Update: $100 bonus is expired. Wanted to report that I am had a bad experience with LFCU after being locked out of my account for over a week. Phone hold times were very long, I got routed to a service that promised to call me back, and then never called me back. E-mails also went unreturned. Maybe it’s just me.

Original post, may be outdated:

Lafayette Federal Credit Union (LFCU) has a respectable history of offering competitively-priced banking products. I recently joined and here is a quick review of their current promotions and the application process. Highlights:

Lafayette Federal Credit Union (LFCU) has a respectable history of offering competitively-priced banking products. I recently joined and here is a quick review of their current promotions and the application process. Highlights:

- 2.02% APY Checking account on up to $25,000 balance (details below).

- $100 bonus for new members (details below)

- Competitive CD rates: 7-month at 0.70% APY, 3-year at 1.01% APY, 5-year at 1.26% APY

Membership eligibility. You can view your membership eligibility options here, including working/living in the Washington, DC area. Anyone nationwide can join LFCU by joining the Home Ownership Financial Literacy Council (HOFLC) for a one-time $10 fee.

Account opening process. I went to the HOFLC.org website and paid my $10 to join. (I hope to spend more time exploring their resources later.) I had to attach a screenshot of my membership approval e-mail as part of my LFCU application. The LFCU application was finished completely online. I also had to upload a photo scan of my drivers license. My application was approved after a couple of days.

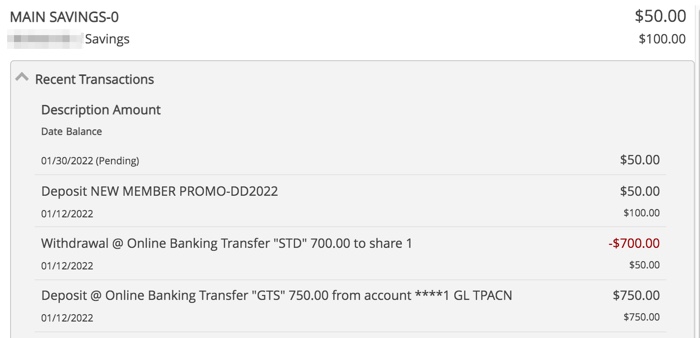

During the application, I was able to charge my initial opening deposit up to $750. This was classified as a purchase on my credit card (worth $15 at 2% cash back). Note that you must keep $50 that is “untouchable” in your Share Savings account as long as you are a member, which is a bit higher than that of other credit unions (usually around $10 to $25).

I applied through this $100 bonus page which includes promo code DD2022. (Update: I honestly can’t remember where I entered the code. You can however secure online message them directly through the membership application portal and confirm that you are signed up for this promotion. I received such a confirmation message promptly.) I must open a checking account and set up a $500+ direct deposit, and I can’t close the account within the first 6 months. Details:

Members who open a checking account and initiate a qualified direct deposit to Lafayette Federal Credit Union will receive a $50 deposit to their savings account. An additional $50 will be awarded after first direct deposit which must be deposited no later than 45 days after account opening. Cannot be combined with any other new member offers. Qualified direct deposit is a recurring direct deposit of a paycheck, pension, Social Security or other periodic payment of at least $500 into a checking account on a month-to-month basis made by an outside organization or agency. Must be eligible for membership. If account is closed within first 6 months, initial $50 promotional deposit will be deducted from account.

The first $50 showed up quickly:

Checking account 2.02% APY details. With the Checking account, they have “2% for ’22” promotion which pays 2.02% APY with a qualified monthly direct deposit of $500 or more on balances up to $25,000. The checking account otherwise has no minimum balance requirements or monthly maintenance fees.

To earn the 2.02% APY3 bonus rate, member must maintain at least one (1) qualified direct deposit of at least $500 per month. 2Qualified direct deposit is a recurring direct deposit of a paycheck, pension, or Social Security periodic payment of at least $500 into a checking account on a month-to-month basis made by an outside organization or agency.

If I keep $25,000 in there at 2% APY, that’s $500 of interest over a year. That’s also $275 more than it would earn in a 0.5% APY savings account. You can use that metric to judge if it is worth your additional efforts. That rough calculation also assumes both those rates stay constant over the next year.

So far, LFCU has been pleasant to work with and my questions were answered quickly and courteously. I hope that they continue to be aggressive in their banking products.

The Best Credit Card Bonus Offers – October 2024

The Best Credit Card Bonus Offers – October 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - October 2024

Best Interest Rates on Cash - October 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

What were you able to get to count as a direct depost?

is this hard or soft pull?

Is it hard or soft pull?

I did not receive any notification of a hard pull on my various credit monitoring services, so I believe it is a soft pull. I also didn’t sign up for any overdraft or line of credit.

It seems that they automatically sign you up for overdraft protection.

I suspect there there is no way to be certain a fund via CC is treated as a purchase.

I did this once when i opened an account with a bank and it was treated as a purchase. Couple years later when i opened an account with same bank using same credit card to fund, it was treated as cash advance and i got slapped a 5% cash advance fee.

It would be great to use this to try to meet minimum purchase for my CC, but …

You can call your credit card company, many allow you to set the cash advance limit to zero or low enough, so if it tries to go through as a cash advance it would simply be denied.

Agree. Excluding Wells Fargo, I called and non of their cards allow it

Did you have to use a “true” direct deposit (similar to requirements by HM Bradley) in order to qualify?

Thanks.

Wondering if a biweekly direct deposit of $250 will meet this criteria?

“To earn the 2.02% APY3 bonus rate, member must maintain at least one (1) qualified direct deposit of at least $500 per month. 2Qualified direct deposit is a recurring direct deposit of a paycheck, pension, or Social Security periodic payment of at least $500 into a checking account on a month-to-month basis made by an outside organization or agency.”

I have the same question. I can hit $500 but not on a single payroll deposit.

I have experience on other bank/CU’s that comibine multiples to satisfy the req.

where do we enter promo code? I dont see any prompt for it. I followed everything but did not see anything for promo code.

Someone else mentioned this as well, I honestly can’t remember where I entered the code. You can however secure online message them directly through the membership application portal and confirm that you are signed up for this promotion. I received such a confirmation message promptly (and the first $50 promptly as well). Seems strange to offer a promo code with no place to enter it.

Thank you

I had to contact Lafayette regarding promo. The application does not provide anywhere to add promo. Does anyone know if ACH from other institutions will count as DD. I am going to try Ally and see if that works.

Stay tune!

How long until you get your account numbers? I got my membership number but have not received any other email or account information to register online.

My turn around was within 24-48 hours. Just call them and perhaps they can do it on the phone. I sent a secure message to verify promo on my account. They responded in hours and promo was applied.

Thank you. I’ll do that.

Just wondering if an ACH qualifies as a direct deposit.

I did an ACH transfer from one of my brokerage accounts (dividends are my paycheck, so I see nothing wrong with that, haha) and it appears to have qualified. I have gotten both $50 + $50 bonuses now. It’s hard to speak for all ACH transfers though.

Which brokerage company in case my Ally account doesn’t work.

Thanks

Ally Bank triggered my $50 bonus.

Jonathan, have you received second $50 and what triggers checking account to get 2%. I am still at the lower interest rate.

Yes, received 2nd $50 bonus, but I am also still showing 0.03% APY and not 2%. I have a sent them a message inquiring about it.

Thanks! What triggers the second $50, another $500 DD? I also sent them a secure message inquiring about the higher rate.

I’m not sure exactly how they are tracking it, but I got first $50 after my verification deposits (less than $1) and second $50 after $500 direct deposit. This is what they said to my inquiry:

Thanks, yes I got same response but received $50 only in Savings.

Did you receive both of your $50 deposits in your savings account?

I received $50 in savings early on marked “DD2022 new member”, and then $50 in checking after my $500 direct deposit marked “DD2022 promo funding”.

Thanks! I stand corrected, my Ally apparently didn’t trigger the first $50, it was new membership. I am going to attach my Schwab brokerage account and see if that triggers the second$50. Which brokerage account did you use?

I have had good luck using Fidelity and TD Ameritrade across many different direct deposit requirements.

Sorry to belabor this but I linked my Schwab account and it says “Moneylink”.

Did your brokerage connection state Moneylink?

My checking $50 deposit isn’t coming thru.

Thanks!

Was $750 the max you could deposit via a credit card?

Yes

Jonathan, which broker triggered the DD for you?

They wouldn’t accept the ACH from Ally as a direct deposit. Will have to see if I can still get a TD Ameritrade transfer in and accepted as a direct deposit.

I can confirm that, for those of you using Quicken, this shows up as “Lafayette Federal CU”, which lists the same web site as the subject of this post. So you can sync transactions automatically, as I always prefer to do.

So does the $50/$50 bonus require that the direct deposit be made into the *Savings* account? It sort of sounds like that, but I’m not sure. It sounds like the 2% interest is a separate thing, which _also_ requires direct deposit into the *Checking* account?

Thanks.

App is pending!

Do we know what the ACH transfer limits are? I’ve never had a problem with Alliant CU, even for large ACH transfers in the 5 digit range, but I’ve gotten hosed by some smaller FinTechs where it might be 2,500 a month or whatever.

I wasn’t able to track down any obvious answer online; Any ideas?

Thanks!

They have told me my Ally and Schwab do not count toward second $50 bonus.

First bonus posted as new customer.

Deposits need to be made in checking. It does state other qualifying deposits beyond pension and payroll etc in T&C.

I am escalating this!

Update, complained about not receiving second $50 especially since terms and conditions of what qualifies as direct deposit. Kevin Fritz took care of me. They think during the transition of their accounts some promos may have dropped off.

So for what it’s worth, if you CC fund, as I did, and it gets declined as possible fraud (by HMBradly in this case), LFCU cannot charge the card afterwards when the account is already opened, and there’s no way in the portal to fund with a card. Which isn’t really surprising. Or at least, the rep couldn’t find any evidence in her system that this is possible.

I suppose I could escalate to a manager, but it isn’t that important. (There aren’t many venues to get money _out_ of HMBradley without nuking your next quarter; This would have been one; Coin deals is another.)

I asked to confirm about the promotional code to verify it is on my account, and someone has to call me back about that. So I’m not sure the front line people can necessarily help with much of anything? Friendly though and didn’t have to wait on hold.

Already have ACH accounts linked! I actually did this so I can use this as my new primary account, so thanks for that. Alliant has been good for 10 years, but their rates haven’t been competitive for YEARS now on checking or savings accounts.

I am having interesting experience with their direct deposit requirement for the $50 bonus and their 2% rate. I thought I didn’t meet direct deposit as I never got the $50, however I recently found that my account got credited with the 2% dividend for the quarter.

After talking to customer service via secure messaging they told me the following:

“In order to get the 2% you must have an ACH of $500 or more come into the checking account, which you do. That ACH does not qualify as a direct deposit that is why you did not receive the $50 for the DD2022 promotion”

I do have an employer DD setup, but I still haven’t gotten a bonus in a month now. Neither part of the $50. I sent an email and was told that I did sign up for that promotion, so I’m going to email again and try to get it sorted.

Otherwise, the experience has been good; I setup ACH with my various accounts, I’ve been transferring money without incident, it syncs properly with Quicken, and I figured out how to enable electronic statements, which is a bit wonky.

I’m not sure if free checks were part of the deal; but I haven’t gotten any yet. You can order some online, but they aren’t free. I’ll keep my Alliant checks for that, I guess.

fwiw did finally got both parts of the bonus, after an email two weeks ago asking to confirm that I qualified and whether this is gonna happen or not.

A family member opened an account, got approved, but did have to call to finally get the account opened, so I can confirm some sluggishness here.

I hope I don’t get locked out; I spent a weekend moving all my stuff here. Oops.

Just FYI their password reset system requires you to know your username, not just e-mail, so I had to talk to a human to find my username (which they didn’t allow to be one of my usual usernames and then they made me change it again when they switched backend IT systems). If it just required email, I could have probably reset on my own. So be sure to write down your username and not forget it like me! Just made me appreciate Ally Bank more – they post their hold times on the website (rarely more than a few minutes) and has humans available 24/7.

If you push money from the Lafayette side, there is a 10k outbound ACH transfer limit I just discovered. fwiw.

(SoFi has ridiculously large limits, and as rates rise, I’m tempted to move my money there as my primary account.)

One year interest penalty on 18 months CD for early withdrawal! That is way higher than average. Most are like 180 days. way way out of line

It is terrible customer service at Lafayette Federal Credit Union. I tried to call the member service and holding over 4 hours, still nobody answered. And they do not have other number can reach if you have any questions.