I can’t recall the exact source or quote, but I read something along the lines of this in a forum recently:

I can’t recall the exact source or quote, but I read something along the lines of this in a forum recently:

We don’t really want to hear other people’s opinions. We want to hear our own opinions out of other people’s mouths.

In other words, confirmation bias:

(source: Chainsawsuit.com)

The majority of my portfolio is in low-cost, diversified, passive-managed mutual funds. In order to hear a different take, I read the shareholder letters of Longleaf Partners Funds (Southeastern Asset Management), which are respectable examples of higher-cost, concentrated, actively-managed mutual funds. The managers “eat their own cooking”, meaning they put a substantial portion of their personal net worth into the funds. They have a limited number of holdings, try to avoid asset bloat, and try to outline their positions in shareholder letters.

In their most recent 2nd Quarter 2018 letter [pdf], they share a presentation that explains their position:

Why We Believe Active Long-Term Value Investing in Common Stocks Will Actually Work

Active investing is out of favor; long-term investing (or really, long-term anything) is out of favor; value investing as we practice it is out of favor; and, investing in common stocks is out of favor compared to private equity. Doing all four of these things really makes us the skunk at the party.

Many have given up on active, long-term, engaged value investing in public equities just at the point when we believe it offers the best risk/reward proposition. Indexing’s multi-year momentum has pushed more assets into fewer stocks because they have gone up and left behind an expanding universe of highly competitive, well-governed and managed businesses with unique advantages that are materially underpriced in their publicly traded securities.

They make several interesting points, including the high amount of “closet indexers” out there. (Haven’t there always been a lot of closet indexers though?) I tried to see things from their perspective, but in the end I think their 1% expense ratio is just too high to overcome. It will definitely take a bear market for their performance gap to narrow.

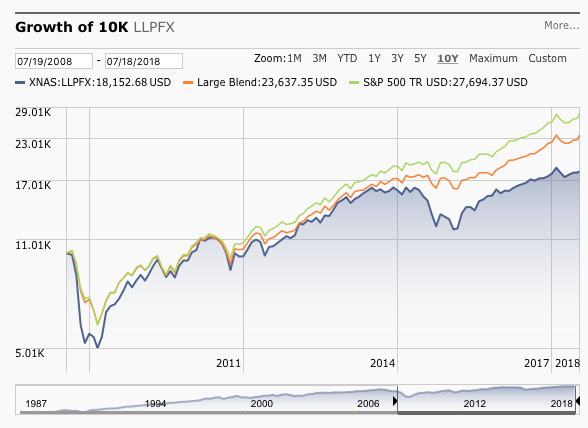

In the meantime, their real problem is that poor relative performance. For every $10,000 invested in their flagship Partners fund 10 years ago, you would have about $18,000 today. If you had put it in a low-cost S&P 500 index fund, you would have about $27,000 today. That’s the difference between 6% and 10% annualized returns over the last 10 years. The extra drag from their ~1% expense ratio accounts for about a quarter of the performance gap.

Longleaf Partners Fund very well might turn things back around. I have no position in any of their funds, but I’ll keep reading their free shareholder letters and watch them try their best to play a very difficult game.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

This was a good read. Thanks for sharing.

Kind of like my twinkie-and-doughnut diet. Sure, it’s had a rough patch of luck in the past few years, but I have a hunch it will outperform the kale-and-broccoli diet this coming year….because of science and stuff.

Many claim, few reach greatness:

In 2007, Warren Buffett bet a million dollars that an index fund would outperform a collection of hedge funds over the course of 10 years.

http://fortune.com/2017/12/30/warren-buffett-million-dollar-bet/

Given that many of these value funds (longleaf,weitz,fpa,oakmark,jensen) provide free learning resources by posting their quarterly reports,is there a long term case study on investors who follow in their footsteps by mimicking the funds by buying the top holdings.If one were to be patient and the fact that many of these funds have low portfolio turnover and a concentrated portfolio it would seem like one could get a free lunch and learn at the same time.Your costs would be only commissions.I wonder if there is a real life study on this.I index majority of portfolio but do follow the above funds and have been mimicking their holdings selectively for the past 7 years or so f about 10% of my portfolio.My results overall have been similar to the indexed portfolio.some.individual holdings have done very well while others have been duds.

Munger talks about copycat/piggyback investing in this interview:

Thanks Jonathan.I hadnt seen this interview of Munger before.Mohnish Pabrai who was mentioned by Munger in the interview is a big proponent of cloning/copycat investing.