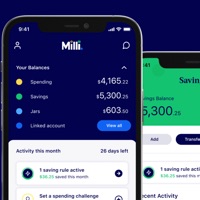

Milli is a new app-only savings account that is backed by the FDIC insurance of First National Bank of Omaha (FNBO). iOS and Android apps available. They came out of the gates at 5.00% APY but recently raised to 5.25% APY. Here are the highlights:

Milli is a new app-only savings account that is backed by the FDIC insurance of First National Bank of Omaha (FNBO). iOS and Android apps available. They came out of the gates at 5.00% APY but recently raised to 5.25% APY. Here are the highlights:

- 5.25% APY as of 7/20/23

- No monthly fees, no minimum balance required.

- Ability to split money into multiple “Jars”.

- App-only. Currently requires iPhone iOS 15.0+, or Android OS 8.0+.

- Uses the Allpoint ATM network of 55,000 surcharge-free ATMs worldwide.

- No paper checks. No checkwriting ability. No mobile check deposit.

For you rate chasers. this puts Milli newly at the top for a liquid savings account after my July 2023 interest rate update. We’ll see how long it lasts.

If anyone remembers FNBO Direct, that is still around at 3.75% APY. So there is a history of FNBO going trendy and grabbing some deposits with a competitive APY for a while. The term “online savings account” is now redundant. The new thing is app-only.

Reading through the various app reviews, the most common complaint seems to be getting denied for a new account after going through the whole application process and/or difficulty funding the new account. So be prepared for some account-opening hurdles.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Easy Set up & opening of an account via their App.

Looking forward to some 5.25% APY for a while…

Finally time to end my relationship w/HM Bradley, which I have been talking about for too long.

Still trying to figure out what the max protection there is for FDIC insurance (P1 + P2) and the max amount that can earn 5.25% APY.

Hi: thanks for sharing this info on this savings app. Forgive my ignorance, but if I sign up for this and deposit 1,000 at 5.25%, at the of the month I will make $52.50 or at the end of the year?

Please clarify.

APY is annual percentage yield. If you deposit $1,000 and the rate stays at 5.25% APY and you keep it there for a year, you will end up with $52.50 in interest after compounding.

Thank you very much. Appreciate your response.

For smart investors, this really comes down to whether its “app-only” API can be accessed by aggregators like Mint.com. (Current answer: heck no.) I suspect that their business model is cynical: they will reap marginal profits from the fact that app-only banking is less attentive, more under-the-radar, the least optimized for moving money around, unintegrated with aggregators like Mint (they can refuse anything of course). Unless it’s an open system, it’s a non-starter.

Experienced an issue with milli ACH transfers.

They have a “SPENDING” account and a “SAVINGS” account.

I linked an external account to the “SAVINGS” account as savings and although

verification and transfer completed it generated “INCORRECT PAYMENT CODE.”

Chatting with them, both of their accounts code as checking, so as strange

as it sounds you have to link their “SAVING” account as “checking”

None of my active accounts would link in Plaid, so I transferred from Fidelity to the account number I saw in the app. Unfortunately, that was the “Spending” account. I didn’t recognize the problem until I got my first statement a month later and discovered there were two accounts and I had received zero interest. I have already filed a complaint with CFPB.

I got an invite to sign up for this new Milli app because I once had my savings with fnbo direct. I moved it to SOFI because they are now at 4.40%. I was considering switching back for 5.25, but I have been unable to create an account. I just get a spinning wheel. This new app has been rolled out very poorly, and SOFI as an app works wonderfully and nearly flawlessly. Unless they can prove they have an app that works well, I cannot recommend.

I tried to setup a transfer from my bank to Milli and got an error “An invalid routing number was entered. Please enter a valid routing number.” Milli’s routing number is 107002600. I googled it and it is correct belonging to First National Bank of Omaha. Anyone else having this problem?

Hi Nick, I finally got my account opened, and set up links to my external accounts using Plaid inside the Milli App, and successfully transfered some money into my new Milli savings account via that method. Be forewarned it took a full 4 business days for the balance to appear as available at Milli. My next effort is to try to get Direct Deposit via my company payroll set up, but my employer does not yet recognize the routing number you referenced above in our payroll systems, so opened a trouble ticket with my own payroll department to see if they can get it added. Hopefully so, as 5.25% might be worth the extra effort to establish automatic Direct Deposit savings with Milli Bank if my payroll department will allow it. Take into account Robert Johnson’s experience as well when setting his up. Has to be coded as checking even though you surely want it going to your Milli Savings account instead. Good luck. The app is very basic, buggy, and hopefully will improve over time.

I opened a Milli account for an emergency fund and received a large sum of a donation and I didn’t get any of it. I didn’t even have the card yet. Someone who doesn’t even live in the same country as me cause I checked myself to see where the purchases and transactions were being made. They used every penny. How does this happen. All I have received from Milli is an email saying someone should be contacting me and nobody has. I reported it and they did nothing.

Any updates??

I opened a milli account n as soon as I deposited money in they restricted my account n now they sent email that they were closing my account n they haven’t responded to my email or chats n haven’t sent me my money back

Any updates?? There has to be more to this story.

You posted this before a long weekend. Hopefully they have responded to you by now.

YEs, please update. Im interested in milli but see many bad reviews.

I did file a complaint with the Consumer Financial Protection Bureau. They responded the next day and forwarded my complaint to Milli. I also reached back out to FNBO from a site I happened upon and asked for someone to call me back. Someone did and I explained the situation. He put me on hold several times and I could tell he was reaching out to someone else, when I asked who, he wouldn’t tell me. While we were on the phone, I got a “ding” on my phone and I said “Well, how about that, my account just got unlocked”!!! He said “Yeah, they said they were going to.”

I have since had access to my account. I have not deposited any more money and have not tried to withdraw any. I have had my interest payment post monthly to my account.

I still would not begin to open an account after what I went through. The process, for whatever reason, was horrible. If they have worked their kinks out, then I would but like I said, I haven’t done a withdrawal or deposit since this happened.

A family member recommended me to milli. He never had any issues with them and seemed to be fairly happy with them. However, as soon as I transferred my funds from my bank to milli’s savings account, milli “restricted” my account.

I received an email saying that my account had been restricted and that I needed to email them or message them on their app. I was not told why my account had been restricted but that it just simply was. What followed, was what i would describe as the worse 3 weeks of my life. I would email milli, receiving messages like “the support team will reach out to you in 1-2 business days.” That day never came.

For the first six days my money was not in my home bank and was not showing up in milli either. Imagine looking at your life saving account and seeing nothing there and no phone number, no customers service representative to help you. I would email milli every day, sometime several tmes a day to geth through for someone to help me. How I am supposed to pay my bills, groceries, living expenses? I finally called the First National Bank of Omaha which the the bank the milli operates under and they told me that they could see my account, but could not connect me to a customer service rep from them. They had no number for this sub-division that could help me. Think about that for 2 seconds. There was literally no phone number to call and beg for help. This went on for weeks.

I have never been so emotionally, mentally, and physically stressed and angry at the same time. Some people have a decent experience with milli. Good for them. I just wish I would have read a review like this one before transferring a large chunk of my life savings into their savings account. There are other online banks with high yield savings that actually have a customer service number. I would not wish the experience I had with milli to my worst enemy. God bless.

I am in a similar situation. I went to my local bank to help me with an ACH transfer. I was able to send 10k to a Milli Savings and $20 for checking, as I did not need to use the money unless in an emergency. The money went in Sept 2, and like others, I was and still am denied access to my money. The app won’t even let me see my statement. Supposedly, in the middle of last month, I was paid interest, but am I really? I used the chat feature,, and all they can do it tell me that I am under review, and someone will contact me, which never happens. They DID send me a debit card but of course I am also restricted from using it or even activating it. When I called the number on the back of the debit card, it tells me to use the app chat or send an email. I have sent numerous emails and get a response that the Investigative Team is reviewing my account and will contact me if they need additional information. Tomorrow is 40 days in since I opened my account and have no access to my money.

I called First National Bank of Omaha last Friday and today. I called the fraud department because everything about this app reeks of fraud. They are aware of who Milli is, and said they are the Parent Company and have no ability to see my account information. So, beware.

I plan to file a complaint tomorrow with the Federal Trade Comission. I may also file with the Comsumer Financial Protection Bureau.

The Milli HYSA party is soon over.

As many Milli depositors by now know, the interest rate will be dropping from 5.5% APY to 4.75% APY on Feb 29th. Ugh!!

What’s more troubling though is the amount of people who were caught up in the “Restricted Account” situations. I’ve read of people being flagged for different things – from the setup of their accounts and transferring money in to trying to do a simple change of address and the accounts being locked down. From their Facebook, Instagram, Twitter, etc social media sites, to Doctor of Credit, DepositAccounts.com, etc, there have been numerous complaints about their lockdown policies and how it is impossible to speak with a live person and that their chat and e-mail support is basically useless. It’s not until folks start complaining to either FNBO (the parent bank), the CFPB, or their Federal Banking Regulator (The Office of the Comptroller of the Currency (OCC)) do they finally get resolution.

I soon will be pulling my $$ to keep the higher interest rate party going for as long as possible. I just hope my account does not get locked/restricted in the process.