A few days ago, the US Department of Commerce released1 that the nation’s savings rate for 2006 was negative 1%. This means as a whole we spent more than we earned after-taxes, again. (It was also negative for 2005). Much is being made about how this is the lowest savings rate since the Great Depression, when there was a negative 1.5 percent rate in 1933. Should we be worried? Is the sky falling?

What’s the recent trend?

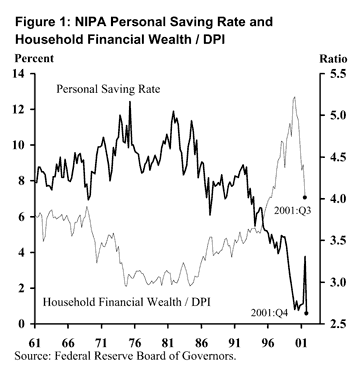

I wonder what the margin of error is on this data. Looking at this graph, it seems like perhaps something happened about a year and a half ago? But then I found it goes back a lot further than that. This chart starts from the 1960s2:

To help better understand the numbers, you have to go into the definitions a little bit. The personal savings rate ignores the capital gains in our investments like stocks and bonds, and also tangible assets like cars and real estate. In fact, our overall net worth is not doing that bad and actually increased over last year. The graph above tracks this by dividing household total wealth by disposable personal income (DPI). There are a few ways the experts try to explain this:

One theory is that this “wealth effect” makes us feel like we don’t have to save as much right now. Look at the graph from 1990-2001… stock market go up, savings go down. I can see this – recently both the stock market and housing prices have been flying high simultaneously. If your overall balances are skyrocketing, it’s much easier to justify buying that new car or trading up into a bigger house. Maybe people just need a good scare. Or a sudden drop in spending would lead us into a depression. Sigh.

The problem with this data is that it doesn’t separate out the very rich and the poor, and thus really reflect how the majority of people are doing. Even though the net worth numbers make things look better, the top 20% of households by wealth have 15 times the net worth of the median household. The top 20% by income make 50% of the total income. Only half of Americans even own stock, let alone have capital gains to worry about. What would happen to these charts if you took out the top 20% richest people? Are the big earners also the big spenders? Or are the lower 80% of people both spending too much and not seeing any gains in net worth? I’m curious.

Another theory is that all of this easy credit is letting people borrow from their home equity or future earnings with a click of a mouse or the swipe of a card. Our debt-to-income ratio is certainly on the rise3:

Perhaps the government should be a better fiscal role model! 🙂 Maybe we just need to adjust our standards. The size of the average house has doubled since the 1950s, while family size has actually shrunk. Mainly, I just get the feeling that a lot of people are going to be working for much longer than they think they are…

Sources:

1Bureau of Economic Analysis, Personal Income and Outlays 12/06

2Federal Reserve Bank: What?s Behind the Low U.S. Personal Saving Rate?

3Federal Reserve Bank: Spendthrift Nation

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

perhaps the negative correlation between net worth and savings isnt a bad thing. naturally if people arent saving, they are spending. but perhaps that spending is constructive debt such as mortgages, loans, etc. that are being used to increase wealth. thats what consideration.

another consideration is where these numbers came from? how do they define savings? if savings does not include new investments in the stock market or other assets, then this entire study is flawed.

in fact, where the US economy is today, it makes little sense to sock money away in a bank account.

i ask these questions because i dont know all the details, maybe you could follow up in an additional post?

I’m still not 100% sure how they figure all this stuff out either, but the savings rate is basically after-tax income minus expenditures. So it is designed to include contributions to savings accounts, IRAs, 401ks, 403bs, 529s, and so forth.

Paying the bills and buying stuff like groceries and clothes are all expenditures as you’d expect. However, if you bought a house (a tangible asset) and put 20k down, that would still count as an expenditure. Same for paying cash for a car. And spending towards education.

So you can argue about the true numbers being really negative or not, but the trends still don’t look good.

So if you had $1 in your savings account, you are better than the national average? I dont know what these things mean…seriously, thats why I read your blog.

Yes, according to this report if you saved $1 in your ING account and didn’t incur any extra debt this year, you beat out the nation on average.

I might tackle this topic for a research paper in my econ class. Any additional comment or info is welcome.

I did a little research on this to try to figure out what these figures meant when these headlines started popping up. It is maddeningly difficult to find a straight answer as to what is included in the NIPA rate.

In the area of housing, I seem to recall that paying down mortgage principle was included as savings. I believe that in an owner-occupied dwelling, the portion of your mortgage that went against principle was computed the same as if you had received it in rental income from a tenant (in this case yourself). So the outlay of paying mortgage principle and your “rental income” cancelled each other out.

“There are serious measurement shortcomings with saving statistics, which call into question the extent of a “real” savings problem. For instance, personal savings measures omit increases in the values of people’s homes and the equities they own, including those in their pension accounts. Personal savings also ignores corporate saving (retained and reinvested earnings), which are ultimately personal saving, as stockholders own those corporations. The magnitude of these problems is indicated by the fact that the Federal Reserve not long ago found that household net worth increased by over $5 trillion while personal savings were officially negative.”

http://blog.mises.org/archives/006216.asp

well, like u said, how do you define savings? but cash is always king and u cant buy something wiht stocks..plus capital savings allow for future investments. i would say its a problem..b/c when u constantly spend more than u earn, eventually u are going to have to pay the reaper. once in awhile, fine..but consistently overspending means one day the debt man cometh and u got nothing for him…when that happens, our economy will be severly shocked.

in other news, im starting to do the 0% game and was wondering how come u cap out at 30k? personal choice or debt ceiling? just wondering.

thanks for the comment on my site too

I guess that this translates to the growth of GDP because of 2/3 of GDP belongs to personal spending. No spending, no growth of economy.

I personally think it’s great that we have such a horrible savings rate. Income inequity is what allow those who are fiscally prudent to get ahead. The 20% are investing in companies depending on the 80% to blow their money the goods and services offered by those companies.

Quick Thoughts:

– If we’re spending more than we earn, than means we’re either incurring more debt, spending home equity or liquidating securities.

– If we’re not saving our income, than that also means that there is less cash available for future investment AND that we’re spending up our current investments.

– Home Equity shouldn’t be a factor IMO, as you either have to borrow against it to use it OR you have to sell your house and trade down to a smaller one. How many people actually do that?

I work in the tech industry going back and forth between Silicon Valley and Seattle, I can think of quite a few people who sold their homes and walked away with a TON Of cash. Only two actually traded down the rest rolled the cash into a new house/spent the bulk of it one way or another.

As Jonathan said, I think the best way to view the data is to adjust it:

– Savings rate per income percentile

– Savings rate with the top 20% removed

– Net Worth increases with the top 20% removed

I think we’d get a better picture

50% of the population doesn’t own stock, not everyone lives on the coasts with booming housing prices (that’s going away anyway).

The data should really depict the following:

– For Americans in the middle 60% of income earners, what % of their income is saved?

– How much debt are they incurring?

– What % of people in the middle 60% of income earners are utilizing home equity as an income supplement?

– What is their rate of net worth increase?

Considering that the top 20% earn 50% of the income and control an outsize portion of the wealth, keeping those folks in there really skews the data IMO.

-Mark

Would it be the same if one said…national debt average increased by 1%?

Last night while trying to go to sleep, I realized that if Bill Gates bought every SINGLE person in the whole wide world a $1 McChicken, $1 drink and $1 fries…..($3 * 6 billion)

He would have only spent $18 billion and have a balance of around $32 billion. It also made me think that this guy has so much cash that he could actually buy out so many companies if he wanted to!! He could have personally owned YouTube if he wanted to. I think he should have and linked it to the dying hotmail account!! Hotmail needs to be ‘coolified’ (made cool)

I may be wrong about the mortgage comment above. I read that changes in values of asset don’t count and rent was an expediture. Payments towards mortgage principal may very well be counted as savings.

As for getting out home equity, look up reverse mortgages. I predict that they will be a booming industry soon in many areas. I already see ads for them now.

Another thing on my mind is the rapid “spending down” many older folks (and their families) do in order to qualify for Medicare. It can be profitable to look poor.

—

Here’s another graph I left out of the original post:

Ratio of personal expeditures divided by GDP vs. time.

It is very intersting that the graph has been declining very steadily since 1985 or so. Clearly whatever is going on, it’s been at work for a long time. I’ve read that he “actual” savings rate is more like 3-4% when you factor in that retirees (e.g.) are spending down their 401(k)’s, and the 401(k)’s have grown in value. So don’t feel too proud of that extra $1 in your savings acocunt! 🙂 But I think that the wealth effect is in play, and it gives me pause. Basically, it reminds me of the San Diego pension crisis. As I understand it, San Diego started counting investment gains as “contributions” and hence stopped fully funding their pensions. Then when the market stopped growing at boom-time rates, they found themselves billions in the hole. Scaling that down to individuals, if the median 401(k) balance for 50 year olds is $60K, I think we need to save more, and borrow less, no matter how well the markets are doing.

we’re also at the highest debt levels. the high DTI is a big factor in negative savings. The negative savings isn’t surprising, as we see more unsecured debt taken on by consumers as well as people with higher than sustainable secured loans like interest only mortgages. People simply want things beyond their means. It’s intersting that IO mortgages preceded the depression then became popular again leading up to these neg. savings years. to me, it’s simply an indication that people are overextending themselves. there is also the fact that although real income increases, people tend to spend it rather than save it.

i do wonder, though, how much of an impact that the 2002 crash, worldcom, and enron had on these figures considering that people lost lots of networth and savings.

i’m also mixed on the way figures are calculated, but all things being equal since the calculations are the same, the figure is more interesting as a trend.

The low savings rate is a HUGE problem. This chart portrays the structural problems with the economy.

People are INCOME savings poor and ASSET savings rich. The ever-growing debt loads of the economy are providing the liquidity needed to increase asset values via abnormal profit margins for corps, low debt spreads on bonds and low interest rates on mortgages.

In theory, net worth goes up. However, a lot of that is from the liquidity cycle. If that cycle stops and asset prices fall, the ‘typical’ worker does not have the income based wherewithal to sustain his standard of living.

This is all tied into large trade deficits, high stock, bond, house and commodity prices, and job loss in manufacturing (and increasingly services) vs. emerging markets.

Since all of us here are so savings-oriented and mindful of our retirement goals, it’s amazing to me that the average can be so low. Not even low like saving 2%, but to actually be at -1%.

And that’s an average – so there must be people that consistently spend 5% or 10% more than they make. Incredible.

Do not blame the American consumer.

Almost the entire U.S. economy is based on consumption – see Jonathan’s GDP chart link:

https://www.mymoneyblog.com/images/0702/saving3.gif

The Fed used to control our spending with interest rate hikes and conservative $$ printing. Those days are over.

After 9/11 the Gov’t/Fed decided to save the economy by increasing spending. The savings/locked-up home equity/fair valuation of assets was jettisoned with low interest rates to avoid a needed recession.

Negative savings makes sense in an economy where the value of the U.S. $ is declining rapidly. The American consumer is doing what makes sense in a looming hyperinflationary era: getting rid of dollars.

Why I think’s it useful:

– it’s a major part of GDP. If it’s negative lately because of housing & stock appreciation, what will happen with the housing market lands and the bull market cools? Will people keep over spending if their networth stabilizes or starts going down?

– how does it compare to your personal situation? Ignoring networth for a second, did you sock away cold hard cash last year, or are you in with the spending herd, in a risky situation?

– how is the U.S. trend compared to that of China and other countries? I think the Chinese savings rate is north of 30%. That implies that there GDP can get even bigger, with some good consumer marketing to the Chinese consumer.

-Wes

i like the term “overexuberance” that the Fed uses. i think it is bettered thought of as a trend vice a real figure. you figure that the vast majority of wealth is heald by a small fraction of the u.s. population. so if there is a negative savings, that just means people are dumping cash reserves. it shouldn’t be a surprise then that savings rates banks are offering is higher with less cash reserves on hand.

also if net disposable income is up and people are spending, it is the reason for the u.s. economy still being healthy.

the problem with china is that they have too much cash reserves. The good thing for the u.s. it is primarily u.s. dollars and they can’t really spend it anywhere else except for in the u.s. and on u.s. goods.

Jonathan — I think you are mistaken on this point:

“So it is designed to include contributions to savings accounts, IRAs, 401ks, 403bs, 529s, and so forth.” I don’t think you are right.. and this mistake explains the dichotomy of what is going on. There is no negative savings rate in America precisely because PRE-tax investing like 401ks is not being counted.

?By the way, if you notice the charts, pre-tax saving peaked at 11% in 1977. A year later, 401 Ks came into being. It has been downhill from there.?

link

Quick question, what is the main difference separating investing and saving? Isn’t it the risk factor as well as investing lies at the mercy of the market?

I ask this because the project that originated from this topic that I was assigned has me a little confused as to how I should be wording it to educating young adults.

There’s a graph in my classroom demonstrating the benefits of starting to make INVESTMENTS when you are younger, even though the name of the larger benefitee in the graph insinuates saving…

I appreciate Clicclic’s contribution that (I think) we are wise in spending dollars that are becoming worthless as the Fed dilutes their value. But are we trading those dollars for something of value that we can use later (possibly a way of saving) or are we trading them for things that have declining value (consuming)? For example, could purchase of a flat screen TV be considered saving if one had otherwise saved dollars and then purchased a TV at possibly higher price (due to inflation) and after losses to taxes?

A similar thought may apply to investments. If taxes plus inflation are greater than the increase in value in dollar terms, then there is as little incentive for investing as there is for saving. But how to preserve money? Investing in housing seems slippery now. Perhaps land. Perhaps gold. What do you think?

I made a rigorous math proof years ago that change in savings is a function of growth. The keyword is “change.” While growth may be positive savings can be negative.

See also my correlation between imports and savings decline at http://knol.google.com/k/cheng-wu/savings-rate/3mfkvo9c0qndy/2