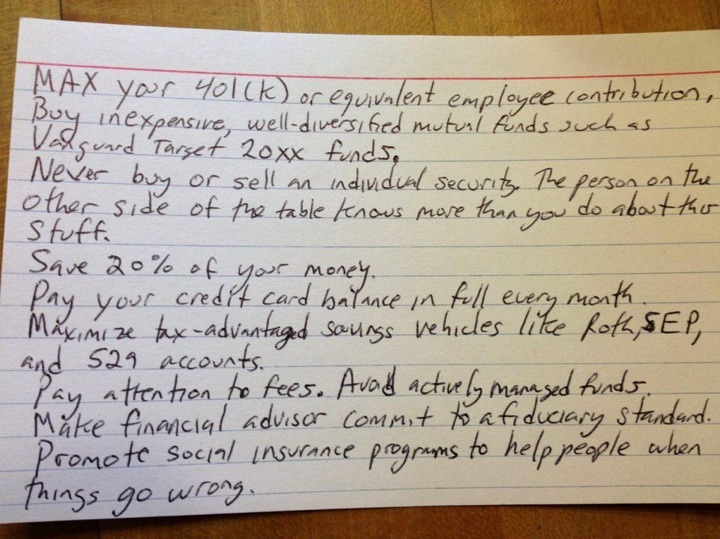

A few years back, Professor Harold Pollack quipped that everything you really need to know about money fits on a 3×5 index card. Folks asked him to prove it, and the resulting handwritten card went viral. Eventually, the idea became a book cowritten with Helaine Olen called The Index Card: Why Personal Finance Doesn’t Have to Be Complicated. Here is the original photo:

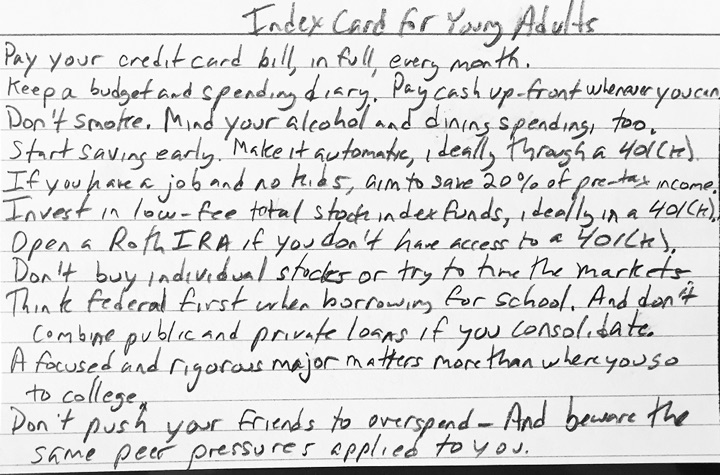

Via Abnormal Returns, I learned that Dr. Pollack recently created a new index card targeted at young adults under 30. Here again is a photo:

In case you can’t make out the handwriting, his tips are as follows:

- Pay your credit card bill in full every month.

- Keep a budget and spending diary. Pay cash up front whenever you can.

- Don’t smoke. Mind your alcohol and dining spending, too.

- Start saving early. Make it automatic, ideally through a 401(k).

- If you have a job and no kids, aim to save 20% of pretax income.

- Invest in low-fee total stock index funds, ideally in a 401(k).

- Open a Roth IRA if you don’t have access to a 401(k).

- Don’t buy individual stocks or try to time the markets.

- Think federal first when borrowing for school. And don’t combine public and private loans if you consolidate.

- A focused and rigorous major matters more than where you go to college.

- Don’t push your friends to overspend. And beware the same peer pressures applied to you.

Sound, simple advice. But simple is not easy, and it can be hard to pull off everything on this list. I recommend using the card to help focus your efforts.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I take strong issues with #9 on the first card. The other eight suggestions are all personal finance decisions, the ninth is promoting a political opinion. “Promote social insurance programs” is requesting political action, not personal decisions. It is called “personal finance” for a reason, we each need to take personal responsibility!

It is a indeed a bit different from the other items. But I think it’s reasonable to include, because even if someone follows all of the previous items, in extreme cases of misfortune, they won’t be able to take care of themself anymore. For the average American, if they are in a serious accident or fall ill to the point where they can no longer work, they will require assistance. Where that assistance comes from (government, family, church, etc.) is a political question, but the card does not go into that.

To pretend that every person can fully take care of themselves in any situation if they just take personal responsibility is fantasy. And once you acknowledge that their are situations where a person would need help, there’s even an element of self interest in promoting social insurance, because you may be the one who needs it one day. (Unless you are ultra wealthy, in which case the rest of the card doesn’t really apply anyway.)

On the contrary, many of the above investment vehicles are also social insurance programs. The IRA saving vehicles, 401(k)s, 457s, are not just personal decisions, but also government programs which allow some to benefit through tax breaks and deferrals. These programs haven’t been around forever, and in offering them the government gives up quite a bit of revenue. They are a kind of social program that costs the government and benefits some more than others, in this way quite a bit like food stamps, etc.

Besides urging philanthropy, I think the professor was cognizant that pretty much all mainstream saving plans (ie, not hoarding guns and gold) need to happen, happen best, in the context of a stable society connected by good individual husbandry AND social programs.

I think the author is overselling IRAs/401ks. Related, I don’t agree they are social programs. What ever you say about a regular IRA, “allow some to benefit through tax breaks and deferrals”, the opposite is true for Roth IRAs. You wouldn’t say roth IRAs are anti-social programs.

I’m assuming the rationale for maxing out both a 401k and a roth IRA is the assumption that it forces you to save when you otherwise wouldn’t. Otherwise, it makes no sense. Either you think you’ll make more money in the future and/or tax rates will be lower (in which case the 401k makes the most sense) or the opposite is true (in which case the roth makes the most sense). If someone just saves the same amount of money yearly in a non-retirement account we wouldn’t expect them to be any worse off then someone maxing a 401k and roth ira at the same time. I would actually expect them to do even better as they wouldn’t be constrained by their investing opportunities and they would have more flexibility to claim gains/losses at the most opportune times

Kevin, I think you are overlooking two benefits of the 401k/Roth IRA approach.

1) Both avoid the drag of annual taxes on their gains.

2) A retiree with both pre-tax and post-tax retirement accounts can strategically draw from the pre-tax account in lower income years to minimize taxes.

There is one negative aspect of 401k accountss that I don’t see discussed much: distributions are taxed as normal income, so a buy-and-hold investor misses out on the lower long-term capital gains tax rates. Figuring out the magnitude of this effect requires a lot of assumptions, which is probably why people don’t talk about it that much.

Annual taxes are no more of a drag then paying the same amount of taxes (adjusted for compounded earnings) once.

Thats a good point about number 2. And I’m certainly not claiming there’s no benefit to retirement accounts, just that the benefits are over rated.

I don’t know what you mean by “adjusted for compounded earnings.” Compounding is the reason that there is a benefit to avoiding annual taxes.

I like your final comment. It’s simple advice but it’s hard to do. Truer words have not been said. The devil is always in the details, and it could be applied to healthy eating, and many other things that people should do.

hi Jonathan,

I few weeks ago you posted your free excel calculators from different sites. I can’t find that post. Could you please suggest where is it located?

Thank you