My last update on the PeerStreet bankruptcy was about a year and a half ago. PeerStreet marketed high-interest investment loans backed by real estate in $1,000 fractional increments. A few days ago, I received a big, thick envelope with lots of legalese. It appears that actual humans are manually going through each claim and verifying them against their database.

For my part, I have two $1,000 notes that are still outstanding and have been in default for a while, well before PeerStreet declared Chapter 11 bankruptcy in 2023. The bankruptcy administrators mostly agreed, but needed to point out that my notes are not “secured” claims, but instead are “Mortgage Dependent Promissory Notes” (MPDNs). Here are notes specifically responding to my claims:

The Claimant asserted a secured claim for $1,000.00, but attached a copy of a MPDN supporting a MPDN Claim in that amount.

The Debtors’ books and records reflect that the Claimant is entitled to Investment Claims in the amount of $1,000.00, as reflected in the Modified Filed Claim column.

Reclassification Adjustment: The Debtors’ books and records and the MPDN support Investment Claims and reflect that the Claimant is entitled to MPDN Claims, not secured claims. The Claimant asserts that the secured claim is secured by real estate, but provides no support for the assertion. Accordingly, the Plan Administrator requests reclassification of the asserted claim to a MPDN Claim (Class 10, 11) (to the particular MPDN reflected in the Debtors’ books and records) in the amounts reflected in the Debtors’ books and records, as detailed in the Modified Amounts column.

With this adjustment, the Plan Administrator seeks allowance of the Investment Claims in the amount of $1,000.00 against Peer Street Funding LLC, as reflected in the Modified Filed Claim column, which matches the amount of the Investment Claims in the Debtors’ books and records.

The Claimant filed two claims for two distinct MPDNs. The other claim, Claim No. [redacted], is also addressed below.

Now, this is what PeerStreet used to say about their “Mortgage Dependent Promissory Notes” (MPDNs) on their FAQ:

A mortgage-dependent promissory note, or “MDPN,” is a note in which an investor receives stated interest and principal, provided the borrower makes payment on the underlying loans. PeerStreet issues an MDPN to investors, meaning they have a direct interest in the underlying loan and indirect interest in the underlying property.

The following is a partial excerpt of what the bankruptcy documents state about MDPNs:

For avoidance of doubt, although MPDN, RWN 1-Mo., RWN 3-Mo. and PDN Claims are all unsecured, holders of those claims are entitled to their pro rata share of the relevant Underlying Loans. All amounts paid with respect to those Underlying Loans are made available pursuant to the Waterfall in section 2.6 of the Plan even if those payments result in holders receiving recoveries in excess of the principal amount of their notes and accrued interest as of the Petition Date. See McLaren Declaration I 10. Notwithstanding this entitlement, however, the Plan provides that distributions on account of MPDN, RWN 1-Mo., RWN 3-Mo. and PDN Claims are made on a pro rata basis for the claimants’ proportional share of the asset or pool of assets tied to such Investment Claims. See Plan § 4.3. In order to properly calculate each holder’s fractional, pro rata share of a particular class of Investment Claim, each Investment Claims’ pro rata interest in the underlying asset or pool of assets tied to such Investment Claims must be measured as of the same date. As a result, postpetition interest needs to be removed from all Investment Claims.

Back in 2018, this all sounded fine. Andreessen Horowitz and other VC firms invested in over $121.9 million. Famous investor Michael Burry put in $600,000 of his own money. Actual, smart lawyers were saying that this was the only practical way to create these fractional investments for real estate loans. We all were comforted by the creation of “bankruptcy remote entities”.

Even if it was really an unsecured note backed that was contractually linked to another loan to a specific property, we’d still only get that money if it was collected by what was basically a small, risky start-up fintech business that may have nobody around to well, collect anything.

My current opinion is that even if the contracts technically still might be the best workaround available, I feel the practical execution and mismatch in the alignment of interests made everything fall apart. PeerStreet was no good at servicing the loans and getting the deadbeats to pay up. They also didn’t have enough skin in the game to care. They didn’t actually hold any loans themselves, they just took a small commission off the top. They were also incentivized to loosen their underwriting standards to feed the voracious demand for new loans given their early success.

I strongly feel that if every PeerStreet executive had to hold a certain slice of every single PeerStreet loan themselves, then things would have turned out differently. Their own net worth would be at risk. They would underwrite better. They would work harder at debt recovery. Just like a certain sub-prime mortgage crisis…

In the end, I put some experimental money into multiple real-estate loans, and thought that PeerStreet was best-in-class. I am fortunate that my overall return is positive, even assuming a complete write-off of my remaining two notes, but I know that many fellow customers were not that lucky. Given these new bankruptcy documents, it seems that there are still people working on the situation and there is a possibility that I will recover some money on my last two loans.

Even today, I still get e-mail pitches for new fractional real estate start-ups. I pass on them all. In the end, the most important promises of fractional real estate are broken:

Your investments are NOT secured by real estate. In every case that I’ve seen, you invest in “notes” that are “linked” to a real mortgage on a real piece of property. The problem is that your name is not on the property, not on the mortgage, and you don’t have any control over the servicing of that mortgage. The legal gymnastics that they did to be able to use the words “direct interest” do not change the fact that you are really just lending money to a tiny, risky start-up to handle everything.

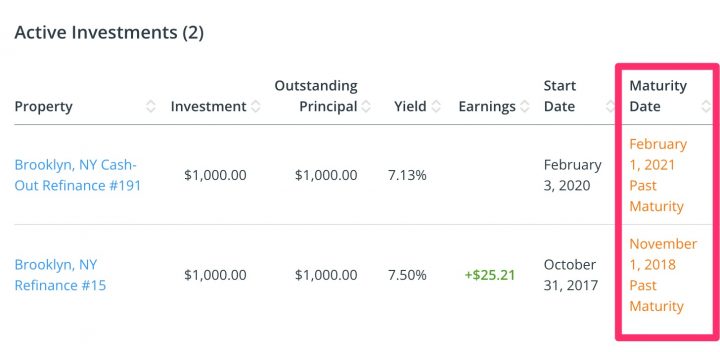

Even if these notes were secured by real estate, I have seen no evidence that PeerStreet had any skill as a servicer able to recover funds from a foreclosure. Let’s take my two Brooklyn loans from 2018 and 2021. I don’t see any possible scenario where if you sold off those properties today in 2025, even in a fire sale, even if the initial appraisal was off, that you would not be able to recover the full value of the notes. It’s not like we had a crash – real estate values have risen so far up since then!

Even if PeerStreet was still fully in business, I wonder if it would have made a difference to my situation. It has been nearly 7 years since my earliest loan was due! Now that they are bankrupt and those same smiling executives have trotted off to their next shiny business, the alignment of interests is even worse. Maybe I’ll eventually get some of this money back, but after waiting for years, my faith in the ability of these real estate fintech companies is shot.

These facts change the risk/return balance on these debt instruments. The upside is maxed out at the interest rate you charge, maybe 7% to 10%. The downside was supposed to be very, very limited because you had a physical piece of real estate to back it up. If that doesn’t hold, then there is no point.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Interesting data point on the individual property linked notes. RealtyMogul works more like a typical broker and their model seems to be intact.

It depends, RealtyMogul sells different parts of the equity/bond stack. They have fractionalized private REITs, which are more of an ownership interest with limited liquidity. They also sell debt, and I don’t know the details but I’d be careful.

The fact that they just now sent you a thick packet of legalese regarding two loans is ridiculous. Couldn’t this be communicated to you electronically, like a year ago!? No wonder why it’s taking forever to finalize the claims. While there was definitely smoke and mirrors that obfuscated the facts, we knew years ago that these would be treated as unsecured claims per the language in the contracts. The inefficiency of this bankruptcy is astounding.

You’re telling me, consider that the borrowers for my Brooklyn note defaulted on their mortgage back in 2018 and it’s 2025 and they are still collecting rent on their property probably. Honestly, the takeaway here is that we should have borrowed money instead with minimal down and defaulted right away and collected rent for 7+ years. The court system overall is much slower than I thought it would be.

Or that court system in NYC always sides with the deadbeat borrower who often takes advantage of the lender. Un0dosclosed geographic policy risks

Would REITs qualify as fractional real estate in the sense you mean here? Or do you think they are a more sustainable investment model?

Public REITs are pretty well established, and are a ownership interest in a publicly-traded company. I wouldn’t really call shares of an REIT, fractional real estate, which is more of a fractional interest in a specific piece of real estate. Private REITs have also been around for a long-time, although they are less liquid and may have higher fees. Personally, I prefer ownership interest via a public REIT index fund through Vanguard (VNQ).

PeerStreet was loans linked to a specific mortgage on a specific property. So it’s debt, not equity. It was more along the lines of a hard money loan, historically fast-closing loans at high interest rates backed by real estate.

Thank you for the update Jonathan !