There are many excellent insights within Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets by Nassim Nicholas Taleb. A useful everyday tip is that you should accept that you have behavioral biases and that they don’t go away even after you become aware of them. (We all think we are more rational than average.) Instead, we should actively construct ways to avoid them.

There are many excellent insights within Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets by Nassim Nicholas Taleb. A useful everyday tip is that you should accept that you have behavioral biases and that they don’t go away even after you become aware of them. (We all think we are more rational than average.) Instead, we should actively construct ways to avoid them.

One example within the book deals with separating noise and signal (meaning) within investing. Let’s say you have a dentist that can invest with a 15% average annual return with 10% annual volatility. For reference, the S&P 500 index has a ~10% average annual return and ~14% average annual volatility. The dentist has good thing going, with the portfolio doubling in value every 5 years on average.

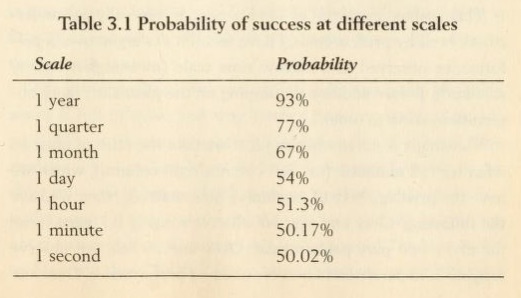

An unexpected factor in his success is the frequency upon which he looks at his portfolio balance. Here’s a chart from the book showing the probability of a positive change in value based on how often the portfolio is checked.

If he were to check his portfolio every minute, he would only see a positive return 50.17% of the time. That is basically indiscernible from a coin flip. The problem is loss aversion.

Being emotional, he feels a pang with every loss, as it shows in red on his screen. He feels some pleasure when the performance is positive, but not in equivalent amount as the pain experienced when the performance is negative.

At the end of every day the dentist will be emotionally drained. A minute-by-minute examination of his performance means that each day (assuming eight hours per day) he will have 241 pleasurable minutes against 239 unpleasurable ones. These amount to 60,688 and 60,271, respectively, per year. Now realize that if the unpleasurable minute is worse in reverse pleasure than the pleasurable minute is in pleasure terms, then the dentist incurs a large deficit when examining his performance at a high frequency.

Again, this doesn’t go away even if you know about the phenomenon:

Regardless of what people claim, a negative pang is not offset by a positive one (some psychologists estimate the negative effect for an average loss to be up to 2.5 the magnitude of a positive one); it will lead to an emotional deficit.

Now, if he were to check that same portfolio only when his monthly statement arrives, he would see a positive return 67% of the time (2 out of 3). Finally, if he has the patience to check only once a year, she would see a positive return 93% of the time. The time scale matters.

Unfortunately, the S&P 500 is not quite that good, but it has posted a positive total return roughly 75% of the time from 1928-2017. (Total return includes dividends. You’ll get a slightly lower number if you just look at the index without dividends.)

This becomes even worse during bear markets when the down days outnumber the up days for a while. Our brains are simply not well-suited to handling that kind of repeated pain. The solution is to block out the noise. Don’t check your portfolio as often and over time, you will hopefully experience a lower likelihood of bailing out during a market drop.

This is the reason why I don’t do monthly asset class returns any more, and only do them annually nowadays. There is too much noise in monthly returns. I wish I could say I only look at my portfolio annually, but that is starting to sound like a good idea too!

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Although I might look at specific investments I own after a day or two of market volatility, I have disciplined myself not to consider any sells or asset allocation re balancing until quarterly results are available. Even then, I’ve found that most of the time I generally re-balance just once or twice a year. I only act if an investment class is +/- 5% from it’s target allocation, and I’ve found — interestingly — even with the volatility of recent years — it takes a long time for any one class to exceed that threshold. I find investment and financial matters too interesting not to look more than once a year – don’t see that changing any time soon!

Rebalance once a year in January and then forget about it.

Some real wisdom in this post, Jonathan.

I’ve read three books by Taleb. This one and “Skin in the Game” and his most famous, “Black Swan.”

Once we’ve decided which large index funds are right for us, once a year is just right.

Has been for me, anyway, for a decade or more now.

Though I’d be rich if I could recognize the end of bull markets. Ha, and the end of bear markets too.