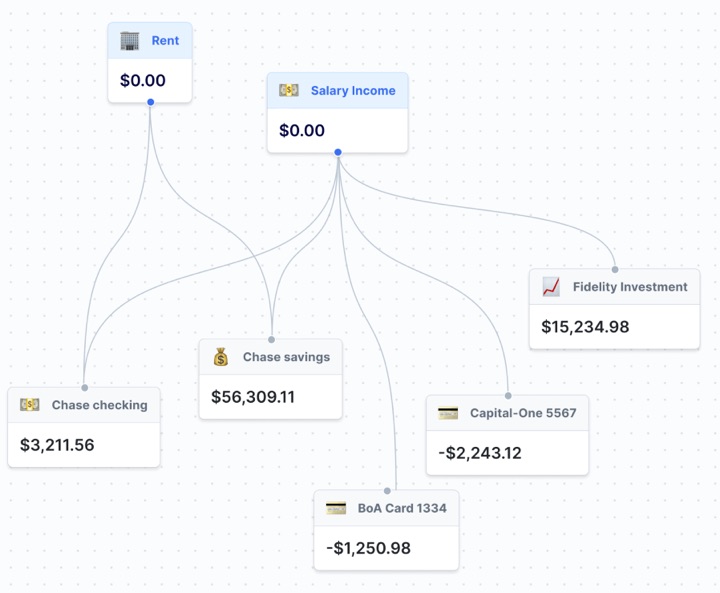

Here’s a new idea that I haven’t seen yet: GetSequence.io lets you apply a flowchart system with simple If/Then conditional statements to your cashflow. Imagine a visual map connecting your financial accounts and being able to manage the flow of money between them using preset rules. They call it a “financial router”.

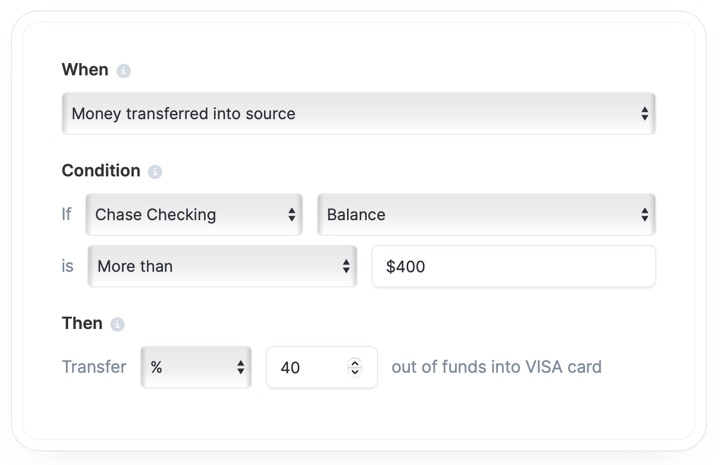

For example, you would first have your paycheck routed to Sequence. Then a rule says “If the balance at Chase Checking is at least $5,000 (perhaps enough to pay your monthly bills), then transfer 50% to savings and 50% to your Fidelity investment account”. But then add “If the savings already has $5,000 in it (maxed out your emergency fund), then transfer all of the funds to Fidelity account”. Or you could always have 10% taken off the top into your Fidelity account, no matter what.

This type of things sounds neat in theory, but I am concerned that reality is too messy to have all these fixed rules. It also seems to rely heavily on accurate aggregation of third-party providers like brokerage and credit card accounts. Some people really like having several “envelopes” or “buckets” for budgeting and savings, so perhaps this would work for them.

Unfortunately, this is all a non-starter for me because Sequence is a fintech. Their banking services are provided by Thread Bank, Member FDIC. But as the FDIC and every other US regulator has told us after ongoing Fintech/Synapse/Evolve debacle, if somehow Sequence or Thread Bank gets confused while routing all your money around and doesn’t keep proper records of all the balances on their ledger, then the consumer is out of luck. With no protection if this start-up fails, I am unwilling to try Sequence myself. I have no other affiliation with them, either. Anyone else out there try this new tool?

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Jonathan, I agree with you the unwilling to risk it with the fintech. The idea is just trying to automate your cash flow. I have my finances set up like a group of switches rather than a router. Direct deposit to multiple accounts (Checking – Investment, Checking – Discretionary, Checking – Fixed costs, & Savings). The Investment buys investments automatically to bonds and stocks, Discretionary pays a cash back credit card (manually as it helps me gauge my spending), Fixed cost are automatically sent to a credit card & payments that don’t accept credit cards because they are always the same every month, Savings is built up for emergencies every month. The same result more less can be achieved with a little planning.

I feel like I had this idea (a long time) before but discarded it because (1) it’s too easy for things to go haywire in practice and (2) if you care enough about your finances to be optimizing cashflow, you will probably have to do it manually a large part of the time anyway.

For (1), I think it’s too easy to overlook a corner case in your rules. E.g. your rules assume that your paycheck will always top off your emergency fund in your checking account, but then one month you have a much larger expense, or your take-home pay from your paycheck is dramatically reduced because you are contributing a bunch of extra money to your 401(k) to try to max it by the end of the year. If you have rental income, maybe your tenants pay super late (or not at all) one month or a check bounces. Do your rules still happily execute and maybe overdraw your accounts? Also, if there are errors with the automation that are maybe not even your fault, do you think your financial institutions that actually handle your money will care? I don’t think they will.

For (2), if you’re taking advantage of a bunch of financial promotions (of the kind often linked on this web site), e.g. deposit bonuses for opening and substantially funding new savings accounts, or 0% interest on a new credit card for ~12 months ideally with the lump sum of the balance paid off before you start to accrue interest, then you will have to be manually monitoring your finances anyway. The one-off interventions required for these promotions can easily overwhelm simple automations that assume more stability.

All that said, automation is cool! I just don’t think the juice is worth the squeeze in this particular case.

They have a monthly fee, too. I figured they would make money from cash sitting in the account. It’s a fantastic concept that I would use, but not from a start-up with a monthly fee and no insurance on my money. I’m ok with making changes once every two weeks if needed.

I’ve been using Sequence for over a year now, and it’s really helped simplify my overall financial picture. I use it to route money to my various financial accounts with the following goals in mind (not too different from the example you used):

– Top off my checking account to a certain amount.

– Pay down my credit cards and debts.

– Save and invest the rest, dividing the remaining funds across my savings, brokerage account, and Coinbase account (from where I manually route the funds to a private credit investment platform … so there’s still at least one click involved in all of this ?).

I receive inflows from a variety of sources: my W2 job, monthly or quarterly dividends from investment platforms like Fundrise and Yieldstreet, and P2P payments when I split bills with friends. Having all these inflows run through a single, cohesive system of rules has been a huge time saver for me.

Additionally, the platform is fairly versatile: I’ve seen others in Sequence’s Discord community using it for budgeting, managing business finances, and more.

I understand your hesitation around adopting any fintech service, especially in light of the recent Synapse failure. I would be lying if I said I wasn’t hesitant to adopt Sequence a year ago. In fact, it’s natural to be cautious with anything built on top of another system, which these days, is most things. We just saw how a faulty CrowdStrike update a couple weeks ago caused major issues for companies relying on Windows. In a similar fashion, AWS outages tend to have global impacts. In the end, I think it really just boils down down to a risk and reward analysis: how much are you putting at risk in the event of a failure, and how much do you gain from using the platform? These are obviously pretty personal questions. In my case, I save hours every month and easily get more value from the platform than what I pay for it. The risk is minimal in my case because, based on how I have things set up, money moves through the platform within a matter of days (you can even set it up so that rules automatically execute during an inflow and schedule external transfers immediately).