I’ve already shared two nuggets from the book The One-Page Financial Plan by Carl Richards – the importance of getting started and the true value of a human advisor. But what about the title itself?

I’ve already shared two nuggets from the book The One-Page Financial Plan by Carl Richards – the importance of getting started and the true value of a human advisor. But what about the title itself?

Before even reading the book, I was impatient and tried to make a one-page financial plan but it didn’t sound right. Even after reading it all the way through, I got a bit lost as besides “one-page plans”, it also tried to cover other big topics like budgeting, investing, and insurance. It took a few re-reads before things finally settled down in my mind. Here are the parts that helped the most:

Your one-page plan simply represents the three to four things that are the most important to you: some action items that need to get done along with a reminder of why you’re doing them.

Having done this with hundreds of my clients, I’ve found no more efficient strategy for solving the problem of how to handle our finances than asking “Why is money important to you?” […] If you’re doing this with a spouse, it’s important that each partner answer the question separately.

The reason I ask my clients this question is because it helps us understand their values. Often, the process of asking “Why?”—“Why is money important to me?” or “Why have I been so anxious about money lately?” or “Just why do I work so hard anyway?”—uncovers deep desires and fears that we are often too busy or too scared to think about. While the process can be uncomfortable, recognizing what really matters to you is the first step toward making financial decisions that are in sync with your values.

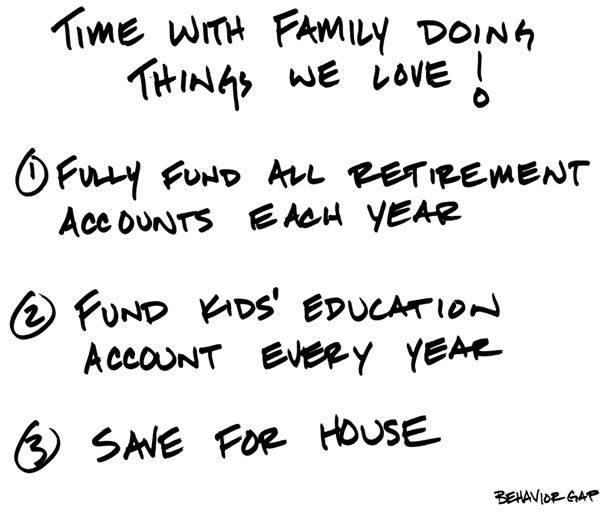

Recently, the author shared his own plan on his website – What Does a One-Page Plan Look Like?:

There are many reasons why my plan (at the top of this post) will be different from the author’s and yours. Our current situation is different, our priorities will be different, our goals will be different.

Why is money important to me?

- I greatly value security, sometimes so much that it is irrational. I don’t want to have to rely on anyone else for money or favors. We cut back on work hours to spend more time with kids, but we still want to make more than we spend. It’s not time to touch that nest egg yet!

- I greatly value spending time with my family, both on a day-to-day basis and for extended vacations in new and strange places. I have to work hard to avoid getting into a rut where the days and weeks all start melding together. Even if it means lugging multiple car seats and strollers everywhere, I still want to stay curious, make some mistakes, have some adventures.

- I want to someday shift my activities such that they more directly give back to my community or some other greater good. I don’t like the idea of just writing checks though, so I need to find a more active and satisfying role. If I could make some money while doing this, that would be great, but otherwise I need to put enough aside that my investments will support me.

The overall point of both this exercise and the book is that improving your financial life doesn’t have to be done perfectly. Just by getting started and putting down your best guess down on paper, you’ll already be better than most. If you see something wrong when comparing your values and your actual behavior, then make some changes. Having done them, I recommend both doing this exercise and reading the book. If your library participates with Overdrive.com, it is available to borrow as a Kindle eBook.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Loved the book. I gift it to anybody getting started.

Might have to check out this book, it’s cool to see the author even following through on his own advice! I like the idea of putting down your plan on paper with a few simple goals and the reasons for doing them. I think it helps you to follow through with those goals and serves as a reminder for why we have the goals we do.

Writing down one’s values is important to stay on task towards one’s goals. When a decision needs to be made, you can go back to your values and say “Is this decision in line with my/our money values? with my/our money goals?”. Spontaneous opportunities make these money values invaluable: You’re in Florida with your good friend and his family- he shows you a newer condo- its the last one available- your friend and his wife owns one in the same complex- and they love it! You get excited. Its a great location! Your money values are the barometer you use to judge if this is in line with your plans. Thanks for the book summary and examples of one page financial plans!

Jonathan, if I may be allowed to play devil’s advocate…

You wrote “I want to someday shift my activities such that they more directly give back to my community” – why not today?

Mostly because I am still working and also raising a 1 and 2 year old with my working wife, and those are higher priorities for me. Right now giving back is via cash charitable donations.

Long time reader – probably never commented before. I am 47 years old. I am a professional earning 6 figures, but my wife stayed home for 10 years with our kids and now works 2 jobs that are barely over minimum wage as we deal with college costs. Our oldest child is a junior at a state school and we are paying for all of it. Our second child will be a junior in high school in the fall and we will also pay for his college. We put money away in 529’s for several years. We live in an expensive part of the country, but have been in the same house for 19 years and paid it off in our early 40’s. It is nothing fancy. We have over a million in retirement savings. I was a volunteer firefighter for 20 years and am just finishing my 12th and final year in elected office as a City Councilman in my town. My wife has been a PTA officer since our youngest entered school. She is also an officer of our son’s Boy Scout troop. We’ve lived a full life and been able to give back to our community.

We drive old cars until they die (or get taken over by kids) and our house is nothing fancy. I am truly “the millionaire next door”.

I just want to affirm that the basis of Jonathan’s post is totally doable. Yes…it can be embarrassing at work for me that I don’t have a boat or a vacation cabin like a lot of my co-workers. But I also had my kids raised by a stay at home mom and I’m also pretty sure they don’t have my retirement account.

I work with people that have lifetime earnings way more than my wife and I have, but are in a financial mess. Just be frugal, people! We still did the Disneyland vacations and all the other middle class rites of passage. My greatest success is that I’m not saddling my kids with loads of college debt.

Not bragging….just giving another perspective from someone that’s done it on way less money than a lot of American families.