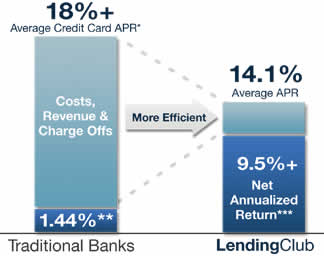

LendingClub.com (LC) is a website that securitizes person-to-person loans so that you can lend money to other people in as little as $25 increments, and you earn the interest. The idea is to replace banks and credit cards as the major middlemen used for lending. Here’s an illustration from their site:

LendingClub.com (LC) is a website that securitizes person-to-person loans so that you can lend money to other people in as little as $25 increments, and you earn the interest. The idea is to replace banks and credit cards as the major middlemen used for lending. Here’s an illustration from their site:

Now, if you read my previous posts on LendingClub, you know I’m skeptical about getting 9.5% returns in the long run. My LendingClub Net Annualized Return is currently 6.8% after fees. If I can stay in the 4-6% range, I’d be happy as I view this activity as a hobby. My favorite loan so far is helping a young couple purchase a tiny 200 sf house-on-wheels.

The investment process is set up such that LC examines the loan application and assigns it a credit grade with an interest rate from 6.39% – 21.64%. All you have to decide is whether to fund the loan or not in increments of $25. You can’t change the rate. Therefore, the key is to quickly fund the relatively attractive loans and avoid the unattractive ones.

You can view historical performance data at the LC website, but it is very raw. I recently came across a new site called LendStats.com that has been sorting through the data and presenting it in some very insightful ways. The owner KenL uses a nice, simple formula for return on investment (ROI) and one can see from the data several ways to improve your returns.

Loan Factors To Avoid

Business loans. If you look at all the loan categories, only the ones under the Educational and Small Business categories have negative ROIs. (Educational loans have a much smaller sample size.) In general, perhaps it is a form of adverse selection when someone with a business idea must resort to making a personally-backed loan from strangers to fund their idea. Also, it may be that the economy is so tough that only select new businesses survive.

Borrowers with mortgages. Until recently, a mortgage holder was deemed more credit-worthy than a renter. That person had to have the means to make a 20% down payment and pass underwriting from a bank. Now, with so many people underwater in their homes, the ROI from renters is higher than mortgage-holders. Renters have greater flexibility with their cashflow. I suspect many people find themselves so bogged down by their mortgages that they decide to simply declare bankruptcy and forget about all their other debts as well.

Loan amounts greater than $20,000. Loans over $25k have a negative ROI overall, with $20k loans not doing much better. Bigger loans means bigger risk, which apparently isn’t adequately compensated for by higher interest rates. Also, I am wary of people doing the “borrow-and-bankrupt” route where they try to amass as much debt as they can and then declare bankruptcy after either a huge party, leaving the country, or hiding assets.

Borrowers with more than 2 credit inquiries within last 6 months. Average ROI consistently goes down as the number of inquiries on your credit report goes up. This indicates that you are also trying to get credit from others, and thus your debt-to-income may be higher than reported. In general, this also increases the likelihood of either desperation, fraud, and/or impending crisis.

Any F and G rated loans. The general trend is still supporting my original plan of only buying the highest-rated A loans, however there are some improvements in the B through E grades. Loans with the lowest grades of F and G continue to have negative ROIs. These are also the loans with the smallest sample size, but since there are so few of them anyway I find it easier to simply avoid them.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Educational loan has a negative ROI. This is interesting. I think it used to be a good category. Does it mean college students are facing much much tougher market?

Well, perhaps those people that can’t get student loans through conventional, government-regulated means and must go through alternative avenues.

Glad to see this article.

I got my feet wet with Lending Club at the beginning of this year. I started with 2500, and I’m now at almost 10k.

My annual return so far is hovering a little over 14%.

I have purchased 45 notes. 2 were paid off in full early. The other 43 notes are current.

I’m pretty picky when I go through these notes, I set my own standards. I mostly fund professionals (doctors, lawyers) or soon-to-be professionals (finishing last year of school, residency, etc.)..

They are far and few to come by, but they are there. Income must be verified, and credit score must be approved my Lending Club. Usaully stay away from $25k loans (the max you can ask for). I prefer current employment to be beyond 2 years. Also I cancel in my search anyone who has any public records, as to me, this is just ‘expierience’ in doing things that I wouldn’t want them doing with my money.

I have about 50% of my money in E grade loans. 35% in C, 10% in D, and the remainder in A grade loans. I think I put $25 in an F or G just to see what would happen 🙂

Again, I am very picky in the loans I pick, and I sometimes will ask the borrower questions that reveal their ‘personality’ more than any ‘financial measurement’… I don’t know why, it just helps me out.

Also, the “Loan Description” (field in which they get to make their case on why they need the loan) has to be pretty well thought out, and pretty well written. If it is blank or says “using this for dept consildation” (or something equally ignorant), then I dont even bother.

I enjoy the professionals who put together their Loan description with thorough details, and also state why they have come to Lending Club (because they have done their homework, and can get a better rate, etc.)..

With that being said, I am waiting to reinvest a good sum of my funds I have collected, but I have not found any notes (There are usaully always A and B notes, but I’m looking for those good D and E grade borrowers) in the last 2 weeks. I will not jump the gun though. I will wait. Got to be patient 🙂

And to match Jonathan’s favorite note.. Mine has to be this soon to be anesthesiologist. He graduates this spring. He used lending club previously to finance an engagement ring, and honored the loan. Liked LC so much, he came back and is using it to finance his wedding this May. His occupation is in high demand, and this guy will definitely have a job. He put together an incredible loan description; very thorough. His credit is good, his residency income has been verified. He will be making the big bucks soon, I know he can honor this loan. He was an “E1” grade loan candidate , and was listed at 16.45%. I was so confident in him, I dropped $2500 alone in his note alone.

That was 6 months ago, been making $30+/month on interest on that note alone, plus my princple repayments. Not bad 🙂

I guess to sum things up. LendingClub is good if you be smart, and have patience.

Joe

Thanks for the tips Jonathan and Joe C. I have already used some of these tips, but you’ve given me a few new ones.

I also like to see which lenders ask questions on a loan. There are a few names I recognize, “Critical Miss” and “USMC Retired” that seem to be after the same loans I am. I sort of ride on their coattails sometimes.

I also loaned to the “house on wheels” people, per the post on this site. I also look for higher ranking military people or government employees. I wish LC was easier to search for keywords, I find the keyword search function nearly useless.

p.s. there used to be a good LC forum, is there one out there anymore? I’d like to discuss with other like minded investors open loans, and kind of help each other root out the good ones.

So what loans should you get involved with then?

Jonathan, sounds like the just about same listing criteria I came up with after lending on Prosper for two years. Good to see lending criteria are similar across platforms.

Frankie, the prospers.org forums have a small section dedicated to LC with several people who contribute regularly and discuss strategies, etc. Be forewarned the other areas of the forums are filled with posts by people dissatisfied with Prosper.com, many of whom feel P2P in general cannot work well for lenders and on occasion may post such grievances in the LC area as well.

At least your return is still positive. I had one of my supposedly A rated loans go bad after only 5 months. After the write off my rate of return is negative 13%. The amount of the loan was the same as my signup bonus so I didn’t lose any of my own cash, but it does make me pretty skeptical about the screening process lendingclub uses and the loan rates they are charging to compensate for the risk being taken.

It’s also made me question whether I want to put any more money into my account or if I should just stick with investing in the stock market

@Russ – Sounds like you don’t have very many loans, so any single bad loan can destroy your rate of return. If you had 100 loans, then one loan going bad early on is still only roughly 1% of principal. If you have 5, then a single loan is 20%.

I forgot to mention that existing lenders should log into their account to see if they have a recurring investment bonus. If you transfer in 200 per month, they’ll give you a 1% bonus on the amount transferred.

I’ve been with lending club since march of 2008, I have about 400 loans(300 of which are 1 month or older),the other’s were recently issued. My Current return is about 12.3%, it dropped recently as I had a default on a loan(A grade) that I never should of invested in. I picked up the loan from experimenting with the lendingmatch feature on LC and the person has $1500 month unverified income, no loan description,etc which is against my criteria for selecting notes on many fronts. I have 2 others that are late, hopefully they won’t default.

I do think there needs to be a LendingClub community for lenders only, I aware of the prosper.org forums, but it is note as lively as it needs to be.

Diversification is key.

I would say that if you are getting a 4-6% return that is better than some other interesting bearing accounts, but given the uncertainty and effort, is it really worth it?

I think calling it a hobby is a good idea, because with all the time and “variability” involved, it seems like a marginal way to invest.

“I forgot to mention that existing lenders should log into their account to see if they have a recurring investment bonus. If you transfer in 200 per month, they’ll give you a 1% bonus on the amount transferred.”

I just got 1.5% for a 500 per month transfer.

Jonathan – yes, I only have about 10 loans, so losing one early destroyed my IRR and agree that a more diversified loan portfolio would mitigate that risk. I was originally planning on setting up a recurring deposit and building a portfolio of a few hundred loans. Now I’m not so sure.

What I’m really having is a crisis of confidence over the entire LC loan rating system. It may be unfair but I no longer trust the letter grade, and subsequent interest rate charged, that they apply to a given loan. Given the time and effort it takes to sort through all the bad loans to find the ones you like and even then most of the info is unverified, I’m really questioning if investors are being adequately compensated for the asymmetrical risk they are being asked to assume.

Nice post. Thanks for mentioning my site. I’m glad to see so many of you recognizing the value of my analyses. I think with the lessons learned from my site a person can easily achieve 7% and with additional diligence and some common sense 10% can be achieved. Of course, if someone is as patient and diligent as Joe C then even higher returns are possible. Good job Joe C!

I’ve been lending for almost 2 years I’ve made about 1000 loans (sold about 300 on folio). I have been using my site to help choose loans for the last 8 months and I’ve seen my own returns climb steadily. I estimate my current returns to be about 8 or 9%. I’m really happy with that and aiming even higher still.

ive been on LC since march…i thought by manually reading and screening the loans i could beat the default rate… BUT…right now..im exactly at the average rate…

i have 50% B and 50% C loans….with now 4 either in grace period or late…one is fully paid…this matches exactly pretty much, with expected default rate ( i consider lates..as defaults for my purposes 🙂

im in Pennsylvania…so i have to buy on the secondary market..thats a good trick for lenders who want to invest..but, their state isnt registered…most (not all) states are allowed on the secondary note market.

I’ve purchased a dozen or so loans at a discount from the secondary market, most of which are loans that are 20-18 months old and meet my criteria(current,no huge drops in credit score, profile characteristics, and payment history).

Though, I remain highly skeptical of it because of possibility of insider trading. Someone who knows the person dumping the loans because they know they’re going to default. Not cool.

excellent idea, and one that has been tried by several other websites before. each one of us has a different risk appetite, and our personal underwriting standards will dictate the activity in this “secondary” market. the challenge here will be getting the comfort level necessary to lend.

Total deposits: $5,640.39

Total withdrawals: – $5,589.96

Cash used to purchase notes: – $2,013.78

Payments received: + $2,002.52

Performance Summary

Payments received: $2,002.52

Principal paid off: – $1,791.34

Payments in excess of principal: = $211.18

Principal charge-offs: – $222.44

Gain/loss to date: = -$11.26

Final results of 3 year Prosper experiment