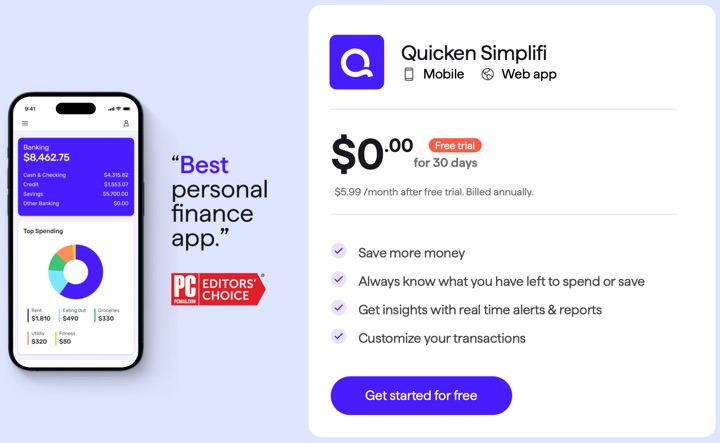

Quicken Simplifi is running a free 30-day trial of their personal finance app. Simplifi is their app-first “Mint-like” software that aggregates all your accounts daily, tracks spending, categorizes for budgets, analyzes investments, and all that. They also still offer their desktop-first Quicken Classic software (although Simplifi has a web interface and Classic has a companion app…). After the free trial, the cost is “$5.99/month, billed annually”, in other words… $71.88 a year. They’ll want your credit card at sign-up, so be sure to set a calendar reminder to cancel. They’ll tell you the date.

I haven’t replaced Mint with anything myself (I ending up deleting all accounts from Credit Karma and just directly log in to websites now), so I will give this a shot. Simplifi won the best budgeting/personal finance app from Wirecutter and PC Mag, but I’d also like to see how it handles investments. It doesn’t look as robust as Empower Dashboard (formerly Personal Capital) (most recent portfolio update). 30 days should be enough time to settle in and feel if it’s worth the cost. Offer ends soon on 9/30. The fine print:

30-day free trial only available to new customers. After 30 days, you will be billed at the then annual price. All offers are for the first year only when you order directly from Quicken by September 30, 2024, 11:59 PM PT. Offer good for new memberships only. Subscription billed annually. Offer listed above cannot be combined with any other offers. Upon the end of your membership term, the subscription will automatically renew at the then-current rates, unless you cancel or we terminate this agreement.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Curious to know what turned you off using Credit Karma. I’m finding it a suitable replacement for MINT in spite of more aggressive advertising.

I agree, CK isn’t horrible, but I suppose the experience degraded to the point (I feel Mint got a bit worse over time first) that I rarely checked things using Credit Karma anymore with the use of password managers and 2FA these days, so I didn’t want them to keep having data access to all my accounts forever. I think it still serves a useful purpose as a free account aggregation tool.

I switched to Copilot (https://copilot.money) from Mint/CK. It’s simple, easy to use, handles investments and not built by a mega corp so hopefully they can survive on subscription fees ($95/yr). Also, they aren’t trying to upsell anything.

?

It turned my thumbs up into a ?

Sorry, this old thing doesn’t handle emojis very well. You have to use the html code for it. 😩

Are you familiar with EquityStat for tracking investments? I’m thinking of checking it out. Does anyone have experience with it?

https://equitystat.com/portmgr/pages/home.aspx