As 2015 winds down, here is a snapshot of the asset class forecasts provided by GMO and the most recent market commentary by co-founder Jeremy Grantham. You can access both of these at GMO.com, although some items require free e-mail registration.

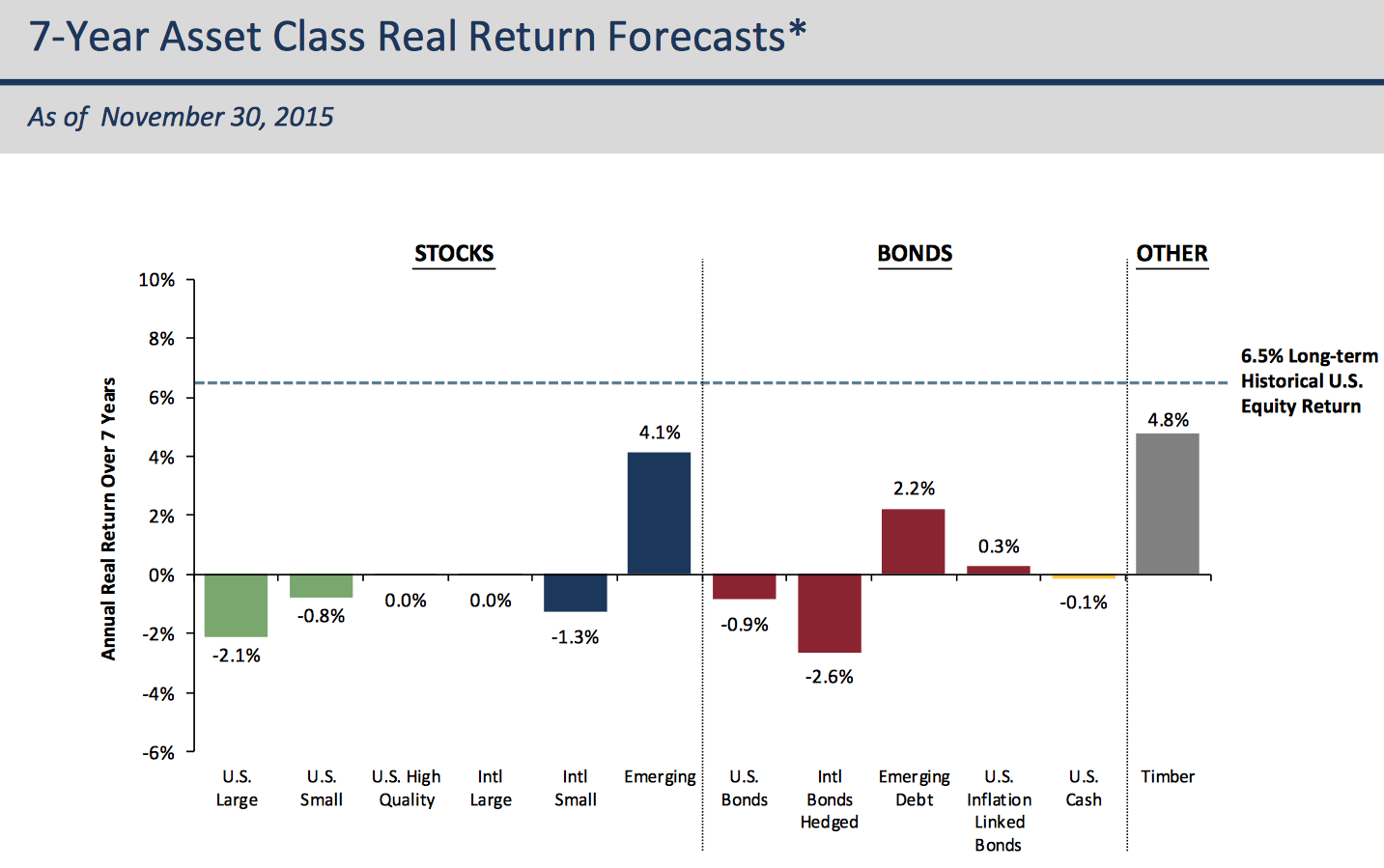

Here is a snapshot of their 7-year expected future returns by asset class, inflation-adjusted, published in mid-December 2015 and using data as of November 30, 2015.

The chart represents real return forecasts for several asset classes and not for any GMO fund or strategy. These forecasts are forward-looking statements based upon the reasonable beliefs of GMO and are not a guarantee of future performance. Forward-looking statements speak only as of the date they are made, and GMO assumes no duty to and does not undertake to update forward-looking statements. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results may differ materially from those anticipated in forward-looking statements. U.S. inflation is assumed to mean revert to long-term inflation of 2.2% over 15 years.

I like to keep track of these forecasts along with those provided by:

- Research Affiliates Expected Returns by Asset Class Tool

- Portfolio Solutions® 30-Year Market Forecast for 2015

- Reasonable Expectations for Financial Market Returns – John C. Bogle and Michael W. Nolan, Jr.

Here are some reasons why I like keeping track of these types of forecasts:

- The projections are based on fundamental, historical, and valuation-based models. This is not to say they can’t be wrong, but the strategy is at least unemotional and provides a reasonable range of expectations.

- They usually provide support for rebalancing and buying more of beaten-down and unpopular asset classes. Currently, Emerging Markets stocks would fit that description.

- They usually temper the mass enthusiasm for putting all your money in hot and popular asset classes. Currently, US stocks would fit that description.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Wow, those are some difficult expected returns.

Alas, a few years ago, emerging markets was still the asset class with the highest expected return. That hasn’t worked out so well in the short term…

Does make me curious about ETFs like TMBR and WOOD though…

Scratch that… The other timber ETF is “CUT”, not TMBR.