This is a continuation of Part 1: Extension of Retirement or Standalone Portfolio?

If you’ve chosen a standalone portfolio for your 529 plan, every provider will offer you age-based portfolio that automatically adjusts based on the age if your child. In general, it starts out with mostly stocks and over time becomes mostly bonds and cash. This preset plan is called the glide path.

My biggest gripe about the glide path of most age-based default portfolios is their short holding periods for stocks. Nearly every one starts with a ton of stocks, and then quickly shifts to a ton of bonds. You’re basically hoping for big stock returns over a short window of time, which is more gambling than investing. Allow me to explain…

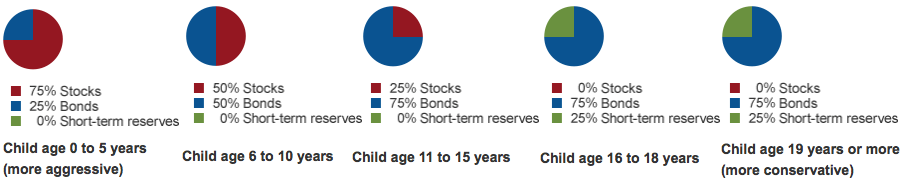

Here is the glide path for Moderate Age-Based Option of the Vanguard 529 plan, Nevada (click to enlarge):

You start at 75% stocks, and then at 6 years old you are down to 50% stocks, and then at age 11 you are down to 25% stocks. So 25% of your portfolio only holds stocks for at most for 6 years. (Imagine if you contributed money at age 5.) Another 25% is only held at most for 11 years.

If you contributed equal amounts of money every year to this Nevada 529 moderate age-based plan, your average hold time for half your portfolio (2/3rds of the stock portion) is around 4-5 years in stocks. If you did a lump-sum in the beginning, the average hold time for half your portfolio would be 8.5 years.

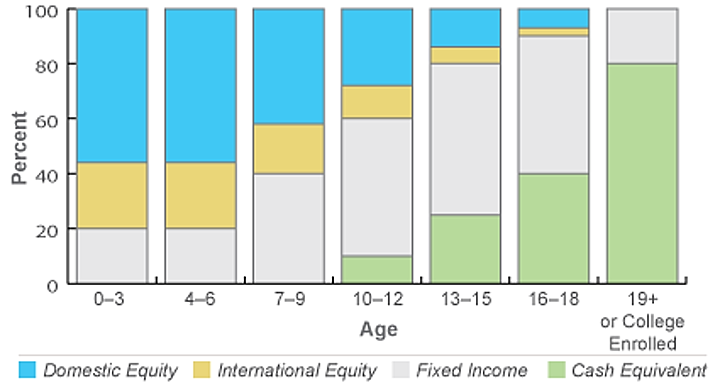

Here is the glide path for Moderate Age-Based Option of the UESP 529 plan (Utah):

You start at 80% stocks, and then at 7 years old you are down to 60% stocks, and then after another 3 years (age 10) you are down to 40% stocks. At age 13, you are at 20% stocks. That means 20% of your portfolio only holds stocks for at most 7 years. Another 20% only holds stocks at most for 10 years. Another 20% holds stocks at most for 13 years.

If you contributed equal amounts of money every year to this Utah 529 moderate age-based plan, your average hold time for 60% your portfolio (75% of all your stock holdings) is around 5 years in stocks. If you did a 100% lump-sum in the beginning, your average hold time for 40% of your portfolio would be 8.5 years.

Hold time vs. Investment returns

Here is a customized chart from PortfolioCharts.com that shows how past returns varied by holding period for the US stock market. (More info on these charts here).

Note that within 5-year and 10-year periods, there are lots of white and red squares which indicate periods of zero or negative inflation-adjusted returns. The longest drawdown was 10 years. Wouldn’t you like to have ridden that out with a longer holding time?

![]()

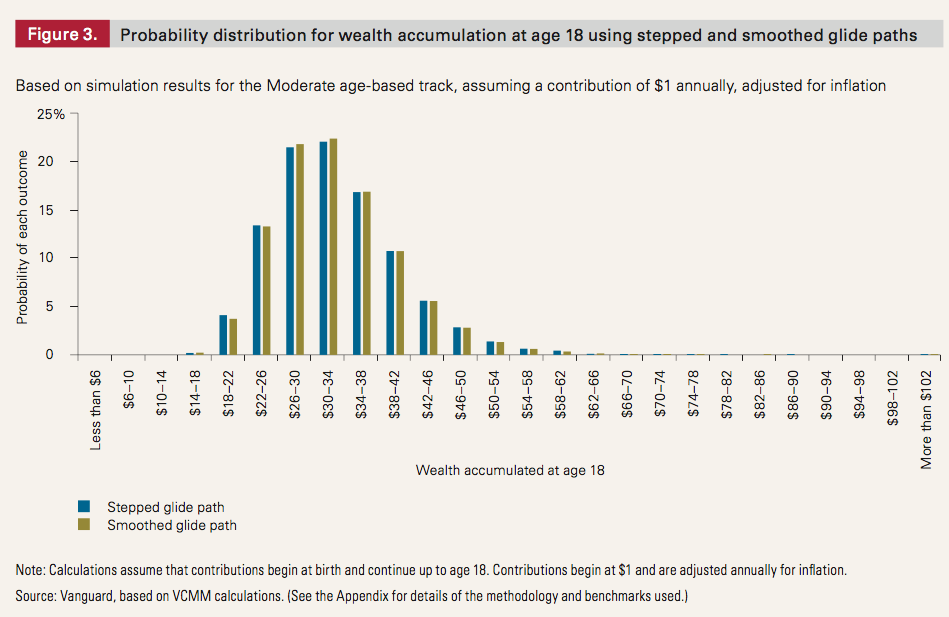

Side note: Some people have criticized the sharp step-downs in the glide path. Vanguard addressed this concern in their 529 whitepaper [pdf]. They ran back-tested simulations and found little difference between a smoothed and stepped glide path (click to enlarge).

They concluded asset allocation was more important, which I agree with, but I wasn’t satisfied with the amount of evidence supporting their short stock holding periods. Sure, on average things look good, but in any given 5-year period things could be quite bad.

My alternative plan is more slow-and-steady, just like my overall retirement portfolio. I will start out with a balanced allocation at roughly 60% stocks and 40% bonds, as opposed to 75%, 80% or 100% stocks. I will then stay that way as long as I can so the stock portion will have a long holding period. Probably 6 years out from college, I will convert 10% from stocks to bonds/cash. So 60/40 > 50/50 > 40/60 > 30/70, and so on until I am at 100% cash at age 18.

I will also front-load my contributions so that they are within the first few years. I know not everyone can do that. This means I will hold all of my stocks for a minimum period of 10 years, with the average holding time closer to 15 years. Look again at the green/red chart above with a 15-year holding period.

I haven’t quite decided on the exact fund mix, but I have settled on using the Utah 529 plan, as it allows full customization and scheduling of your own glide path with a pretty solid menu of low-cost and passive investment options. Last part of this series will have the full implementation.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

What are your thoughts about how much to save? I have two one year olds and I’ve been struggling to figure out what 18 year target should be? Many of the calculators I’ve looked at have said that in order to go to a state school, paying 50% of their fare, I’ll need to save something like 500/month/kid for the next 18 years. That seems pretty outrageous!

I’m curious on your thoughts.

That’s a good question. My thoughts are… that it’s complicated 😉 There are so many variables, maybe I’ll put my WAGs in another post but they are just that… wild guesses.

I’d take a look at Figure 5 in the Vanguard whitepaper linked above. They make their own batch of assumptions and found that if you take their Aggressive Age-Based portfolio and contribute $3,000 a year starting at birth ($250 a month), and adjust everything for headline inflation (both contributions and tuition cost), you’d have a 95% chance of completely covering an average in-state public school. With the Conservative Age-Based model and the same number, it goes down to 76% chance (but there’s also a bigger chance you’ll miss by more). Still a lot of money, but lower than your quoted numbers 🙂

My wife and I live in Michigan and invest for my daughter’s college education through Michigan’s 529 plan (MESP). While it rarely makes the “best of” list, the TIAA-CREF funds offer fairly flexible savings options and are quite low cost (generally 0.2% or less). Additionally, we receive a slight state income tax benefit. After I read your article, I double-checked our age based selection (Aggressive) and am still pretty well satisfied with its holdings. It holds at least 50% (well technically 49.5%) stocks through age 14. Also, somewhat unusually in my minimal research, it has a real estate/international component and continues stock holdings after age 18. I may supplement this core fund with stock/bond fund purchases, but have been pretty happy with this so far.

Jack – Again, my research is fairly limited, but I MESP’s calculator (https://www.misaves.com/tools/calculator/) to be very helpful regarding how much to save. It allows you to adjust inflation, portfolio return, and, most interestingly, even pick a specific school and view projected attendance costs. By the time my daughter goes to school, the four years at the University of Michigan is estimated to cost $240,000!

Our oldest is six and we’ve been saving since before birth. We currently put $600 per month per child in our 529s and I hope to cover half of their tuition from the accounts when they reach college age if they go to a private university, more if they choose a state school and state schools are still cheaper.

Jonathan,

I recently opened a 529 plan with Utah and have also been debating which asset allocation is best for me. My daughter is only 3 weeks old so I have some time.

When you say 60/40 stock bond, for the bond portion are you thinking just Total Bond Index or are you going to include some of the shorter term bond funds that Utah offers? I was thinking of maybe splitting the bonds between Total Bond and the Short Term TIPS fund that Utah has, but I’m not educated enough on the nuances of the bond funds to make a decision right now.

Sorry if I’m jumping the gun and you are going to talk about this in your implementation post… Thanks for your help.