Multiple sources are suggesting that increasing student loan debt levels will have a significant impact on future housing prices because people will delay their home purchases (or put them off entirely). Although that seems like a reasonable assumption, I haven’t actually seen any hard data on it.

In a recent Vanguard research paper titled No bubble to burst: U.S. student debt is not housing [pdf], they took data from the Federal Reserve’s 2010 Survey of Consumer Finances and U.S. Census Bureau and found that:

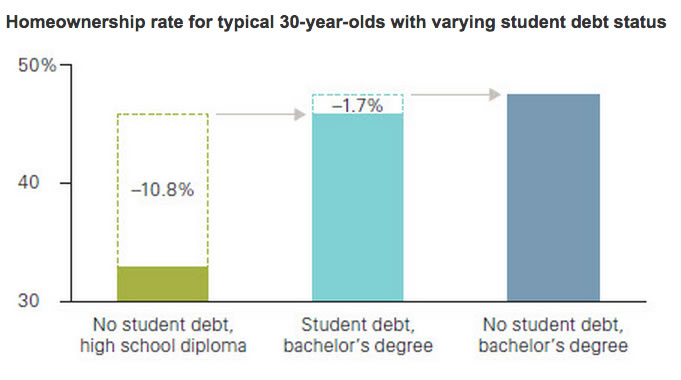

Although financing a bachelor’s degree with student debt decreases the likelihood of a typical 30-year-old college graduate purchasing a home by –1.7%, obtaining that degree also increases the likelihood of purchasing a home by 10.8%, relative to not attending college at all.

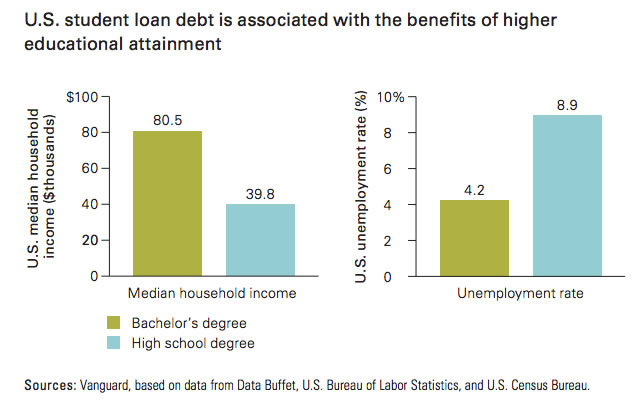

In the end, the conclusion seems to still be consistent with other findings. Getting that college degree is still “worth it” financially, even with the accompanying debt, at least on average. Your income is higher, you’re less likely to be unemployed, and you are more likely to own a home.

I suppose the primary thing to avoid is to not be above average on the debt. If you have to take on $120,000+ of debt just to get a 4-year degree, you’re probably going to the wrong school anyway. If the school really wanted you, they’d offer you a better aid package with grants and/or tuition waivers.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

The question is no longer, “Should I get a college degree?” It’s “Should I get a college degree when I don’t know what I want to do when I graduate?” And the answer is no.

I think most kids (and I do consider them kids) at age 17-18 don’t know exactly what they want to do when they enter college. I had a general idea but didn’t know enough about career fields to realize my current job even existed. Going through college is part of the process of deciding what kind of work you are interested in and good at. And typically it takes a few job changes to find out exactly what you want to do (even within your field) and maneuver yourself into that job.

Agreed. Few 18 year-olds (or even 22 year-olds) *know* what they want to do, but college – ON AVERAGE – still pays off from a job/salary standpoint from graduation through retirement, based on the best information available.

As Andy says, there are career choices emerging all the time and if one approaches college correctly, they don’t view it as simply job or career training but rather life-improving, equipping them with certain skills but more importantly a bigger picture of the world, opportunities and experiences to enhance job/career/life and lead a more fulfilling life. It can be a growth process, typically in a safe environment to get deep into an interest, try some new interests and prepare for both career and life.

I’d be interested in seeing a graph of homeownership versus student debt load at age 30. I suspect we’ll see a precipitous dropoff in ownership rates for those with high debt loads. Also, though these results aren’t showing huge declines, I suspect since it is from 2010 that it’s not showing out all the circumstances millennials are facing (including the housing crash in ’07 as well as rising student loan debts), things that will be really be reflected in data ~5ish years from now.

What do you consider “high debt loads”? Yeah I’m sure people with a bachelors and > $100k in debt are much less likely to own homes. But keep in mind that very few people are in such a situation. Less than 1% of people graduate undergrad with that high of debt.

For most people student debt is really not going to have much impact on home ownership. No more than car ownership.

The last graph has got to be wrong. You’re telling me that a bachelor degree is worth $40,700 per year in increased household income? I don’t believe that.

If that’s the average of all households based on only those two conditions (bachelor’s degree vs high school degree), I would believe it. Toward the mid career, I imagine the ceiling of earning power is much much higher with a bachelor’s or above degree…

I believe that the ceiling is much higher, but I don’t believe that the median is double.

Its median HOUSEHOLD income and by that measure the number is correct.

Here’s a census table :

https://www.census.gov/compendia/statab/2012/tables/12s0692.pdf

$39k median for high school grads vs $75k for bachelors in 2009. So $40k vs $80k today sounds right.

INdividual earnings differ from household. INdividuals working full time with high school make $666 a week versus $1176 for bachelors. Thats about $35k vs $61k.

Yeah, I get the difference between individual and household income, Jim. Thanks. So if we’re to believe your numbers, it sounds like there’s a lot more at play here than just the difference in education level. It seems like the folks with the degrees have a higher probability of having other income producing household members than the folks without the degrees.

And, this analysis is somewhat vacuous anyway, because there are likely other differences between the two groups than just their education level. The proper way to analyze the true value of the degree is to compare two groups of similarly skilled and motivated people: one group who graduates college and the other group who doesn’t go. Then, compare the incomes of those two groups. We can’t just assign all the excess household income of people who are college graduates to having the degree itself, since it’s likely that the people who graduated are more intelligent, driven, etc. These are skills that would be rewarding financially regardless of whether or not the individuals have a college degree.

Just think about it – if the median household is benefiting by $40,700 per year by having a bachelor degree, why are we getting so hot and bothered about going $100,000 into debt to get one? That is astonishing return on investment; It would pay for itself in less than 2½ years. And even that $100,000 in debt figure is the 99th percentile of all debt loads according to an above comment.

If the median household income numbers are correct, getting a bachelor degree is profitable up to a maximum debt of about $517,000, assuming you work until age 65, pay 8% interest on the student debt, and can earn 8% on savings/investments.

Which is precisely why tuition can and mostly likely will, barring some public policy intervention, continue to increase at a rate well above the rate of price inflation.

There are more often than not two earners in each household, and statistics show you are more likely to marry someone at your own education level. That means that there are 2 bachelors degree to support that increased $40,000 income, or $20,000 per bachelor degree. Still a good return on your initial investment, if you think you will be at the median or greater.

Very interesting graphs and information. I have a large student debt load, but don’t want a house either. I’m glad because I cannot afford it! I think many people will buy houses and have kids later because of student loans. We are already seeing this trend.

There is a positive skew on all the data that says college grads make more $. The kids who typically earn a 4 year degree grew up in the middle-upperclass zip codes and likely had bountiful resources at their disposal in early adulthood. In short, the degree isn’t the sole factor, or even foremost factor that provided them the higher income. It was pretty much the luck of where they were born.

Sure there are exceptions…but this is how it works for the most part. So, the question is…was it better to stake that money for 4 year college….or an apprenticeship, or a franchising fee, or business start up capital or the like?

I graduated 5 years ago and the problem isn’t student loan debt, but it’s a combination of student loan debt along with receiving meaningless degrees. If students pursue degrees that are worth something in the real world, than paying off the loans shouldn’t be a problem.