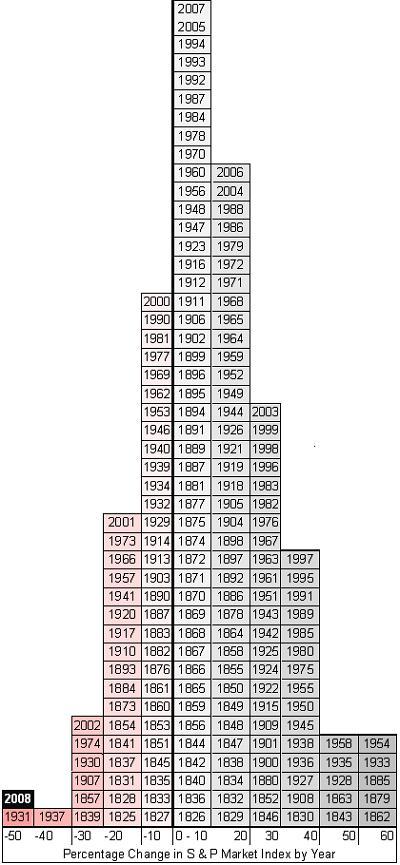

Here is a chart that plots out the distribution of annual returns of the US stock market as measured by the S&P Market Index*. Guess where 2008 is so far?

This chart does a great job to fix the assumption that some have that the 8% or 10% annual returns we hear about come every year. Nope, those are just historical averages. Sometimes we lose 40% or more, and sometimes we gain 40% or more – in just one year! So you can’t say today that it will take X years at 8% per year to get back to what you had before. It could take longer, or it could take a lot less.

* The source for this data is a bit vague since both the S&P company and the S&P 500 index did not exist in 1825. Most sources quote Value Square Asset Management, Yale University. I found it via Daily Kos through Bogleheads and Get Rich Slowly. Here is another similar graph. It is not clear if the chart is based on total annual return, or simply a percentage change in price each year, but it looks like the latter. This paper (also from Yale) with data from 1815 to 1925 might be related.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

While I agree with you that 8% is roughly a mean yearly rise, one should note that the extreme years (in both positive and negative) often occur together. 1931 was one of the worst losers, while 1933 was one of the best gainers. Oh, look… there’s 1935, 1928 and 1936 on the high side. Who’s on the extreme low end? Why, 1930, 1937.

The huge drop in 1929 occurred at the end of the year, with a decent run-up preceding.

This is all probabilities. If you can handle the swings, and want to hold, realize that right now it’s a -gamble-, not an investment. Sure, sure, on the average over time the market seems to have gone up. But it could just as easily go down, way down, from here. Investing should not be about gambling. It should be about taking measured (and known) risks. The risks right now are not known. government action tilts the balance from day to day. Revelation of bank balance sheets could go either way. It’s a gambler’s market right now.

Someone last thread said you have to be in to catch the ‘roaring’ market once it turns, or you’ll miss out… whatever that means. Yeah it may roar, but how will you know whether to get out after a strong roar (ie. will it fall back to a lower low?). It is simply NOT prudent for a cautious investor to remain in the market at this point. Want to gamble and catch the rocket? Go for it, but understand you’re gambling, and your rocket may turn into a knife.

It’s fun. I’m glad to be around for this kind of action, and I’ve even bought a few companies recently. But I realize it’s in no way an “investment for the future”, or any other such delusion. It’s legalized gambling.

If you’re buying for the eventual return to mean-market behaviour, wait it out. You don’t -need- to try for the 50% gainer year. And not trying to catch that coin flip may save you from catching the 50% loser.

Cool chart. I also question the source of the data (“S&P index” didn’t exist back when some of this data is from I don’t think). But it is a neat way to present the data. That paper link you gave is great.

Also the current value is -39.38% YTD to Dec 10th

http://www2.standardandpoors.com/portal/site/sp/en/us/page.topic/indices_tmi/2,3,2,2,0,0,0,0,0,0,0,0,0,0,0,0.html

On Dec 4th it was down 43%

It might appear to some at first glance the market is down over 50% this year in fact above -50 they mean (a return of -40.001 to -50%)

Hmmm…. kinda resembles someone giving us the finger, doesn’t it? With 2008 forming the knuckle of a thumb… 🙂

is it me, or does it look like the market is flicking us off? either way, it sure feels like it anyways 😉

I started investing in 2001. The market has been flicking me off for a while now! (Look where 2001 and 2002 are…)

Great chart. Noteworthy that two other years in this decade did poorly and that was 2001 and 2002.

They’ll probably need to create a new section for next year, the 60-70 bracket, when the market comes back from this year. (I’m an optimist.)

Jonathan, I would kill to have started investing when you did (I started the beginning of 2005), you started during the last recession. You are going to be set for life since you’ve been using your prime compounding years investing when stocks are largely undervalued.

Things can only go up from here. All, throw in as much money as you can in now into as much of a stock skewed portfolio as you can and you’ll be set.

It would be interesting to hear what people were saying in 1973 and 1974. That was right after the first oil embargo. Before then, I remember gas being 19 cents a gallon at the discount places. I was a freshman in high school and I did not pay much attention to the market or finance. Many readers here probably weren’t even born yet.

At times like these I like to go an review some of the books I have read in the past like “A Random Walk Down Wall Street” or “The Only Investment Guide You Need” or even “The Tightwad Gazette”

Hmmm Maybe a better idea is to sell Senate seats 🙂 nahhh….

I wouldn’t count on the market rebounding that fast or that hard, or that we can only go up from here. We’re probably in for a long, nasty, churning spell (look at how many years in the 1930’s are on the left side of the chart). But I think if you want to hunt for bargains, there are some great opportunities out there.

Jay,

While you point out that we won’t rebound fast and hard by pointing to the 1930s on the left side of the chart, don’t forget about 1933 & 1935 on the RIGHT side… If anything, this chart shows that the market does rebound fast and hard when it comes back. Those two years both had +50% returns.

A really, really awesome site to look at charts for this is:

http://www.djindexes.com/mdsidx/?event=showAverages

Just click on the decades on the left side to see just how hard and fast the market tends to rebound after drops like this…

Jim Cramer was on CNBC last night, suggesting that the “game” (stock market) is rigged. He is calling it a ponzi scheme.

True. But a -50% year followed by a +50% year doesn’t get you a wash – you are still down 25%.

But it’s important to note that from the top in 1929, until the “bottom” in 1933, we’re talking almost 4 years of downward sliding. The “explosive” rebound in 1933 really just erased 1932’s losses. If you’d picked a your bottom and invested at around 150 in 1931, you’d have had to wait nearly 15 years for a permanent gain in your investments via a buy & hold strategy. Assuming you’d invested in a broad-based index like the S&P.

I’m not saying you shouldn’t swoop in and buy stocks while they are on sale. I’ve done that recently myself. But I think there’s a really good chance we’ve not seen the bottom yet in the overall market, one that we may not see until 2009 or even 2010. At this point, I don’t know that anybody knows. The fundamentals of our problems are unchanged, and the governments are mainly throwing gasoline on the fire at this point.

So tread cautiously. My feeling is that buy & hold is a dead strategy for the next decade, but there are some INCREDIBLE opportunities out there for those who can invest a little more nimbly and think outside the box.

I think to some degree he is correct. And here’s the problem:

A large demographic bulge in the population of the United States – the baby boom – is now approaching retirement. They’ve just witnessed (for many of them) their retirement money, which only barely recovered from the 2001 recession, collapse to half its value. They do not have time to “buy and hold” for a long term. A lot of that money is leaving the market, and it is not coming back – at least not directly. A lot of them are shuffling that money out of growth funds in their 401ks and IRAs into low-yield, “low-risk” funds.

While I don’t see that as the harbinger of doom in an increasingly global economy and marketplace, I do think this will limit our upside growth potential over the next decade in the equities market.

Another thing to remember is the extra pain of the downside. A 50% loss in value requires a subsequent 100% return just to break even. It’s an exponential relationship, and when you get into the 40-50% drop range, it really starts to gets ugly. Just another 10% drop (for a 60% loss) now requires a 150% return to break even. Ouch. Be careful catching falling knives!

Thanks for sharing this Jonathan,

Although, it is a little scary seeing where 2008 is, it is great seeing the distribution like that! I think it is encouraging!

This graph is not a distribution. It is misleading to calculate the mean of this as average return. 50% gain does not offset 50% loss. The negative side of the distribution should have higher weightage than the positive side. In other words, you could start with $100 investment in the first year and find cumulative return until 2008 and then calculate aerage compounded gain per year over all the years and it will be a heck of a lot less than 8%. Wall street doesn’t want average joe to know this and average joe including most wall streeters are too dumb to figure it out. Hence the 8% mean gain number.