portion of those savings in stocks or other “riskier” investments (and not bail out when things turn bad), even a four percent real return year in and year out may be too good to be true. You sure won’t see that type of return in a saving account or CD…

I started saving 10% when I got my first job at 21 and I’m STILL in the grey zone?!? Very discouraging. Just goes to show that you can do everything right and still get shafted. Life isn’t fair. 🙁

10% is not enough. Never has been… which is why so many older folks are screwed…

It should be though. I’ve been saving 15% for the last several years and I still don’t think it will be enough. If 10% is enough for God, it ought to be enough for the government and for retirement.

There is so much to argue with here. For one thing, I’m not even sure that counts as a heatmap. But more importantly, the 4% SWR rule of thumb only applies (if at all!) for time periods of 30 years or less. Everyone in the “green” area of the chart is in for a surprise if they were to rely on it.

Are we keeping taxes out of this? In your example, 50000 income is after income and payroll taxes?

I’m 31, have been investing for the last 8 years and have taken a net worth of ZERO to $680,000. I have done this by always having 15 year mortgages, maxing out my employee retirement account 401K and continuing to save another 10-20% after tax. Also, if you work the long term numbers and don’t distribute your funds into bonds or money markets once retired you should be able to make on average 7% which would allow you even at the age of 40 to continue to withdrawal 3.5% a year and never run out of money. Check out this great article. http://www.madfientist.com/safe-withdrawal-rate/

I absolutely love this sheet. it’s a great starting point for anyone who is think about early retirement and what is involved. Everyone’s personal situation will be different, so using this as a starting point will give you a better idea of how much you will need to save and live off of as time goes on. Thanks for sharing this!

Andrew

FamilyMoneyPlan.com

I think you’re right – “at least 10x more people have achieved early retirement through high income and average spending, as opposed to average income and very low spending.” You can only cut spending so much, so very, very low spending is pretty rare. In our case, we had a moderate savings rate earlier in my career, but as my income grew rapidly (mainly from becoming a freelancer), we kept our spending growth very moderate. We definitely spend more now than in years gone by, but it grew at a more steady, pace.

This method also seemed less painful. We really didn’t “cut” anything; we just didn’t allow it grow as fast as our income.

Nice post.

John

There’s so much wrong with this chart. The reason we call it personal finance is because it is exactly that personal. What I may need to retire with does not mean that every one needs the same. Some may have a pension, social security or even a disability payment. Others may live a life more conservative or more luxuries. Either way there’s a ton of variables that come into play here that a single chart could ever cover. This is just bad for all. Talk with a professional and yes invest as much as you can. Who knows you maybe further ahead than what you think.

There must be many more assumptions that would need to be understood before getting value from this “heat map”. (Ex. If I start saving at age 18 with a savings rate of 95%, I can retire at 19!). I am guessing there is an underlying income assumption and the retirement age is functioned off of that and a 4% retirement withdrawal rate.

Interesting. According to this chart, if we pay off our debt over the next couple of years, then we start saving 90% of our income at age 37, we can retire at 40 years old (per the plan). Of course, as pointed out above, there are other factors to be considered. We have been saving a small percentage of our income for some time now. And, we plan to continue to earn money from various part-time work after age 40.