Home ownership continues to be a goal for many people, but downpayment requirements also keep rising with housing prices. I previously posted about Unison, which offers downpayment assistance in exchange for a percentage of any future upside (or downside) on your home. Their example states a 40% cut, although it will vary with the size of assistance. Unison also charges an origination fee of 2.5% of the downpayment assistance.

Home ownership continues to be a goal for many people, but downpayment requirements also keep rising with housing prices. I previously posted about Unison, which offers downpayment assistance in exchange for a percentage of any future upside (or downside) on your home. Their example states a 40% cut, although it will vary with the size of assistance. Unison also charges an origination fee of 2.5% of the downpayment assistance.

Landed offers a similar shared equity down payment program, but restricted to employees of selected school districts, colleges, and universities in high-cost areas. They also offer up to a 10% downpayment assistance (i.e. $50,000 on a $500,000 home), but they only ask for 25% of future upside (or downside). Instead of charging an origination fee, they ask you to use a real estate agent in their network, who have all agreed to pay Landed part of their commission (0.75% of purchase price). You can use your own agent, but you’d still have to pay that 0.75% fee. That’s a clever trick to avoid any upfront fees.

Here’s another important twist: You must agree to stay with your current employer for at least two years after buying your home. I believe that if you don’t, you will need to pay Landed back within 30 days (even if you don’t sell the home). You may also need a certain amount of time employed with the school. The idea is to improve employee retention in these high-cost areas.

Currently, Landed covers K-12 school districts, colleges, and universities in California (San Francisco Bay Area, Los Angeles Metro Area, and San Diego Metro Area), Colorado (Denver and Boulder metro areas), the state of Hawai?i, and Washington (King County Metro Area). Right now, you can get up to $120,000 in down payment support. They plan on expanding to other high-cost areas including the East Coast.

Unison vs. Landed fee comparison. Let’s say you have a $500,000 house. The Unison numbers are based on the stated example on their website. Unison might provide $50,000 assistance (“co-investment”) and you put in $50,000, and that is the 20% downpayment needed. If the house appreciates by $100,000 and is sold for $600,000, then Unison would get $40,000 of that appreciation (plus their original $50,000 back) and the homeowner would get $60,000. If over time the house doubles in value to $1,000,000, then Unison would keep $200,000 and (plus their original $50,000 back) and the homeowner would keep $300,000 of the gain. The upfront fee would be $1,250 (2.5% of $50,000).

Since Landed only asks for 25% of the upside, the numbers would be $25,000 on a $100,000 gain ($15,000 less than Unison), and $125,000 on a $500,000 gain ($75,000 less than Unison). There is no upfront fee if you use their real estate agent, but Landed will get $3,750 (0.75% of $500,000).

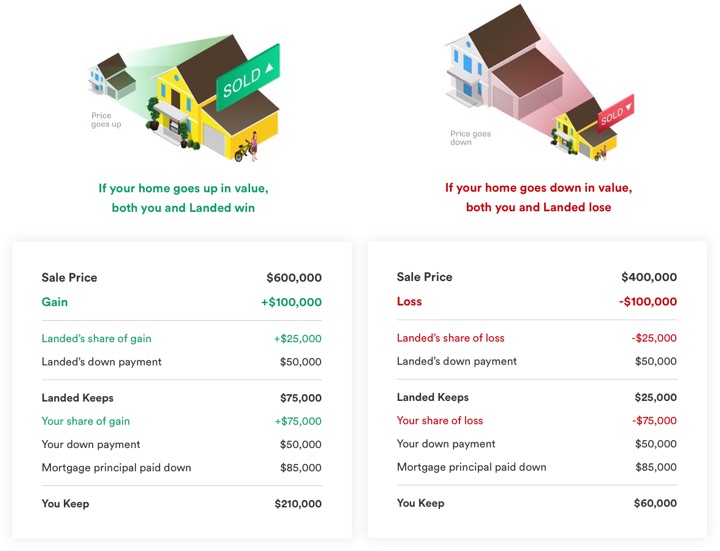

Here’s a separate breakdown example from Landed for a $600,000 home purchase, assuming you sell after 10 years of mortgage payments and either have a $100,000 gain or loss.

I know that some people will scoff at say “who would accept such a bad deal and give up all that home appreciation?”, but for many people the idea of scraping up $50,000 is many times more imaginable than coming up with $100,000. I’m not saying it’s a good idea, but I definitely understand the demand and think these programs will be popular as a result.

It is interesting that both “shared equity” companies have the same basic concept, it’s just the specific implementation that is different. Landed focuses on a group that tends to have stable employment and potentially solid retirement benefits but low base salary. It’s also a group that people want to see living in the neighborhoods that they work in, like firefighters and nurses, and thus can get cheaper funding from non-profit sources. However, this would also mean that if the concept gains traction, there is room for competition to lower the costs for everyone else.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Affordable housing is a problem for many metro areas and the lack of it is part of what drives inflation. When service workers (including educators) cannot find affordable housing near their workplace, they may find other employment in another less expensive area. In order to keep their operations running, employers are then forced to raise wages in order to attract or keep a sufficient workforce. This cost is passed on to the consumer, who now pays more for that service than they did last month. As consumer prices rise, so do home prices, making housing less affordable again. And the cycle continues.

Some state governments offer incentives for developers to build affordable housing in high-rent districts. I recently attended a ribbon-cutting for a beautiful new affordable housing complex in the resort district of Virginia Beach. We’re hoping that other developers follow this example.

so i noticed this on their FAQ

For customers who opt to buy Landed out without selling their home, this can be done by refinancing with their lender or by paying Landed’s down payment program directly with funds from savings, investments, or gifts. You have control over when and how to end the partnership.

which means you could pay off landed early, if you get favorable appreciation, just by doing a regular refi.

so you can cap their upside. without a limit to their downside.

That’s a good observation, and kind of what the examples suggest. Once your $500k house goes up by $67,000, technically your 75% share of the appreciation will exactly cover the $50k

loan (“coinvestment”). Add in some wiggle room for fees and appraisals, and you might wait for $100k in appreciation.

Of course, a home buyer doesn’t ???? to put down 20%. 20% is for a better terms with the bank. Paying PMI for several years may be better than giving away 25% of the upside. If a homes value increases over several years, why not ask the bank to reevaluate the PMI situation based on a new appraisal? Seems far less expensive to me. These programs seem to be targeted toward first time home buyers with little experience.

You don’t need to put down 20%, but if you got 10% of the house value covered upfront, the better interest rate from a traditional mortgage, and no PMI, your total monthly payment is going to be a lot lower and thus easier to qualify and/or simply afford in real-world terms.

Agreed, the homebuyer should consider all the many financing alternatives out there.

Hey Jonathan,

This is a great suggestion but with some drawbacks as suggested. Firstly, anyone joining on Landed will be tied into a two year contract essentially with their employers.

Won’t the employers use this to limit or even deny people a pay rise because they know the employees will be unable to leave.

Also on a side note, I just want to say I am a huge fan of your website and have been following you for a while. Your insights and information is well presented and easy to follow whilst being insightful.

This is why we have picked you to be on our list of top 10 blogs to follow online to make money and/or gain financial literacy.

https://www.theypzone.com/top-10-blogs-on-how-to-make-money/

Kind Regards,

The YP Zone team