Schwab just sent me an e-mail with the subject “The wait is over. The future of investing is here.” That boast means their new automated portfolio advisory platform called Schwab Intelligent Portfolios (SIP) is now opening accounts, meeting their stated date of Q1 2015. Here are some highlights of this service:

Schwab just sent me an e-mail with the subject “The wait is over. The future of investing is here.” That boast means their new automated portfolio advisory platform called Schwab Intelligent Portfolios (SIP) is now opening accounts, meeting their stated date of Q1 2015. Here are some highlights of this service:

- Portfolio asset allocation will be decided using a 12-part questionnaire.

- Portfolio will be constructed using ETFs, mostly from Schwab-managed market-weighted and fundamental-weighted index ETFs.

- No advisory fees, no trading commissions, no account maintenance fees.

- Accounts must maintain a minimum balance of $5,000 to be eligible for automatic rebalancing.

- Tax loss harvesting is available on an opt-in basis for clients with invested assets of $50,000 or more.

- Live support via phone or online chat, 24/7/365

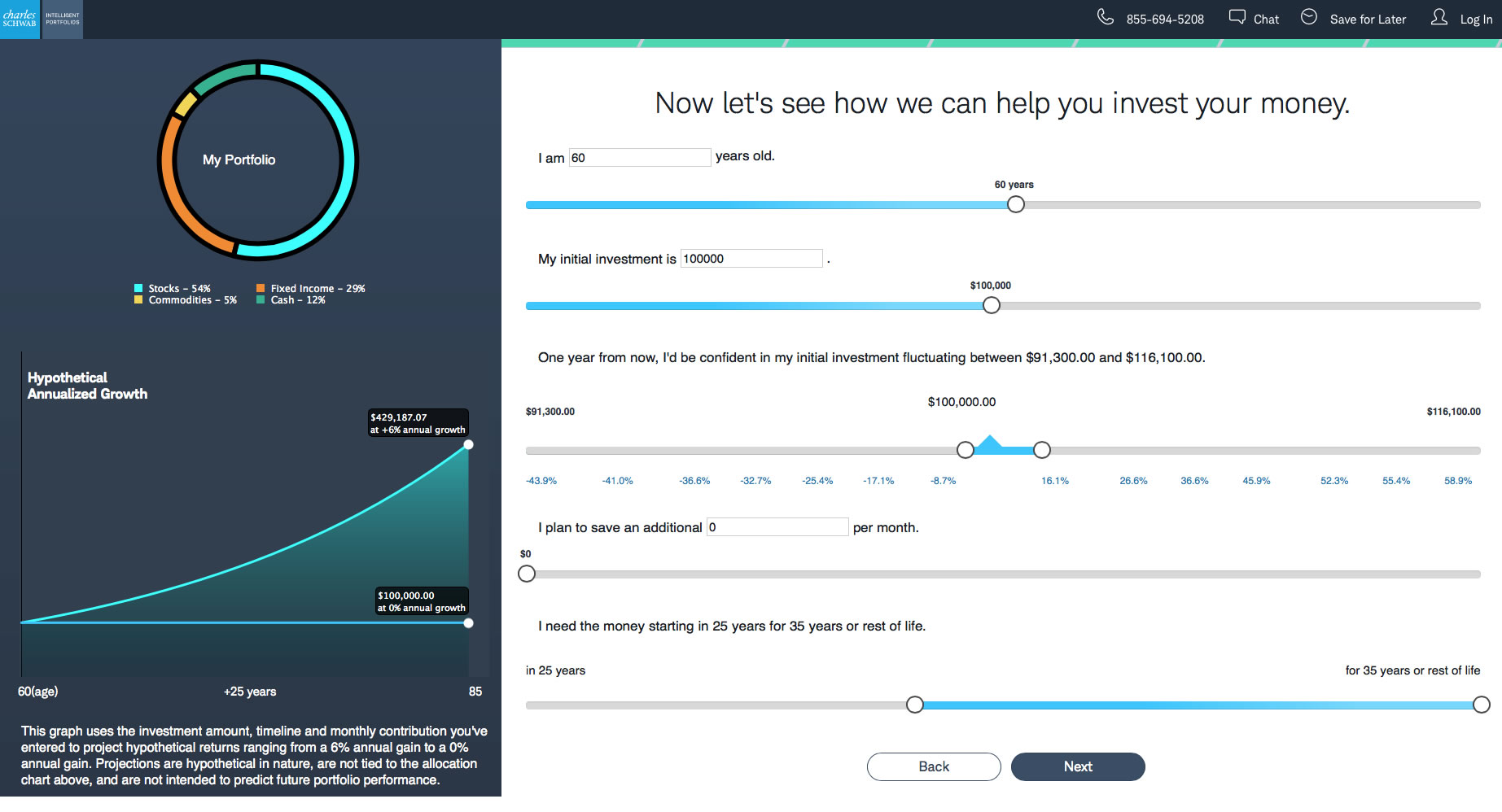

You can do the questionnaire and see your proposed asset allocation without signing up for an account. Here’s a screenshot taken from the questionnaire tool (click to enlarge).

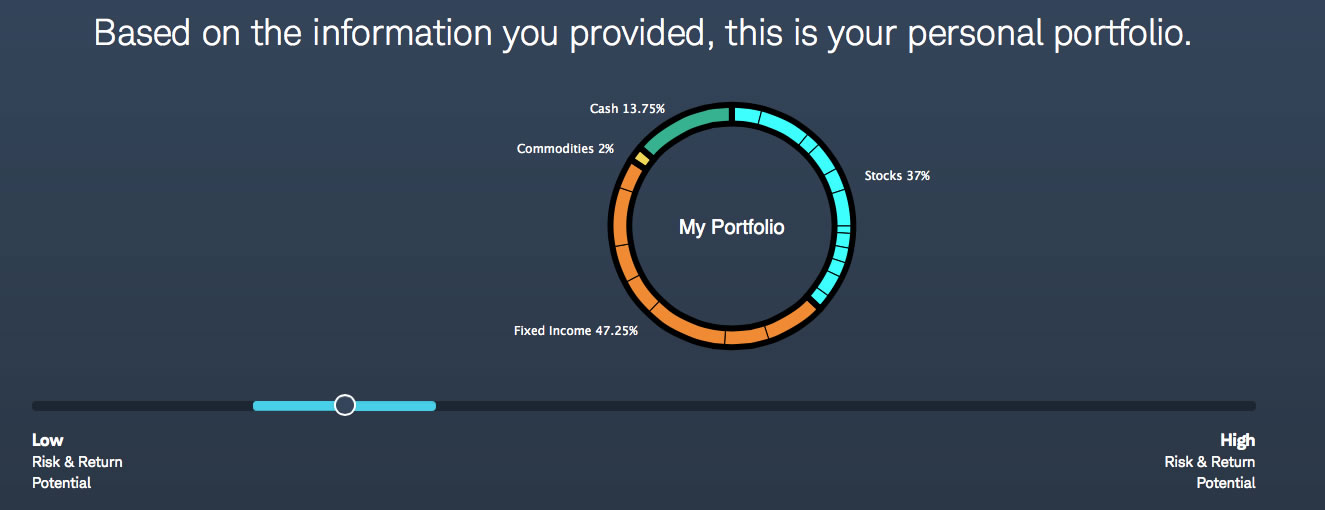

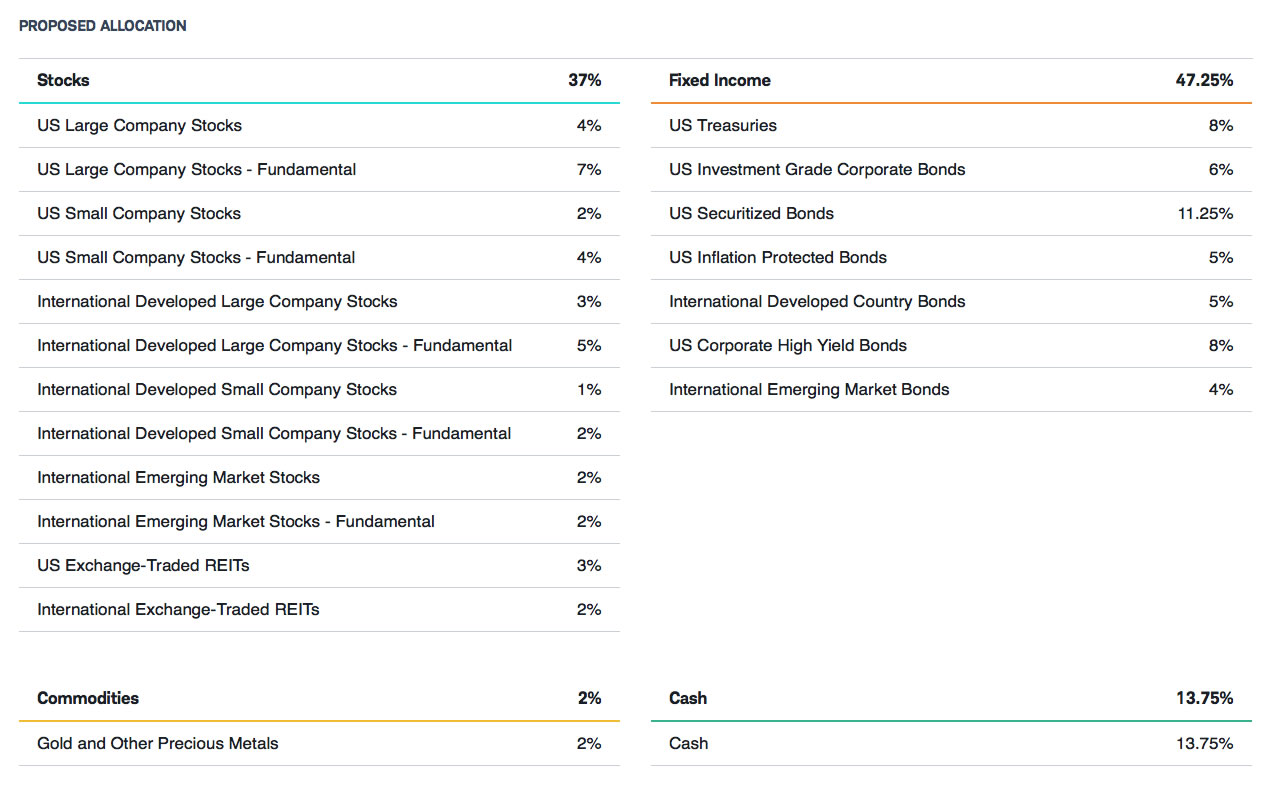

Here are some sample asset allocations that the website provided. I basically just made up two fictional people, so don’t assume these are the only options they give out. First up is “Conservative Cal”, who is 60 years old with plans to retire at 65 and can’t stomach too much volatility. The proposed breakdown for Conservative Cal was 37% stocks, 47% bonds, 2% commodities, and 14% cash. See screenshots below.

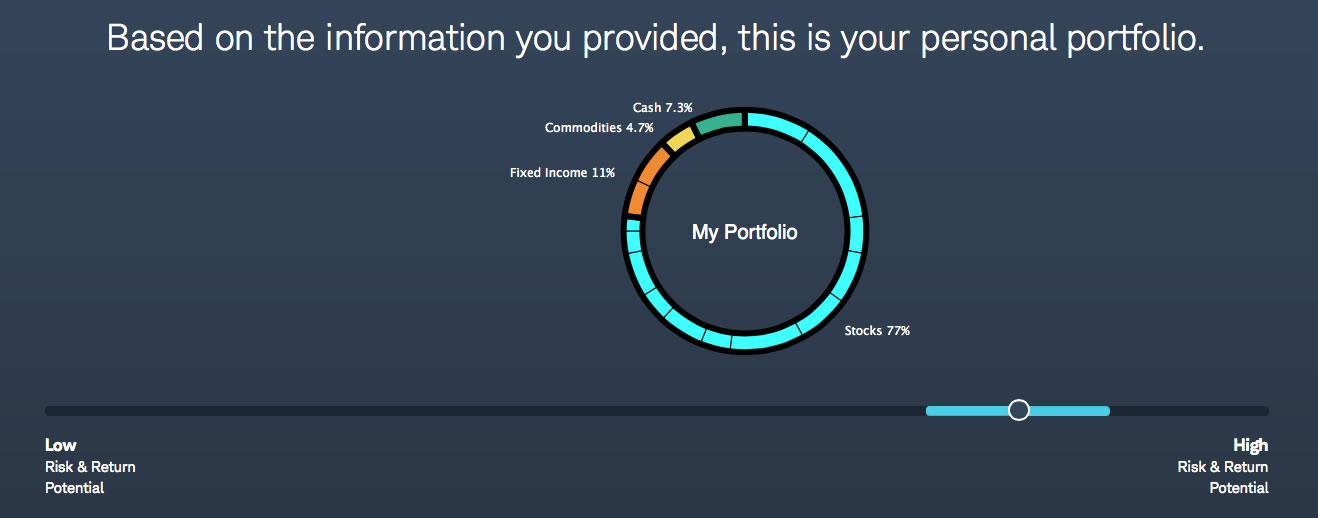

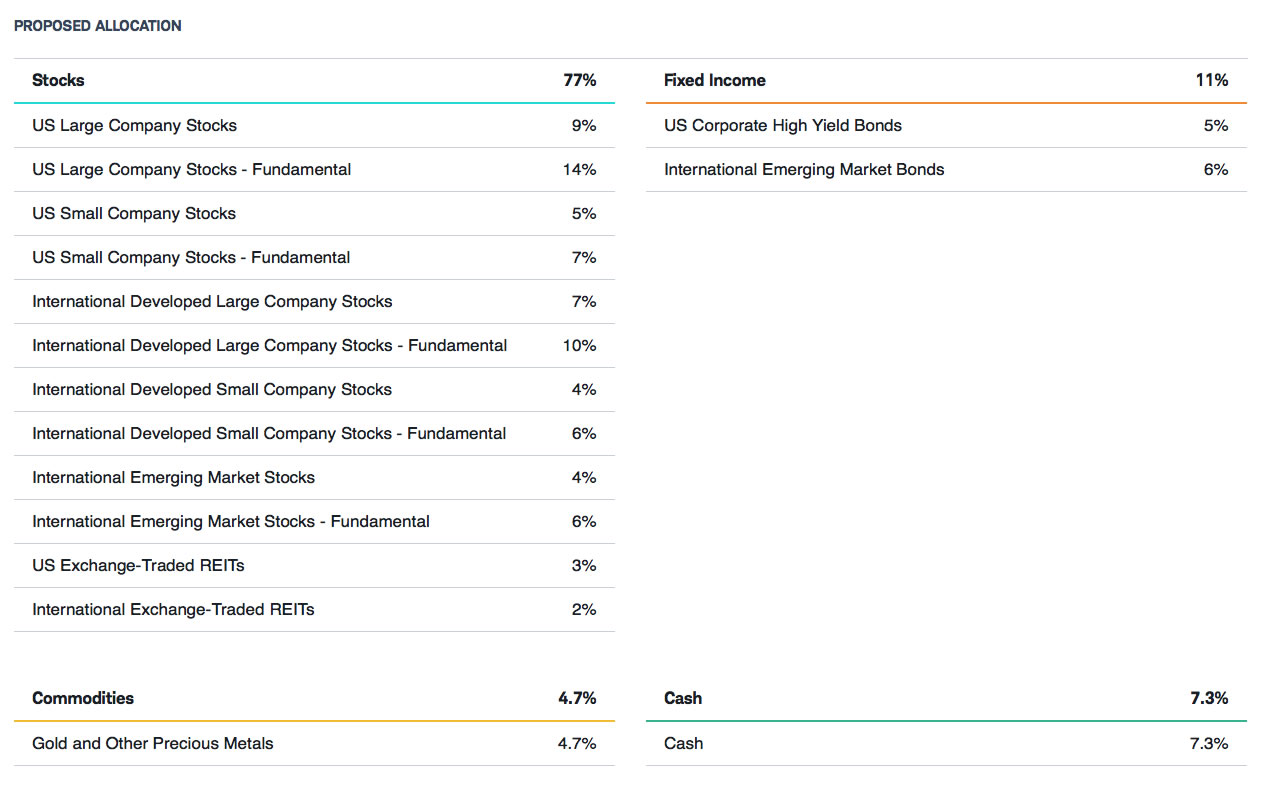

Next up is “Long-term Linda” who is 30 years old with a long time horizon and a healthy appetite for risk. The proposed breakdown for Long-term Linda was 77% stocks, 11% bonds, 5% commodities, and 7% cash. See screenshots below.

It doesn’t actually tell you the exact ETFs you will be investing in unless you continue and fill out an application, but you can bet that most of them will be Schwab market-cap ETFs and Schwab fundamental ETFs. Also keep in mind that there will be “alternate” ETFs for each asset class to be used for tax-loss harvesting.

For example, here’s the likely primary ETF line-up for the stock portion:

US Large = Schwab U.S. Large-Cap ETF (SCHX)

US Large Fundamental = Schwab Fundamental U.S. Large Company Index ETF (FNDX)

US Small = Schwab U.S. Small-Cap ETF (SCHA)

US Small Fundamental = Schwab Fundamental U.S. Small Company Index ETF (FNDA)

International Developed Large = Schwab International Equity ETF (SCHF)

International Developed Large Fundamental = Schwab Fundamental International Large Company Index ETF (FNDF)

International Developed Small = Schwab International Small-Cap Equity ETF (SCHC)

International Developed Small Fundamental = Schwab Fundamental International Small Company Index ETF (FNDC)

International Emerging Markets = Schwab Emerging Markets Equity ETF (SCHE)

International Emerging Markets Fundamental = Schwab Fundamental Emerging Markets Large Company Index ETF (FNDE)

US REITs = Schwab U.S. REIT ETF (SCHH)

International REITs = Vanguard Global ex-US Real Estate ETF (VNQI)

SIP is a direct competitor to Vanguard’s Personal Advisor Services (VPAS) which has a lower average overall expense ratio on their suggested portfolios, but also charges a 0.30% advisory fee. Schwab’s overall average expense ratios on their suggested portfolios are higher, but charges no advisory fee. Schwab then goes as far as to guarantee that the total amount paid to ETF OneSource affiliates and Schwab ETF management fees will not exceed a 0.30% fee.

So Schwab admits that there is some extra profit baked into the program due to their more expensive fundamentally-weighted ETFs and such, but it should still be cheaper than Vanguard after all is said and done. Very interesting.

This is not my full review, as I haven’t decided if I should open a test account (superfluous trades get annoying at tax time). Although I will likely have my criticisms, I am still glad to see it finally roll out because I think Vanguard and others need the competitive pressure to keep improving their own low-cost advised portfolio platforms. A lot of people out there don’t need a full-service human advisor, but could still benefit from having occasional investment guidance available to them at a minimal cost.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Wouldn’t you also consider this service targeting Betterment, Wealthfront, Future Advisor, etc. as competition? It seems to me that with explicitly mentioning automatic tax loss harvesting, Schwab is going after some of these younger services, too.

There seems to be a growing market for the so-called robo advisors, and I think Schwab is trying to keep themselves competitive in this area.

Definitely, but I think that roboadvisor + occasional on-demand reputable human contact will be the eventual winner. Fidelity may not want to reduce it’s huge fees, but I think they will soon because Vanguard just went to 0.30% and Schwab just told everyone they don’t mind disrupting themselves. Wealthfront CEO got feisty because he knows this is a big deal, just didn’t like that Schwab calls it 0% fee when they have other fees baked inside the pie.

Does Fidelity have something similar?

Fidelity doesn’t.

Well, they kind of do with their Portfolio Advisory Services, but is really expensive around 1% of assets for not much better feature set. Fidelity doesn’t have anything positioned as a low-cost robo option.

Fidelity has struck up a relationship with Betterment. But it’s not like a Fido client has access to Betterment on the Fido website. Instead, Fido RIA’s can use the Betterment platform to manage their clients’ portfolios. For the life of me, I can’t understand the reasoning behind this. Why would someone pay a RIA 1%+ just to have them turn around and use a robo service? Human contact isn’t worth that much.

Re: Vanguard’s service – they charge 30 basis points but do have the benefit of a designated human advisor.

How does this compare to Wisebanyan, since they will have only top ranked ETFs (i..e, mostly vanguard) in their portfolio ?

I just opened a WiseBayan account today so that I can compare. I like everything I see and have read about it, but my only fear is how they will make money. I’m expecting some upsells coming in the future as they try to sell additional services. Still, from what I have seen from the setup, I like it more so far than Schwab Int Ports. Just the fact that they allow you to tweak the risk rating after the questions is a nice plus. They rated me at 7.3, and then I moved it manually to “8” to lower my bond exposure. And no cash holdings either which is def a plus!

I like the goal of Wisebanyan, but the questions are where is their profit going to come from once the venture capital gets burned up? Also will they offer human support whenever you want to talk?

I would say this service is very BETA-like at the moment. They don’t say what the aggregate expense ratio is. Xfers between Schwab accounts are not instantaneous as they are with other banks/brokerages I use. There are two different sites used for the service. If you want to see the tickers, you need to login to schwab.com. Other info is available at the intelligent portfolio site. Overall, I’m finding it tough to find certain info, and it is disorienting having to login/look at two different sites. I’m sure it will get better with time. For now, I don’t plan on investing additional funds until things smooth out.

BTW – I know Fidelity has partnered with ether Betterment or Weathfront to offer a similar service. No idea on when that will be or costs.

For Schwab customers, SigFig is also an interesting choice. They charge .25%, and take trading authority over your account. You work with them to create an allocation that they then rebalance to and keep in line. The first $10K is managed free.

It’s essentially Wealthfront’s service without needing to move your money from Schwab…

The question is, is it worth 25 bps more than Schwab’s service just to customize your allocation and presumably lower the cash allocation?

The big downside is they keep at least 7% in cash. When I calculated it the potential loss of not investing that 7% was more than betterment’s fees. I already have some cash in Ally making almost 1%, I don’t want an additional 7% kept by Schwab only making .08%.

I found a response on Reddit which addresses this point. The problem is, no investment advisor’s cash fund earns as much as a bank because they are in Money Markets which pay much less.

“A cash position with an investment firm is going to be in a money market fund and that fund is going to have next to no interest paid in today’s market because that’s how it has to be. Money markets aren’t like a bank account where they can pay whatever rate they deem business acceptable. They’ve got to pay out what the underlying holdings pay minus expenses. Since by definition a money market must invest in securities with less than a 270 day maturity they simply can’t pay better interest. “

I spent a LOT of time researching this yesterday, so happy to answer questions.

The actual list of ETFs used and their alternatives (for TLH -Tax Loss Harvesting) can be found at the end of this white paper.

https://intelligent.schwab.com/public/intelligent/insights/whitepapers/tax-loss-harvesting-rebalancing.html

There are two primary complaints with Schwab Intelligent Portfolios.

One is that they hold way more cash than anyone else in their model portfolios. They will hold a minimum of 6% cash and up to 30% in conservative portfolios. Schwab actually makes a lot of money from this over allocation to cash as Adam Nash, the head of Wealthfront points out in this article here:

http://www.investmentnews.com/article/20150309/FREE/150309913/wealthfront-ceo-accuses-schwab-of-deceiving-investors-with-free-new

The other complaint is that they use very expensive Fundamental Based Indexes in their allocations. The large-cap fundamental index charges 0.32% compared to the cap-weighted index which charges only 0.4%.

Schwab uses both funds in their allocations, but uses more of the more expensive fund in all cases.

Both of these are legitimate concerns and keep Schwab from being ideal. That said, Schwab may still be the best game in town in the Robo-Advisor space.

It’s most expensive allocation has an “all-in” cost even with all the fundamental indexes of 0.26%. What’s more, Schwab gives you the ability to remove up to 3 ETFs from your allocation.

The most aggressive allocation (it still has 6% cash) has 6% cash, 46% US, 32% International, 10% Emerging and 6% REITs. By removing the 3 most expensive ETFs, I calculate the total operating expenses of the underlying funds to be a miniscule 0.125%

12.5 bps (basis points) is half the cost of what Wealthfront is charging even before adding on fund expenses! It’s also not a bad allocation in my opinion… Would love to tweak it though.

So yes, a very interesting option that is free so long as you don’t mind having a chunk of cash in your long term portfolio allocation. You can read Schwab’s response to Adam Nash’s opinion letter here:

http://www.aboutschwab.com/press/statements/response-to-blog-by-wealthfront-ceo-adam-nash

Happy to answer any questions. I spent all day on the phone with them yesterday…

Yes, the cash % is an issue. I tried answering the questions as “most aggressively” as I could, and I still got stuck with 8.3% cash. I tried redoing the questions a few times, but got closer to 10% cash. And there is no way to manually tweak the aggressiveness factor. It’s all based on the 12 questions.

Yes you can remove up to 3 ETFs, but I was told the money doesn’t flow into the other remaining funds. Instead, they select “replacement ETFs”, which could cost as much or more than the funds you replace.

Yup, I just found this out when I went to sign up today. The original Rep had told me incorrectly. If you remove a fundamental ETF it gets replaced not with the cap-weighted ETF, but with a more expensive fundamental ETF.

Suffice to say, I wasn’t pleased the Schwab rep led me wrong. Still incredibly cheap at .23 bps all in for my allocation, but I don’t like being forced into more expensive funds.

Yeah, IMO the reps are not all up to speed yet on this product. I have rec’d some conflicting answers also. I hope they work out the kinds quickly, as right now I’m a bit disappointed with the overall product.

It’s a nice interactive little system. The problem is in the end you have to deal with Charles Schwab which has just been one of the worst companies to do business with. They are poor with communication, excessively slow processing transactions and uninvolved, uninterested customer service. I have to still use them for a previous employer’s 401k. But I’m back with Fidelity and Vanguard and the difference is unbelievable.

Obviously YMMV, but I’ve overall been happy with Schwab and don’t share your concerns re: customer service. I do think, however, their security profile is rather weak.

The fact that their password policy is letters and numbers, only, between 6 and 8 characters is laughable in the days of identity theft, spear phishing, APT, etc. They do offer the option of two-factor authentication, but they don’t even interoperate with many of the industry-standard solutions (TOTP, text messages, voice response, etc.), requiring you to acquire a purpose-built piece of hardware that you must keep track of. It is, frankly, disappointing that their security policies appear to have been developed a decade (or more) ago, and no attempts have been made to keep up with the overall industry.

Read this article from Wealthfront CEO about Schwab: buff.ly/1MmGWRW

I am personally a fan of Hedgeable. They wrote a couple great articles dissecting the new Schwab Intelligent Portfolios.

Here is the link: bit.ly/1AaSh1v

I spoke with the Hedgeable guys. A bit skeptical of their portfolio model which is essentially based on market timing. They can basically go from 0 cash to 100% cash depending on what their models tell them.

They insist they aren’t market “timing” but they are market “pricing”… They say they aren’t making predictions about the future, but rather basing allocations on current prices.

Feels an awful lot like market timing… Will be interesting to see what happens to them when their models are on the wrong side of a crash or boom. Could be better results, could be a lot worse. Either way, you’re out the .5% management fee. Oh, and they have an optional Bitcoin allocation for the truly adventurous.

Who uses these services? I just throw my money into a Target Date Fund and focus on making more money.

Vanguard 2045 costs 0.18%. The Schwab intelligent portfolios run anywhere from .012% to .26%.

Schwab just has a different asset allocation mix than Vanguard. They are pretty similar at the end of the day. There’s a bit more variety in setting the level of risk your comfortable with at Schwab. Vanguard really only has one allocation for everyone.

Maury – I am really skeptical of this .012%-.26%. I looked at the largest (% wise) 8-10 holdings in the portfolio Schwab put me in. Other than 1-2 of them, the exp ratios were .32-.48%. And that doesn’t include the impact having 8.3% cash either.

As I mentioned in my earlier post, they don’t provide what your aggregate exp ratio is, but I highly suspect mine is > .26%. If I had to guess, it would be closer to .35-.45%, but I am unwilling to do the math and figure it out on my own, since they put me into close to 20 different ETFs.

Clock – You are correct.

I was told by a Schwab rep that you could remove 3 of the Fundamental based ETFs and they would be replaced by their cheaper cap-weighted counterparts. (e.g. replacing a .32% fund with a 04% fund.) When I went to sign up today, I discovered that wasn’t true. They would be replaced by slightly MORE expensive fundamental ETFs! (It’s a shame as it was an incredibly impressive spreadsheet I had made to figure that out! Ha.)

That said, Schwab lists the average ETF expenses on their website for various portfolios.

Conservative = 0.18%

Moderate = 0.23%

Aggressive = 0.26%

Still dirt cheap, but there is no getting out of the expensive fundamental ETFs. Also, there is the long term cash drag.

Ok, I took the time to create a spread sheet and calc my overall exp. If my math is correct, I got .27%. So a tad higher than what they claim for “Aggressive”. My cash is also higher than they said. When I did the questions, they said my cash allocation would be 8.2 or 8.3%. Looking at my account, they have me in 8.74% cash.

I update my spreadsheet, and put a exp ratio of .95% for cash holding. Not sure that is the best way to measure, but I figured I get .99% interest in my MMA account, and I figure Schwab will prob pay about .05%, so I took the difference.

When factoring the cash in, then my portfolios exp ratio goes from .27% to .33%. So overall, this offering is probably priced similarly to Wealthfront, Betterment, etc…

Interesting way go about calculating the “real” expense of this fund. I like it. I can see no flaws with assuming a .95% fee for managing cash although it hurts my head to see all these funds and the one with the highest expense ratio is cash! Ha!

I ran the same calculations for the most aggressive fund they have. The “All-in” expense ratio was .23%, and when you add the expense ratio for cash it jumps to .29%

Right in line with Betterment’s all in cost, but a tad cheaper than Wealthfront’s.

Obviously, getting the asset allocation right matters a lot more in the long term than 10 bps here or there. Not sure if I like being in as much cash as Schwab is suggesting for the long term.

The trick is, how do you get the most aggressive portfolio? I answered the questions a aggressive as possible, trying to keep my cash allocation down. I still ended up with 8.7- 9.4% cash. And unlike Wisebayan, they don’t let you manually tweak your risk score and the end of the question.

I’m going to make the prediction that Schwab will reduce the cash allocation in their proposed asset allocations in response to all the criticism. Let’s say within a year from today.

I agree with you. Any article/blog you read on this mentions the cash issue. That along with the “fundamental” ETFs they favor, it is hard to figure out what you are really paying for this account compared to their competitors.

The Hedgeable guy probably has the best written analysis of the cash thing. (While I’m skeptical of Hedgeable’s market timing philosophy, he has a great analysis of Schwab’s new offering.)

https://www.hedgeable.com/blog/2015/02/schwab-intelligent-portfolios-review/

From their disclosures:

“The Sweep Program is a feature of the Program that clients cannot eliminate. In most of the investing strategies, the percentage of the Sweep Allocation is higher than the cash allocation would be in a similar strategy in a managed account program … This is because, as described below under ‘Fees,’ clients do not pay a Program fee.”

Just wondering, if interest rates were not at all time lows, the cash allocation may not be an issue.

If, when and how much interest rates rise in the future, will be the true test of it’s performance and cost of management.

In the context of a retirement portfolio, cash should be a T-bill and thus just a really short-term bond. The problem is the appearance of bias. I like Mebane Faber’s take:

“I don’t mind cash as a strategic allocation, but I do agree with Wealthfront that Schwab earning revenues from the money market sweep accounts could bias their decision to include cash. There is just no need to do this – they could have used an ultra short term gov bond ETF and still made some money off it. However, the moral outrage from Wealthfront comparing Schwab to Merrill is a little ridiculous considering Wealthfront used to charge 1.25% for access to “geniuses”.

http://mebfaber.com/2015/03/10/what-a-great-time-to-be-an-investor/

Wow, that Faber article was great.

He’s absolutely right. On the cash, Schwab probably makes .8% at most lending that out. If they had put this in short term government bonds they would have earned .8% on their own fund and had zero outrage.

Now I’m curious about Faber’s crazy 0% management fee Global Asset Allocation ETF (GAA). Intriguing…

Another good take from Tadas Viskanta:

“A disciplined portfolio strategy, even if sub-optimal, is better than an ad hoc portfolio strategy. For DIY investors cash represents a bad habit they need to kick. For investors shopping among the many robo-advisor solutions it simply represents a feature they need to better understand.”

http://abnormalreturns.com/2015/03/11/great-cash-debate/

Has anyone looked at basically recreating a Schwab, Betterment or Wealthfront allocation at MotifInvesting.com?

You can create a portfolio with up to 30 ETFs in any % configuration you want and buy them all for $9.95.

You don’t get tax loss harvesting, but I’m mainly looking at retirement accounts where that doesn’t matter.

You can rebalance for just one $9.95 cost whenever you feel like it. (Say 4x a year for a total of $40.)

On a $100K account, that is a rebalancing fee of .04% per year…

Heck, this might be cheaper than Schwab at the end of the day… Any drawbacks to this approach?

And tell me just how this is better than say a Vanguard Target date fund?

At this point in time, the only thing I’ve actually recommended to actual family members is a Vanguard Target date fund. BUT, my opinion is that people want to know there is a human somewhere they can call with questions. Since that person won’t be “Bob from Church”, they’ll want a reputable brand name. That is why I think a robo-portfolio plus a human phone support is the future and agree with the folks that say either Vanguard, Fidelity, or Schwab will “win” this game. Add in some competition to drive costs lower, and the future doesn’t look that bad! 🙂

Jimbo

Vanguard Target Date funds are always a great choice. That said it is a one size fits all solution.

For example, I’d like a dedicated allocation to REITs. I’ve read Swensen and see the value in that. I also see the value of a small and value tilt which Vanguard doesn’t have. I actually think Jonathan has a great portfolio allocation, with the exception that he has to manually rebalance.

Is it worth the hassle to tweak your own portfolio. For most people no, it probably isn’t. Also behavior factors creep in.

Personally, I want to set up my asset allocation the way that “I” want it, and just have the provider rebalance and reallocate new funds. Alas to get that, you are forced to choose one of their predetermined portfolios and pay an extra fee. The portfolios are decent and the fees aren’t bad, but they could be better in my opinion.

The other thing I forgot to mention, is I have doubts about their ETF selection process. They claim to use bid/ask spread and fund size in part of the selection process, but I noticed many of the funds they put me in are smaller than 100mil. I doubt a $40mil fund has the small bid/ask they claim to require.

Also of note 11of17 funds they put me in are Schwab ETFs, but I think we all kind of expected that. I think their selection criteria must heavily favor there own funds over others.

Jonathan, do you still have the money invested with WiseBanyan ?

Some quick questions:

1) Am I correct in assuming that you can use this feature for an IRA Account? So any tax implications would be minimized.

2) I have a Schwab One and 2 IRA accounts. Do you direct the robo-advisor to the specific account you want managed or does it have to have access (and manage) to all your accounts at Schwab? If you already have securities in the account(s), does the robo-advisor sell them for you and convert the proceeds to the new portfolio or do you need to convert the account into cash beforehand?

Thanks.

You have to create a new account for the Intelligent portfolio service.

So when you need to go through a 15-page Disclosure Brochure (https://www.schwab.com/public/file/SIP-SCHWAB-WEALTH-ADVISORY-DISCLOSURE-BROCHURE) to understand what “FREE” means, you might question why such a marketing effort to not be more transparent. It does not inherently mean that the service does not have value, but it does inherently outline the conflicts of interest and help you understand that NOTHING is FREE.

You might also consider that most, but not all, of Schwab’s ETFs have anemic volume. However, not one of them even carriers an average daily volume (ADV) of 1MM shares. Additionally, investors might wish to consider avg spread, tracking error, premium/discount, as it relates to liquidity, Certainly, don’t forget about expense ratios. While 14 of Schwab’s 21 ETF carry expense ration of 4 to 14 bps, the other seven range from 19-48 bps.

Moral of the story, know you who are dealing with and if they are dealing straight with you. As always, do you homework and work with someone you trust. In the end, when you have a question about how this all works do you want to speak to a call center or the portfolio manager. Just something else to think about.

Schwab has quietly completely overhauled the hypothetical ‘conservative’ portfolio.

instead of all the fundamental and cap indexes, it is simply a domestic and foreign dividend ETF, a tiny sliver of domestic and international REIT’s and some MLP’s(!). They’ve also completley changed the bond allocation to include preferred stocks and floating bank loans. The more aggressive portfolios don’t seem to have been effected.

https://intelligent.schwab.com/public/intelligent/about-intelligent-portfolio

Is there a fixed setup fee or is the example of 14 ETFs going to gen 14×4.95=$69.30 set up fees and then $69.30 per year for rebalancing all of these…