This an update for my investment portfolio, including 401(k) plans, IRAs, and taxable brokerage holdings. There have been only a few small changes since my last portfolio update. As always, this is our own personal portfolio and may not necessarily be completely applicable to anyone else.

Asset Allocation – Target vs. Actual

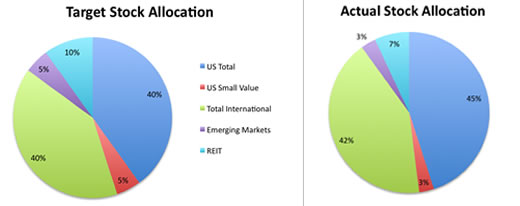

I separate the stock and bond portions for clarity. My target asset allocation remains the same:

Here is my actual stock allocation, where it shows that I am slightly overweight US Total and will need do some light rebalancing.

My actual bonds allocation is not really worth making a chart for… the target is 50%/50% and I have 47% short-term nominal bonds and 53% inflation-protected bonds.

Stocks vs. Bonds Ratio

One way to calibrate your portfolio risk is with the balance of stocks and bonds within your portfolio. A few years ago my stock/bond ratio was 85% stocks/15% bonds, which corresponded to a formula of [Current age – 15]% in bonds. After the stock market plunge in 2009, I felt like I had to keep my stock portion high. Since the stock market has since recovered substantially and with the realization that I am possibly within 15 years of “retirement”, I have started gradually becoming more conservative. I have been adjusting my target gradually to [Age – 10]% in bonds, which leaves me now at 77% stocks/23% bonds. However, I still hold mostly stocks.

Fund Holdings

Here are the actual investments that I am holding to represent each asset class, along with ticker symbols. * denotes selection due to limited 401(k) choices. The only significant change is that I now hold some shorter-term municipal bonds in my taxable account, in order complement my stable value holding and to make tax-efficient room for other stuff in my tax-advantaged accounts like REITs and TIPS. Munis also makes sense due to our current high tax bracket.

US Total Market

Vanguard Total Stock Market ETF (VTI)

Diversified S&P 500 Index Fund (DISFX)*

Fidelity Extended Market Index Fund (FSEMX)*

US Small Cap Value

Vanguard Small-Cap Value Index Fund (VISVX)

Real Estate

Vanguard REIT Index Fund (VGSIX)

International

Vanguard FTSE All-World ex-US ETF (VEU)

Emerging Markets

Vanguard MSCI Emerging Markets ETF (VWO)

Short-Term High Quality Bonds

Vanguard Limited-Term Tax-Exempt Fund (VMLTX)

Stable Value Fund* (3% yield on past purchases, 1.8% on new)

Inflation-Protected Bonds (TIPS)

iShares Barclays TIPS Bond ETF (TIP)

Individual TIPS securities

The overall expense ratio for this portfolio is in the neighborhood of .20% annually, or 20 basis points. That is a much lower hurdle to overcome than the average mutual fund expense ratio of over 1% annually.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

and how do you achieve this portfolio mix?

do you buy several separate etf’s or is there an etf or fund that already has the portfolio mix?

Jon, what is your opinion on having international treasuries or international TIPs (for example, WIP, BWX, or IGOV) as part of one’s portfolio?

Thanks.

how did you arrive at a bond percentage of [age minus # of years to retirement]? I had heard of your age as a proxy for bond allocation percentage, but never the adjustment for years to retirement.

@James – I buy each separate ETF at Vanguard. There is no commission fee to buy or sell them there.

@RP – I don’t have a strong feeling either way about them, but international TIPS should track international inflation rates, no? Are those all currency-hedged? I remember researching them before, but forget exactly why I chose not to use them. Perhaps cost was part of it. I suppose you might want to hedge credit risk across countries, although I don’t feel the need to currently.

@Scott – Please check out this post:

Deciding On The Stocks/Bonds Ratio

It’s part of a collection of posts about investing here:

https://www.mymoneyblog.com/my-money-blogs-rough-guide-to-money

I’ve worked in the financial services industry for some time and am constantly amused by the variety of approaches to asset allocation. The brokers in my first office had some colorful charts created by the firm to use in sales presentations. They showed a mix between all asset classes would reduce volatility for a portfolio and produce higher returns than any one asset class. Then after the sales pitch the broker would arbitrarily come up with an optimal allocation.

There’s a company called Riskalyze that claims to have a mathematical formula for objectively calculating a person’s risk tolerance and matching it with historical market volatility across asset classes to create an optimum portfolio allocation. Full disclosure: I know the CEO personally and may be a bit biased.

WIP: I think it tracks an index that tries international treasury-inflation-protected bonds. I don’t believe that it is currency hedged.

WIP+BWX: i just checked and you are correct. Expense ratios are at 0.5%. pricey for bonds. IGOV is at 0.35% though. not cheap, but not terrible.

I was asking originally because I was considering diversifying bonds internationally (since many of us do this in our equity portfolio). Still not sure if I want to do this. right now. I kind of do the same thing as u with 50% TIPs and 50% intermediate treasuries.

I definately have a large portion of our bond portfolio in intl bonds – they are worth looking into and generally have a higher yield. If you have an intl stock position….why wouldnt you have an intl bond pposition? While i am a fan of etfs the mutual funds for intl bonds appear to be more mature/strategic as well as getting better FX exposure (something i wanted!)

How did you decide on your asset allocation within stocks? Why 45/45 Domestic & International, 40/5 total market & emerging/small cap?

willy j,

would you care to share some international bond fund names?

thanks

Srian

I am curious about your Veu + Vwo. Given that Veu includes emerging markets, why add more? Are you intentionally overweighting them? Why not opt for something Veu doesn’t cover, such as foreign small caps?

Thanks!

Jon, have you given any thought to allocating some assets to one of the ETFs that is indexed to the actual price of gold or other metals? I know all the historical data indicates that gold, silver, etc. has not outperformed stocks, but I do wonder if “this time is different.” I am toying with the notion of maybe putting 1% to 3% of mine is something like i shares ETF (IAU).

@ srian

Here is my list…. if you find any on your search please do share – you would think there would be more global bond funds/etfs out there.

My current portfolio includes:

DIBRX – Dreyfus International Bond

PFBDX – PIMCO Foreign Bond

Others I have on my watch list / considered:

LSGLX – Loomis Sayles Global Bond…… objective does not spell at least 80% in non US currency…. but consistency outperforms the ones I am in

FNMIX – Fidelity New Markets Income Fund….. made positions in global funds first.. this is a emerging mkt focused fund but has been doing well…. might be out of steam? ETFs seem to be better for emerging mkt bonds

willy j,

Thanks for those names. I will have to look into those. The ones I know of are

RPIBX – TRowe Price International Bond

TGBAX -Templeton Global Bond (this one is good but has a high initial limit $50K which is a limitation for me). Templeton has some other classes and offerings in this space but the front loads are a big turn off

On the emerging market side I agree that ETFs are a better option (ELD, EMLC being the two that I know of)

I dont own any of these but looking to add some developed (non-US) and emerging bond exposure in my portfolio

Jonathan,

It’s very hard for me to believe that you do not invest in individual stocks. My limited experience (12 years) tells me that well researched individual companies in your account create far more superior results that your average/above average fund. I’ve been investing in individual stocks for 12 years and beating most market indexes/funds hands down.

May be your risk tolerance is low but with the financial IQ you have you could do very well with individual stocks.

Jonathan,

for ex-US stocks, you use a combo of VEU (0.22% exp ratio) for ex-US & VWO (0.22%)

why not use a combo of VEA (0.12%) & VWO in whatever combo you desire to meet your desired mix of developed vs emerging? This is what I do to implement the ex-US stock portion of my asset allocation.

My sense is that although VEU may have a benefit of being broader, for example having Canada stocks, this benefit is severely outweighed by the VEA’s cheaper exp ratio.

Jonathan, am I missing something obvious about VEU v VEA?

Or perhaps this is an issue of “401k lemonade”, eg you have access to VEU & not VEA in your 401k?

also fyi since you invest in the REIT asset type.

I randomly noticed Vanguard offers a ex-US REIT VNQI (0.35% exp ratio) as well as the US REIT VNQ (0.12%) aka your VGSIX.

@Ken in Georgia – I don’t own any gold, I just don’t see it being a long-term investment for me. I don’t see anything wrong with it as a small portion that you rebalance, however.

Re: Foreign bonds – Diversification sounds nice, but bonds are primarily for safety for me. They also still cost a bit too much. I take my risk on the equity side, where the interests are aligned, a la Swensen.

@LongTermBull – I do have an extra ~5% of my portfolio in individual stocks, and they’ve done okay, but I don’t have the belief that I’ll consistently do that much better over time.

@Cabron – You make a good point, but I am consciously overweighting Emerging Markets. I do believe they, especially Asia, will create higher overall returns over the long term, but with lots of volatility.

I think I will add foreign REITs one day, I just wish I didn’t have to own yet another ETF to rebalance. An all-world REIT ETF would be nice. 🙂

Jonathan said “..I am consciously overweighting Emerging Markets…”

I still don’t see why you could still do that by using VEA instead of VEU to save on expense ratio. You could overweight Emerging Markets (VWO = %100 EM) as much as you want. You could allocate your ex-US stock slice of the pie 50% VWO 50% VEA (or whatever combo you wished to).

Again I’m not trying to tell you what to do. I’m trying to perhaps learn from you – your expertise exceeds mine on these Asset Alloc & chosing funds topics. I’m trying to “debug” my thinking, to check to see if there is a reason that VEU is superior to VEA to an extent that is “worth” its higher expense ratio.

@Cabron – You could certainly do the same with VEA and VWO. It would save some basis points. VEU does include a few extra countries if I recall that VEA+VWO might not cover like Canada (something like 7% of VEU).

I think I mentally prefer having the “whole” area covered, and then adding a little weighting. Just like Total US already has the Small Cap Value stocks included. I like the symmetry of having the my VWO and VISVX holdings be the same size, which is pretty illogical I must admit. 🙂

In my case, there’s also capital gains within VEU that I want to avoid incurring from selling, unless I want to have multiple holdings.

Thx for the info Jonathan.

“there’s also capital gains within VEU that I want to avoid incurring from selling”

Most of my assets are in tax-sheltered/IRA accounts. I forget that many folks have a big portion of their “pie” in taxable accounts, & hence there is a much higher “switching cost”.

Actually, maybe you could use the VEU v VEA as an example of how taxable investors can do a “wash sale”. I don’t understand this idea, but would like to understand it for future possible use.

Jonathon – I’m curious, why did you decide to “overweight” Small Caps by holding 5% in that fund? it is my understanding that Small Caps are included in the Total Stock Market fund. Thank you!

Do you buy several etf’s? Am wondering how you have the portfolio mix.I learned a few tips from this post