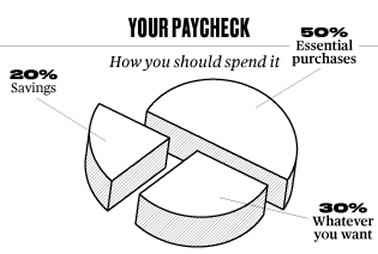

LearnVest is (yet another) online financial advisor, but they are more focused on money management and life planning than nitpicking asset allocation details. Founder Alexis Von Tobel’s book Financially Fearless is on my (long) reading list, and here is one reason why – Per this Businessweek article, their budgeting advice is based on splitting up your take-home pay into three major categories with their 50/20/30 plan:

- 50% towards Essentials, which includes housing, transportation, utilities and groceries.

- 20% towards Savings, which can be retirement accounts, emergency funds, or debt payments.

- 30% towards Lifestyle Choices, which are whatever things you value and make you happy. Eating out, shopping, childcare, cell phone plans, entertainment, and so on.

This is an interesting way to make people streamline their budgets. I don’t recall any other personal finance book breaking things down like this. 20% is a pretty good starting point for savings, and I like that there is explicit room for the fun stuff. (Though the fact that “childcare” is under Lifestyle Choices may be somewhat controversial. If you pay for daycare, it is not uncommon for that to be a huge chunk of your expenses.)

LearnVest has several free features and mobile app, including a Mint.com-like app that tracks your spending and matches it up with their 50/20/30 pie chart. However, they will try to upsell you a more personalized advice packages with Certified Financial Planners. Their target demographic is young professional women, but I didn’t really notice when using it briefly so far. Anyone else use them for longer?

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

This is the exact breakdown Elizabeth Warren suggests in _All Your Worth_. The idea is that if you lost your job and had to go on unemployment or disability, you’d be getting about 60% of your original income, enough to cover the essentials. Or if you are a two-earner household and one person’s income was lost, the other income would suffice.

I really like it as a guideline, but find it kind of hard to apply in practice. You can’t just calculate half of your paycheck for essentials, because you have to add back in the cost of medical insurance premiums and other “essentials” that are taken as payroll deductions. And it’s hard to budget things like groceries because most grocery bills include “wants” and not just the bare minimum needed to survive. Still, it’s a useful metric, and I like that there’s a basis for the numbers; it’s not just totally arbitrary.

Thanks for your comment. I should add that book to my reading list as well.

That’s a great breakdown for someone who wants to retire at 65. Not so much for FIRE.

Agreed, but most people just want to retire comfortably at 65. I’ve met so few people “offline” that are serious about early retirement (or even consider it an option without a lottery win or huge inheritance).

i thought that 50 30 20 is pretty common?

http://lmgtfy.com/?q=50+30+20+rule

Hmm, it does look like the first mentions of this are from Elizabeth Warren from her book All Your Worth published way back in 2005. I’d never heard of it myself before now.

I’ve used them for a while and even bought the CFP package when they had a super sale. I would say it’s definitely geared towards younger professional women with no children. I had many chats with them about childcare being categorized as a lifestyle choice instead of essential (because my childcare bill is larger than my mortgage and I know I’m not along in that). That really sticks in my craw, and they were unable to help me adjust their tool to really work for me. I completely derailed them when I asked for input on how to financially prepare for a divorce. I spoke with two CFPs and they were both younger women without kids who just did not seem to get me or really give me a personalized plan based on my situation.

Thanks for sharing!

I agree, childcare (esp daycare) can be huge and pretty much non-negotiable. I was thinking that maybe people could just consider childcare a “tax” and then budget their after-tax and after-childcare income around the pie chart. Still tough.

See the whole thing of essential vs lifestyle is kind of arbitrary : living in a certain house and driving certain cars is a matter of lifestyle too not “essential”

We do have commitments that we can’t easily abandon due to financial transaction costs : like changing a car, or house.

And other that we can’t ethically abandon like having children and pets. I have 5 pets in my house. Way too many and they affect my budget, yet I can’t just get rid of some of them to balance my budget like I can downgrade my phone or cable bill or even a car. I can try finding best value for their food and Healthcare. And so people with kids.

Hence I like to have four categories: fixed essentials (e.g mortgage, rent) ; variable essential (e.g food, childcare;electric ) ;fixed non-essential (cable, phone ) and variable non-essential (dining out)

Hi samatha,

Do you remember what you paid for the CFP package when they had a super sale? Their 5 year planner is now $50/month which seems to be alot higher then before. If you know a way for me to get a better deal, please let me know. Thanks!

Hi Sarah,

I paid around $200 for the plan and a year with a CFP. That was back in 2013. They offered me a re-up with a new plan and $19/month access to the CFP but I declined.

Good luck!

Samantha