Whether you invest your hard-earned money in passive index funds or actively-managed funds, the more important thing is that costs matter. Every penny you pay in mutual fund expense ratios, sales loads, trade commissions, and financial advisor fees reduces your return. Even Morningstar, a company famous for their proprietary  star rating system, looked at their data and admitted that expense ratios are the “most dependable predictor of performance” and should be the “primary test in fund selection”. I like to visualize high expenses as a constant, relentless drag that is almost impossible to overcome over long periods of time. You can play with this cost widget to see how much costs eat into returns over time.

star rating system, looked at their data and admitted that expense ratios are the “most dependable predictor of performance” and should be the “primary test in fund selection”. I like to visualize high expenses as a constant, relentless drag that is almost impossible to overcome over long periods of time. You can play with this cost widget to see how much costs eat into returns over time.

Here comes more proof. I invest a huge chunk of my money in Vanguard funds, because they offer the best selection of low-cost mutual funds around. Every year, as they get more successful, my costs actually go down as they advantage of economies of scale. However, they also offer a large selection of actively-managed funds, one of which has been around since 1928.

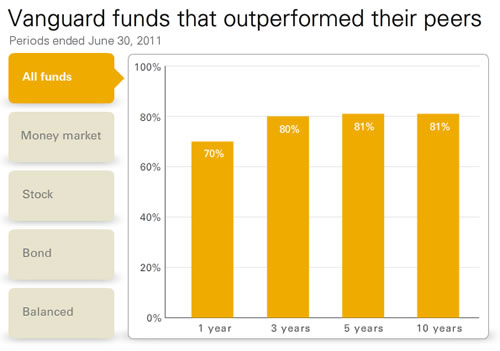

Data from Lipper Ratings shows that over 80% of Vanguard funds (both active and passive) have outperformed peer funds in the same categories over the last 5- and 10-year period ending 6/30/11.

You’ll find that T. Rowe Price also touts the returns of their group of funds:

Not by accident, one of their tenets of investing is low costs:

Low-Cost, Active Management

We believe in actively managing our funds and pursue a disciplined process to individually evaluate every stock and bond we invest in. But we don’t believe it should cost a lot. We keep our expenses low, so your investment can go even further. We offer over 90 funds with no loads, no sales charges, and expense ratios below their Lipper category averages.

Survivorship Bias

Making the case even stronger, by hovering over the the Vanguard chart, you can see how many peer funds there were. Let’s just take the stock funds. For the 1-year comparison, there were 10,644 funds in their peer category. For the last-3 years, that drops to 9,207 peer funds. Last 5 years, 7,562 peer funds. Over the last 10-years, only 4,035 peer funds existed.

Where did all the funds go? Sure, some funds are new, but there were lots of new funds back in 2000 as well. The fact is that many older funds are unable to be compared today because they never lasted 10 years. Most likely, their performance was so low that they quietly closed down or merged with another fund. This is called survivorship bias, and means that existing funds did even better than these charts might indicate because of the dead funds that aren’t even included.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Doesn’t the Vanguard chart simply reflect the steadily increasing number of stock mutual funds? That is to say, ten years ago there were around 4000 in their category, and as of one year ago there are over 10,000(!). The survivorship bias is certainly valid, but the Vanguard stock chart doesn’t seem to exemplify this — instead reflecting an increasing, not decreasing, number of funds over time.

@Michael – That’s a good point, I think there are more funds now. My idea is that in any given year there are a lot of mutual funds, but most are young. But finding “10-year old” funds is harder. I can’t seem to tease the number of funds existing back in 2001 out of the Lipper website. Will try again over the weekend.

Ah, an excellent point about the relative youth of most funds. I can’t recall exactly when it was that I first heard that there are now (then) more equity funds than there are actual equities in the US market. Yikes!

And I don’t think I’ve mentioned it before, but thank you for your wonderful blog. The information herein is almost uniquely sensible, insightful, and eminently useful. You are directly responsible for saving all of us substantial amounts of money. Thanks for all of your hard work!

I’ve never had much interest or luck in picking bond or emerging market funds. I’ve typically bought individual Corporate, GSE or in a few cases foreign Corporate bonds denominated in other currencies.

I’d be curious to know what your top Vanguard picks were.