Here’s a final update on my investment portfolio holdings for 2014. This includes tax-deferred accounts like 401(k)s and taxable brokerage holdings, but excludes things like physical property and cash reserves (emergency fund). The purpose of this portfolio is to create enough income to cover all of our household expenses.

Target Asset Allocation

I try to pick asset classes that will provide long-term returns above inflation, distribute income via dividends and interest, and finally offer some historical tendencies to balance each other out. I don’t hold commodities futures or gold as they don’t provide any income and I don’t believe they’ll outpace inflation significantly. In addition, I am not confident in them enough to know that I will hold them through an extended period of underperformance (i.e. don’t buy what you don’t understand).

Our current ratio is roughly 70% stocks and 30% bonds within our investment strategy of buy, hold, and rebalance. With a self-directed portfolio of low-cost funds and low turnover, we minimize management fees, commissions, and taxes.

Actual Asset Allocation and Holdings

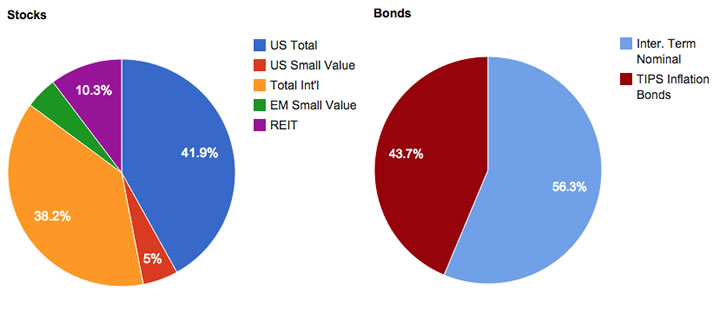

Stock Holdings

Vanguard Total Stock Market Fund (VTI, VTSMX, VTSAX)

Vanguard Total International Stock Market Fund (VXUS, VGTSX, VTIAX)

WisdomTree SmallCap Dividend ETF (DES)

WisdomTree Emerging Markets SmallCap Dividend ETF (DGS)

Vanguard REIT Index Fund (VNQ, VGSIX, VGSLX)

Bond Holdings

Vanguard Limited-Term Tax-Exempt Fund (VMLTX, VMLUX)

Vanguard Intermediate-Term Tax-Exempt Fund (VWITX, VWIUX)

Vanguard High-Yield Tax-Exempt Fund (VWAHX, VWALX)

Vanguard Inflation-Protected Securities Fund (VIPSX, VAIPX)

iShares Barclays TIPS Bond ETF (TIP)

Individual TIPS securities

U.S. Savings Bonds (Series I)

Notes and Benchmark Comparison

There was very little activity during the last quarter of 2014. I’ll need to do some rebalancing in the beginning of 2015. I did change my asset allocation tree above to reflect that my bond holdings have a weighted duration of close to 4 years now. It used to say “shorter-term” but really now it is more “intermediate-term”. I’ve been putting my new bond money into VWIUX, which holds intermediate-term high-quality municipal bonds. I haven’t sold any of my limited-term holdings. Overall, it’s a little longer in maturity and a little higher yield, but nothing drastic. I don’t really listen to future rate predictions; they’ve been wrong more than they’ve been right.

I’ve already noted the 2014 performance of each individual fund here along with my overall portfolio total return of roughly 6.5% for 2014.

A simple benchmark for my portfolio is 50% Vanguard LifeStrategy Growth Fund (VASGX) and Vanguard LifeStrategy Moderate Growth Fund (VSMGX), one is 60/40 and one is 80/20 so it also works out to 70% stocks and 30% bonds. That would have returned about 7.1% for 2014. One reason for my portfolio’s relative underperformance to this benchmark is my inclusions of TIPS bonds which returned 3.5% whereas the Vanguard Total International Bond Index Fund (BND) returned 6% for the year. I’m still happy to hold TIPS. If I had more tax-advantaged space and/or a lower tax rate I’d hold BND instead of muni bonds but I’m still happy with my muni funds as well.

In a separate post, I will update the amount of income that I am deriving from this portfolio along with how that compares to my expenses.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

” I don’t really listen to future rate predictions; they’ve been wrong more than they’ve been right.”

Isn’t that the truth! 🙂 And for the long term investors… who cares what rates will be next year or in two year? Doesn’t matter.

You are more tilted to international exposure than a lot of folks I see. Any particular reason for that?

My US/non-US breakdown is very, very close to the actual breakdown if you were to weight each country by total market value. Some people prefer to have a “home country bias” but I think this gives me better exposure to the world market, wherever capital flows.

Jonathan, are you planning to only use this portfolio for income or to also “spend it down” at some point? Would be interested in your thoughts as I plan my journey as well

I’m not sure yet, as I get closer I’m trying to get a feel for how much dividend + interest income I can generate and how variable that income will be. I’m trying to imagine living off the quarterly dividends from my stock funds and monthly interest payments from my bond funds.

Since hopefully I will have a long spending period, I’d love to only have to spend the dividends + interest. I’m also considering putting a chunk into a rental property for some income diversification, but I’d rather not if I don’t need to.

Cool. Can’t wait for your portfolio income v/s expenses post

Jonathan – a very long time follower of your blog (back from the days when you were posting real dollar amounts in portfolio updates :). I was just wondering if you have any particular affiliation towards index funds as opposed to ETFs, VTSMX as opposed to VTI. Is your portfolio predominantly index-fund based as opposed to ETFs? I get that both have more or less same returns and you go for ETFs if you dont have enough capital to meet the minimum fund requirement, my question is if you started off with ETFs and kept on adding year after year, does it really matter if you just keep the ETFs or are you better off switching to the index funds? Thanks for years of useful advice on investing..

It doesn’t matter all that much, but if I could, I would have all index funds. I like being able to get the same tax advantages as ETFs from my mutual funds (due to the unique set-up that Vanguard has) while also getting a guaranteed buy price at NAV (something you don’t get with ETFs). I don’t have to worry about bid/ask spreads with index funds. I can also invest whole dollar amounts with mutual funds. I don’t care about buying intra-day.

That said, I have both because I bought ETF versions when their expense ratio was lower and due to the tax implications of selling them I am keeping them indefinitely. You can convert from mutual fund to ETF but not the other way around. Hope that helps. 🙂

https://www.mymoneyblog.com/vanguard-mutual-fund-to-etf-share-conversions.html

If you were younger do you think you would still have 30% in bonds? I’m in my mid-30’s, and planning for long holds on all my stock investments. As a result, i feel like having my money in bonds would be costing me potential gains (even in the terms of a market dip, i have the time to recover). Curious your take? Great site