Harry Markowitz, who received the 1990 Nobel Prize in Economics for his contributions in creating modern portfolio theory, passed away recently. He introduced the use of mathematical methods to illustrate the power of diversification and how you can combine multiple different components into a portfolio that can achieve the highest expected return while taking on the minimum amount of risk. This NY Times obituary outlines his long list of achievements.

These days, anyone can run many backtests to optimize for a historically optimal portfolio using a number of different asset classes (as of today, it will be different in 5 or 10 years). However, if you listen to many of his interviews, Markowitz doesn’t necessarily think the average investor needs optimize relentlessly. Here are some useful quotes that don’t require any advanced math.

From his landmark 1959 book Portfolio Selection: Efficient Diversification of Investments:

A good portfolio is more than a long list of good stocks and bonds. It is a balanced whole, providing the investor with protections and opportunities with respect to a wide range of contingencies.

How did Harry Markowitz actually run his own personal portfolio? From Jonathan Zweig’s NYT article about emotions and investing:

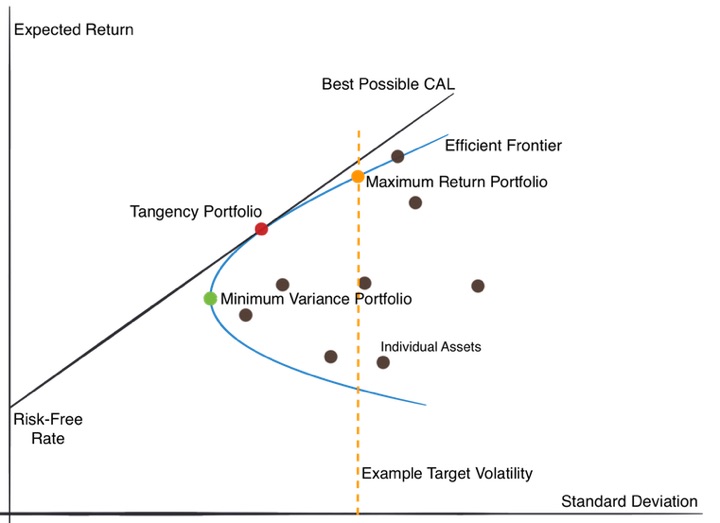

Mr. Markowitz was then working at the RAND Corporation and trying to figure out how to allocate his retirement account. He knew what he should do: “I should have computed the historical co-variances of the asset classes and drawn an efficient frontier.” (That’s efficient-market talk for draining as much risk as possible out of his portfolio.)

But, he said, “I visualized my grief if the stock market went way up and I wasn’t in it — or if it went way down and I was completely in it. So I split my contributions 50/50 between stocks and bonds.” As Mr. Zweig notes dryly, Mr. Markowitz had proved “incapable of applying” his breakthrough theory to his own money. Economists in his day believed powerfully in the concept of “economic man”— the theory that people always acted in their own best self-interest. Yet Mr. Markowitz, famous economist though he was, was clearly not an example of economic man.

From a Chicago Tribune interview by Gail MarksJarvis:

Early in his career, he did not take the risks some investment advisers suggest for young investors to maximize returns. Rather, he saved regularly and put half his money into stocks and half into bonds to grow while controlling risks. When he thought he had accumulated too much in either category, he stopped putting money there for a while and directed savings to the neglected group. […]

“I never sold anything,” he said. If stocks were increasing in value, he would let that portion grow for a while, but eventually he would stop stock purchases and beef up the bonds. The idea: The bonds would insulate him from the downturns that crush stocks from time to time without clear warning. […]

“Say you were 65, and invested $1 million, with 60 percent in stocks and 40 percent in bonds,” he said. “It became $800,000 [during the financial crisis], and you are not happy, but you lived to invest another day.”

From this Business Insider article via Bogleheads forum post (emphasis mine):

In an interview with Personal Capital, Markowitz was asked, “What are the top pieces of advice you give people about money?”

“I only have one piece of advice: Diversify,” he replied. “And if I had to offer a second piece of advice, it would be: Remember that the future will not necessarily be like the past. Therefore we should diversify.“

From ThinkAdvisor:

“Perhaps the most important job of a financial advisor is to get their clients in the right place on the efficient frontier in their portfolios,” he told me. “But their No. 2 job, a very close second, is to create portfolios that their clients are comfortable with. Advisors can create the best portfolios in the world, but they won’t really matter if the clients don’t stay in them. “

Thank you, Mr. Markowitz, for your contributions to economics, behavioral finance, and investing. Thanks also for the simple, actionable lessons that don’t require a degree in mathematics or economics: keep saving regularly, maintain a diversified portfolio of both stocks and bonds, rebalance when it gets off, and stick with it for a long time (don’t panic sell).

Image credit: Quantpedia

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Speak Your Mind