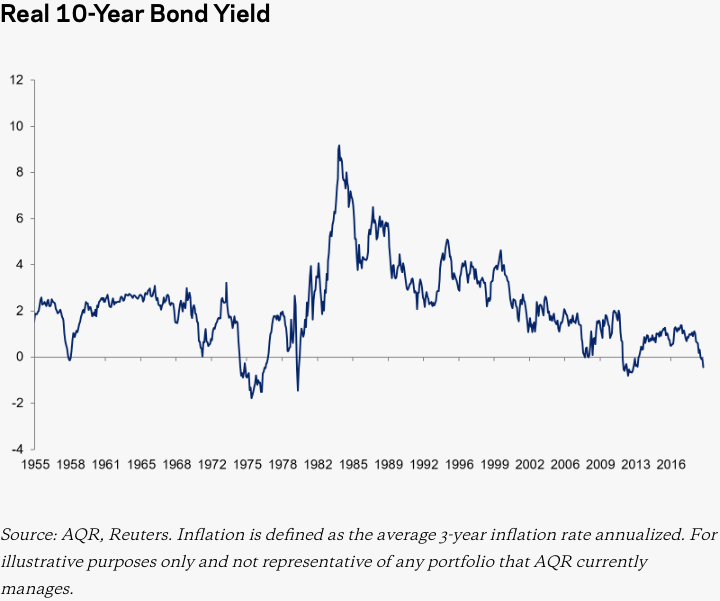

I was looking for a historical chart of the 30-year US Treasury yield that adjusted for inflation, as the yields were much higher in the 1970s and 1980s but inflation was quite high as well. The closest I could find was this chart of the inflation-adjusted (real) 10-year US Treasury yield. (Please let me know if you have something better.)

Taken from Bonds Are Frickin’ Expensive, Cliff Asness of AQR takes the nominal 10-year Treasury yield and subtracts the 3-year trailing annualized CPI inflation. I prefer the use of hard numbers over a forecast.

You can see that in the past, the inflation-adjusted yield has varied quite widely. There have been zero and negative real yields, and there have been really high positive real yields. From a historical perspective, right now bonds do not yield very much and the overall curve is rather flat. The article concludes:

So, the bottom line is, as measured by real bond yield, U.S. Treasury bonds are really frickin’ expensive. Measured by the slope of the yield curve they are really frickin’ expensive. But, measured by the average of these two simple variables, they are 60+ year just about record-low frickin’ expensive. This result is not caused by, but is certainly exacerbated by, the (perhaps) surprisingly uncorrelated nature of slope and real bond yield, thus making both so low and at the same time considerably more surprising.

The usual disclaimer against timing bond rates is thrown in there, but it felt only half-hearted.

I have no plans to sell my high-quality bonds because they have historically been a reliable buffer against stock drops:

- High-Quality Bonds Still Best Antidote to Stock Price Drops

- Stocks and Bonds Asset Class Correlations 2009-2019

Still, it would sure be nice if they actually gave me some positive real return…

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

With due respect to Cliff Asness—who gets quite upset when not accorded due respect (https://www.wsj.com/articles/SB124303417991748685)—the US is no longer an economic island suitable for in vacuo analysis. Look at long term government bond yields the world over. Then decide how frikkin’ expensive our bonds are.

I’ve read a couple opinions to not consider bonds as the alternative to equities, but as the alternative to cash. The bond part of the portfolio is there to smooth the ride and give buffer for rebalancing. If the real rate is positive then you’re doing ok in that regard, albeit it’s a very low bar.

The only way I hold US Treasuries is through ETFs. That said, 35% of my portfolio are individual corporate bonds that have served me well since 2001. But now I find that Corporates are impossibly expensive, go out to 2057 and yields are barely 3.25% and costs are way over par.

Though as Gerry points out, anything is better then negative interest rates (barely).

To me the interesting part of the whole charade is….5 years or so of negative interest rates in Europe have been a total failure. Ten years of rate repression and next to nothing rates in the US and we’re right back where we started from. These policies are a sham, where are the talking heads when the real question is: Why is the global economy in constant need of fiscal and monetary stimulus, even with all the accommodation already received?

Jonathan, bonds have had a monster year and the capital gains on it have been much more than equities. In such an environment why do you still believe you are not receiving positive real return?

Comparing the yield on a bond that you buy today that matures in 10 or 30 years to inflation over the prior three years is meaningless. All that matters is inflation from the date you own the bond forward; past inflation doesn’t influence your return at all.

I understand perhaps using the trailing 3-year inflation calculation as a proxy for the inflationary environment, but still I don’t think it contains much useful information.

You can explicitly observe the real yield on Treasury bonds by looking at TIPS. The difference between the yield on the nominal Treasury and the TIPS is known as the breakeven level of inflation, or the market’s best forecast of inflation over the life of the bond. However, it hasn’t been a perfect predictor of actual inflation either.

But you can always just invest in TIPS and get a real return. 10-Year TIPS yields were actually over 1% late last year, but now they are negative again, which confirms the idea that bonds are quite expensive.

It’s for this that I keep much of our emergency fund in I-bonds. You can only put in $10k per year per taxpayer, but after a few years, that can add up. For us, it’s a great way to lock up and secure our emergency fund.

For investing, I like munies, and I have found several mutual funds that I can invest in munies in to spread the risk and save me the hassle of investing in them on my own. I looked into it, and I found it to be easier to just buy the fund. That might be a mistake, but the yields are good.

There is $17,000,000,000+ of negative yielding debt in the world. If that isn’t a worrying statistic I don’t know what is!

Matador not only paid 2.5% interest, they didn’t drop their rate as the Fed lowered interest rates as SoFi, Betterment, Wealthfront and others did. But, it may have been too good to do, particularly for a startup. I have not received my November 2019 interest payment yet.