Roth IRAs are popular and powerful, and while they have an earned income requirement, they don’t have a minimum age requirement. As long as a child has “official” earned income, they can contribute that into a Roth IRA (technically a Custodial Roth IRA as a minor, with full rights when they turn 18).

There have been various tips floating around on how parents can help “support” the creation of earned income for their child. There was even a now-defunct website called 1417power.com that would “hire” your kids to take surveys online (of course, the parent had to “hire” 1417power.com first…).

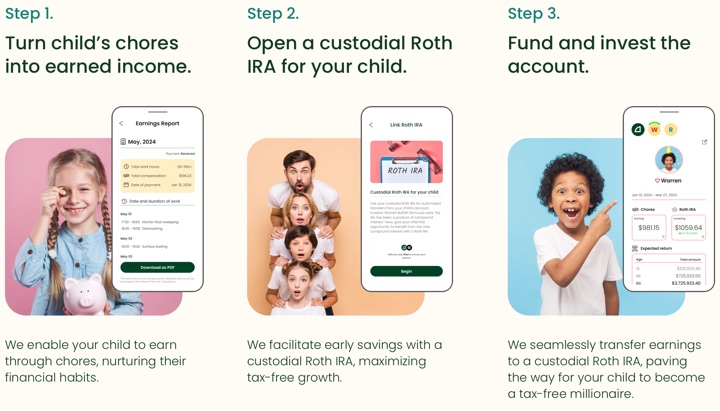

A new app called Halfmore can now facilitate the creation of a nice paper trail between parents as employers and children as workers. They promise to turn chores into a Roth IRA balance. Based on their screenshots, examples of such chores include floor sweeping, washing the dishes, surface dusting, and plant watering. The screenshots also suggest a pay rate of $15 to $16 an hour.

For chores to be recognized as legitimate sources of income, your kids should be paid for tasks you would typically hire another neighborhood kid or a nanny to do (rather than for regular family chores). They should also be appropriate for your child’s age and abilities. Examples include cleaning the garage, mowing the lawn (without a machine), and babysitting. The work must be real, and the wages should be fair.

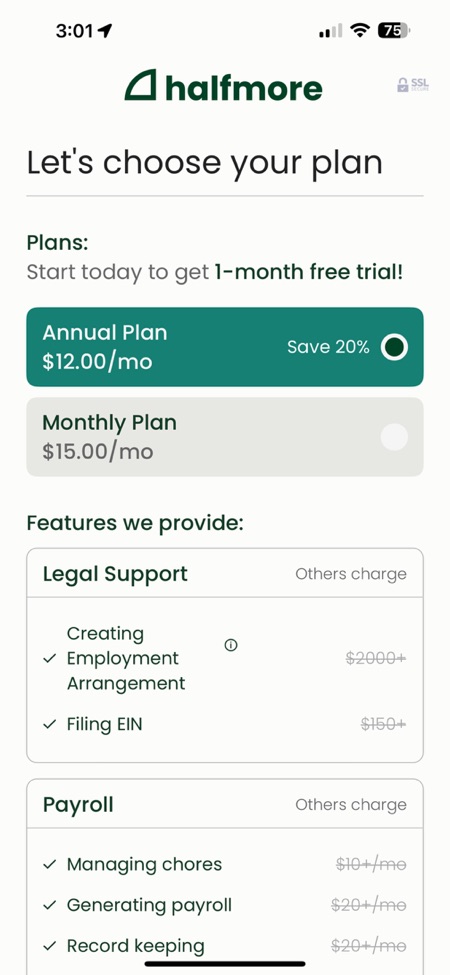

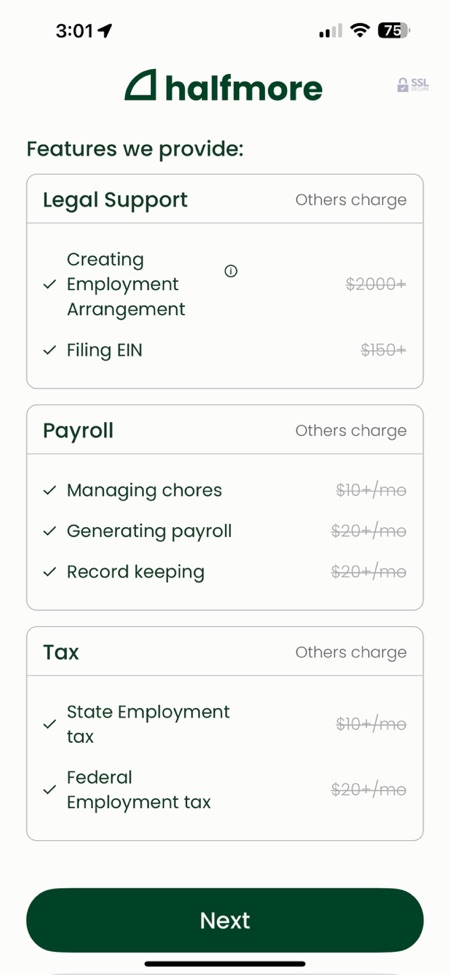

From what I can gather through the limited information on their website (I had to register to get more details), this is what they offer:

- They will help you file for an EIN from the government, so you are registered as an official household employer. This is basically the type of thing you should do if you hired a full-time nanny.

- Through the app, you can track the completion of chores and manage payroll for your children. For example, the washing of dishes can be marked down as 30 minutes of work.

- They will prepare work documentation for IRS income tax filing and record-keeping requirements.

- They will help you navigate Federal and State employment taxes.

- They will help open a custodial Roth IRA for you at Fidelity or Schwab, and transfer money into that account.

The cost is $15 per month or ($144 per year). Their FAQ says this covers up to three children (another place on the website says up to five children). You could file for an EIN, track chores, and open up a custodial Roth yourself for “free”. You are essentially following the same steps as if you were hiring a full-time nanny as a household worker. But if you make enough money such that you are considering this scheme for your kids, then your hourly rate is probably high enough that the convenience factor makes this a reasonable fee.

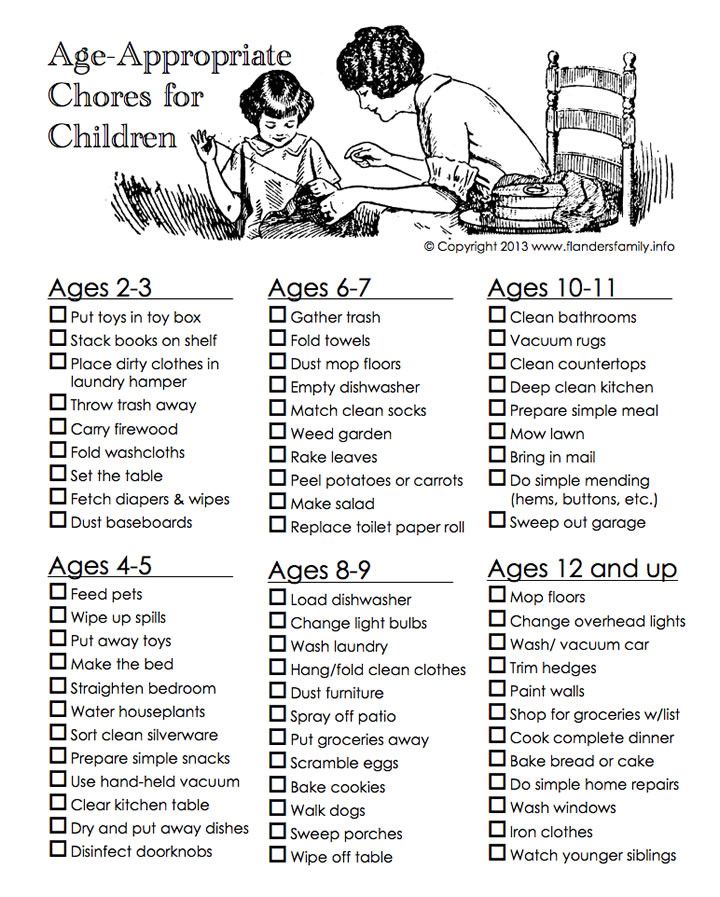

If you need more chore ideas, here is the Montessori Chart of Age-Appropriate Chores For Kids that keeps floating around like a meme:

Looking through my archives, I realized that I have already written about “Roth IRA for Kids” in 2007, 2012, and 2019. My eldest child is in middle school now, and I’m still working on how to best teach them about money. I can see a matching program later on in life when they have a real job from an outside employer. But right now, I don’t pay them anything to do their chores. Chores are not a job, they are a responsibility to their family. They can’t decline their chores by declining the money. Maybe I’ll pay for extra jobs around the house, but I think it’s gonna be a stretch for that to add up to thousands of dollars a year.

If you already plan on gifting your child money anyway, this might be a more efficient method. For me, I already tell them that we spend a lot of money on their education right now, and that is our “gift”. I am already paying plenty for tutoring, swim lessons, tennis lessons, STEM camps, etc. Not to mention who knows how much college will cost! I suppose I just feel like this is too far down the list. Maybe my attitude will change later. Maybe I’ll just let them have the sense of accomplishment from funding their own retirement accounts. 😁

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Interesting, but looks like a lot of work overhead and cost for a simple thing.

Anyone can create a Roth IRA for their child. The work is in recording the earned income over time legitimately and then filing appropriately. Personally, I have doubt in trusting a new app to both be there in the future and to do it right in the short term.

In my state, children can work at 14 (with the proper paperwork submitted to the proper government office) for minimum wage. Them working on the weekend at a religious school (as a classroom helper) enabled our contributions to a Roth IRA on their behalf.

Since it is a Roth the money would be after taxes. Would your child have to file and/or pay income and payroll taxes?

Additionally, I believe you can create and fund an IRA (Roth or traditional) for a non-working spouse. If that’s correct, can you simply not do that for your children?

https://www.irs.gov/businesses/small-businesses-self-employed/family-employees

Thanks Jonathan! I’m having a hard time understanding the first point because it sounds like it negates itself

>Payments for domestic work in the parent’s private home: Are not subject to income tax withholding unless the payments are *for domestic work in the parent’s home.* [emphasis mine]

So they are?

My understanding is yes, you need to do tax withholding in that situation (domestic work in parent’s home). But no SS, Medicare, FUTA.

…but I also think kids can earn up to $1,xxx (too lazy to find it again) with no income tax.

No, the non-working spouse exception does not apply to children.

Custodial taxable account is more flexible since you can withdraw everything anytime, it’s 0% capital gain tax as long as it’s in the lowest bracket. Unless parents plan to give money much more than that bracket, else custodian IRA is a waste of time since earnings can’t be withdrawn easily.