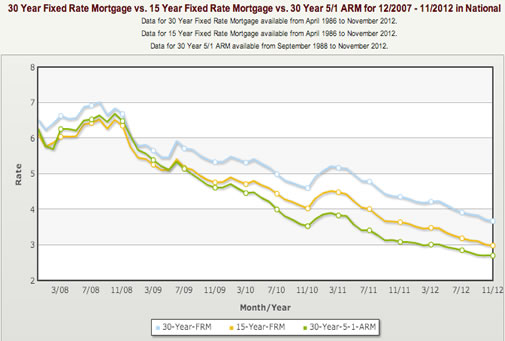

In case you haven’t been paying attention, mortgage rates are still dropping to new lows. Here’s a chart of the historical mortgage rate averages since I bought my house in late 2007, courtesy of HSH.com. It includes the 30-year fixed, 15-year fixed, and the 5/1 30-year adjustable.

From looking up some quotes (see below), 30-year fixed rates are ~3.125% now (~3.5% with no closing costs), and 15-year fixed rates are ~2.5% (~2.875% with no closing costs). Can you honestly say that you would have expected this 10 years ago? Another example of the difficulty of predicting the future.

If you haven’t refinanced in a while, it is definitely worth a try to see how much you could save a month. But what are you going to do with that savings? Buy more stuff that you don’t need? Buy more house that you don’t need? Why not consider refinancing into a 15-year mortgage and have that house paid off much sooner? From this CNN Money article using recent average rates:

Homeowners current paying off 30-year loans with rates of 4% spend about $1,098 a month in mortgage payments on a $200,000 balance, paying a total interest cost of $143,739. Refinancing at 2.63% for 15 years would cost them about $250 a month more, but they would wind up paying just $42,250 in total interest and their payments would end years earlier. Refinancing into another 30-year loan at 3.31% would cost homeowners only $877 a month, saving $221 from the existing loan.

If were to give advice to my future kids, it would be to determine home affordability only using the 15-year mortgage. Just forget the 30-year exists. You’ll be forced to budget properly and if you buy a house at age 30 you’ll be mortgage-free by 45! I think they would thank me in the end. I can still tell them their old man paid his off at 35, of course. 😉

Compare with rate quotes from:

- Provident Funding

- Quicken Loans

- Cashcall Mortgage

I hear that Costco provides a mortgage refinance referral service now as well – any real-world experience with them from readers?

Recent mortgage refinance articles:

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

With direct (income + payroll) marginal tax rates for most of us in professional occupations approaching 35% (with an “up” perspective), we are probably talking about 2.1% effective for 30 year, and 1.5% for a 15 year fix. Historical US inflation is something like 3.2%. A lot of money has been printed of late, but let’s stick with 3.2%.

I haven’t done the math but it may be higher NPV, depending on your discount rate of course, to be in a 30 year since you now get paid (in house equity) to have a mortgage.

This is crazy. We just bought our current house 18 months ago (4.75% 30-year) and I just re-fied six months ago at 3.875% (also 30-year) with no closing costs. I’d consider another refinance but the application process was so exhausting and drawn out.

The HSH numbers feel too high to me, both comparing the Nov 2012 numbers to the other links you provided and also comparing with the rates I got on my original mortgage and the two times I refi-ed over your time span.

I guess a significant number of people must be getting 30-yr mortgages above 4% right now to average to 3.67% on HSH when Provident Funding is advertising 3.125%.

Always worth noting that you can “roll your own” conversion on an existing 30 year to a 15 year by just simply paying the extra principal every month – and you can “rollback” in case things get tough. You won’t have the chore of refinancing & closing costs but you won’t get the benefit of the rate reduction either.

I completely agree with Joshua. With the tax-effected rate differential so small, the right move is to do the 30-year. Many of the muni funds yield much more than 2%, so you can take the payment differential, invest it there, and come out ahead. If your priorities change, you always have the option of paying more toward principal.

So frustrating how it seems like everyone and their mom is successfully refinancing to some incredibly low rate and here I am paying my mortgage on time for the last 7 years, checking with different brokers every few months, and still unable to do anything because I can’t get the place appraised high enough. It’d be optimistic to say the appraisal amount would come in around the current loan balance.

If you have lots of money to spare, then paying $250 more per month to get a lower rate may be a good idea.

But for the other 99% (to use a cliche term), there are tradeoffs to consider and the money may be needed more elsewhere. For example, we do pretty well but I would never consider paying more to get into a 15-year mortgage instead of a 30-year because I plan to need that money in just 17 years for my 1yo son’s college education. Pushing the home expense further out means I can get more into his college fund by the time he turns 18. Even if we did a 15-year mortgage today, it would take me until he was almost 20 to catch up to the same amount of principal invested, and tax-free earnings in a 529 account would be greatly diminished.

As Joshua sort of pointed out, with a 30-year mortgage you get more flexibility to control where the extra money goes. If you want to put it towards the mortgage, great, but if it’s needed elsewhere no big deal.

I have a question on this idea of pre-pay on top of 5/1 ARM versus 15yrs fix-rate, and I try to type-out-loud so you kind folks can help me.

(disclaimer: I am not mortgage professional, doesn’t work in banking, and not a tax profession. You are more than welcome to point out my flaws in this comment)

Say I have a loan amount of 360K from the get-go and comparing all loan options (and I can afford them all, under the 15yrs I would be on tight-budget though):

(via http://www.bankrate.com/calculators/mortgages/loan-calculator.aspx with quick local mortgage rate quote)

30yrs / 3.5% => Monthly $1616.56

15yrs / 2.75% => Monthly $2443.04

5/1 ARM / 2.62% => Monthly $1445

Now, if I pick 5/1 ARM but follow the discipline of 15yrs monthly payment amount without committing to 15yrs fixed-rate loan.

At the end of 5yrs,

(with the help of extra payment calculator

http://mortgage-x.com/calculators/extra_payment_calculator.asp

)

15yrs fix rate:

Payment Interest Priciple

$146582.27 $42636.3 $103945.97

5/1 ARM

Payment Interest Priciple

$146582.27 $40477.45 $106104.79

By doing so, you slightly improve by almost $2000 in principle, of which tax deduction may lose $700 total depends on your tax bracket, and going throw the re-fin again with next 5/1ARM.

Even with the extra money you save from 30yr fix rate and put it back in every month in principal, you gain:

30yrs fix rate w/ 3.5% at the end of 2017

Payment Interest Priciple

$96993.65 $59903.11 $37090.54

5/1 ARM w/ 30yrs fix rate monthly payment

Payment Interest Priciple

$96993.44 $43810.5 $53182.94

You get $16092.94 in principle! And paying less interest at most lost $4827.918 of tax refund to IRS (assuming your tax bracket is entirely above 30% for 5yrs).

Conclusion: I most likely overlooked some costs associate with 5/1 ARM that could be greater both fixed rate options. However, the bone of idea is really to pay more money toward principle and leverage ARM & refinance, by taking risk of the interest rates soar in 2018.

If I can afford to do 15yrs mortgage, great! If I cannot and opt for 30yrs, I wonder if 5/1 ARM with a discipline attitude is a better option 🙂

Is there other ways you can think of to pay off principle other than taking shorter fixed rate loan?

What do you think of using 30yrs fixed rate payment to pay 5/1 ARM and refinance afterward? I did a long post earlier but probably due to long link the post didn’t get published. You can reference my google doc spreadsheet here : http://tinyurl.com/ce3o233

Payment Interest Principal

30yrs at end of 2017 $96993.65 $59903.11 $37090.54

5/1ARM at end of 2017 $96993.44 $43810.5 $53182.94

Assuming you can refinance, you put $16082.4 more in principal while pay less in interest. with 30% tax bracket you may lost $5000 in tax refund.

Did I miss something other than the risk of interest rate soars in 5yrs?

I just refi’d 3 months ago and decided to go with a 30 year even though I plan to pay it off in 12. I just wanted the peace of mind of the lower required payment in case of us lost our job sometime in the next 12 years.

I’m torn because although I hate debt I see the logic of carrying a mortgage as an inflation hedge.

Over the past 18 months, I’ve refinanced twice. The first one from a 30-year to a 20-year, and the second one from the 20-year to a 15-year. While I paid closing costs each time, my rate has gone from 4.875% to 2.75%. While the lower required payment on a 30-year is nice, the amount of interest I could save on a low-rate/shorter-term loan was just too attractive for me to pass up. Now I will have my house paid off before my kids go to college–and we don’t have enough saved up, I can redirect our income towards their education. I, like Jonathan, seek financial independence–and it takes just too darn long to get there with a 30-year loan! While I could have pre-paid my 30- or 20-year loans with similar results (albeit paying more interest), I’m not sure I would have had the will power to consistently make enough extra payments to get it paid off in 15 years.

In the middle of the process myself and my initial loan docs say 3.35%! Super excited