I’ve read Jeremy Grantham’s quarterly letters and the GMO 7-Year Asset Class Return Forecasts for over 8 years. (Anyone can sign up at GMO.com for free.) Grantham gained successively more fame after avoiding the Japanese bubble, the Dot-com bubble, and the Financial Crisis. Given the recent talk about record bull markets, let’s take a look back and see how accurate the most recently applicable GMO predictions turned out to be.

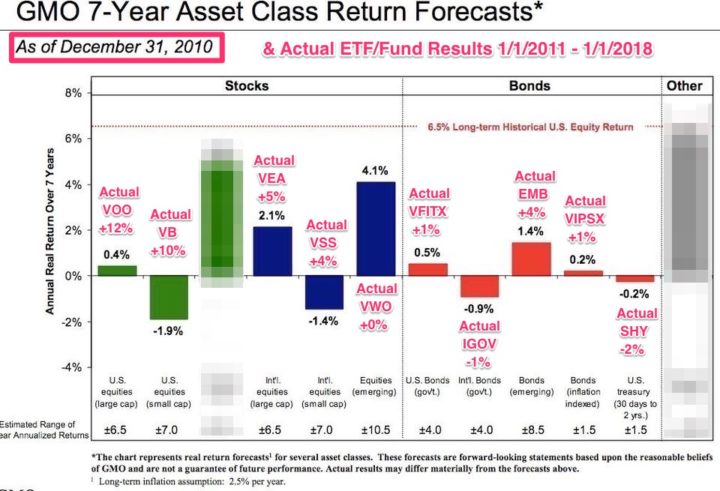

Let’s compare the GMO 7-year return forecast with reality, in this case actual returns from January 1st, 2011 to January 1st, 2018. Below is the forecast chart as of December 30, 2010. I looked up the closest ETF or mutual fund that I would have invested in for each asset class, and then found the total return via Morningstar or ETF Replay for 1/1/2011 to 1/1/2018. According to BLS.gov and SmartAsset, the total inflation during that same period was 1.6% to 1.7 annualized. I added the actual 7-year real returns onto the old prediction chart below.

(The blurred-out asset classes are basically special investments that GMO was selling to their institutional clients that the Average Jane could not have easily bought via ETF or mutual funds. Since they didn’t make their position clear in the beginning, it’s hard to judge the subsequent results.)

Some quick and simple observations:

- US Large-Cap and US Small-Cap stocks did a lot better than forecasted. Compounded over the full 7 years, the difference was on the order of doubling your money vs. making nearly nothing.

- International Developed Large-Cap and International Small-Cap stocks also did significantly better than forecasted.

- Emerging Market stocks did significantly worse than expected.

- Bonds did about as expected across the board.

Reading the commentary is always illuminating and helps me better understand their forecasts. Grantham has addressed these results here and there, but basically he still thinks a reversion to the mean will happen eventually. Here’s a quote from one of his recent quarterly letters:

“Relative to what we were thinking [in 2010], emerging equities have done surprisingly badly, and the U.S. equity market has done surprisingly well,” said Grantham. “Was that the luck of the draw, which has no bearing on future returns? Was it a temporary phenomenon that will soon reverse? Or does it tell us something important about emerging being a value trap and/or the U.S. being extraordinary that we need to take into account in our forecasting of the future?”

The short answer to these questions is that while emerging markets “deserved” some of their bad luck over the last several years and the outperformance of the U.S. has made some sense, we do not believe that emerging is a value trap, nor do we believe that the U.S. has proved itself particularly extraordinary.

Here’s GMO’s most recent forecast as of July 31st, 2018:

I understand the fundamentals behind these numbers, but I can’t help but think that if you keep calling for a drop long enough, it’ll happen eventually. There’s a reason why market timing is hard and why it’s called a “risk premium”. You never know exactly when the drops will come. All you might really be able to say is that a drop is more likely now than when people were worried in 2014, 2015, 2016, 2017… The rubber band is stretched, but it’s been stretching for a while and it could still stretch even longer.

Bottom line. Forward-looking stock return forecasts can be off. By a lot. Most of them rely on a reversion to historical average valuations, which doesn’t always happen in a timely fashion (who knows, maybe not ever all the way back?). Forward-looking bond return forecasts are made differently, and more likely to be kept within a tighter range. I sitll believe in simple diversification between stocks and high-quality bonds.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Speak Your Mind