As part of its “Portfolio Basics” series, Morningstar has an educational article on taxable bonds, including corporate bonds, US government bonds, and foreign government bonds, along with their different credit grades and maturity lengths.

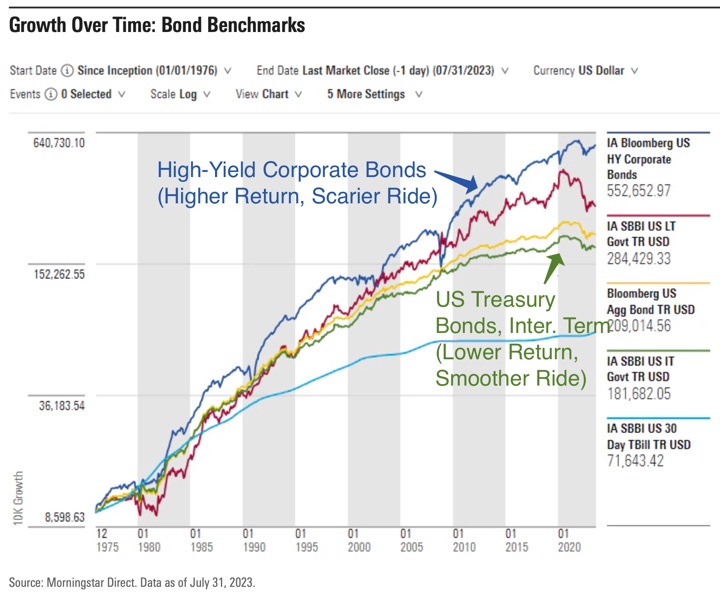

Over the last 20 years, things have played out pretty much as the traditional theory would have predicted. The higher the “risk”, the higher the return. High-yield “junk”-rated corporate bonds have had the highest return, but also the bumpiest ride due to their higher credit risk and higher interest rate risk (they are usually of longer maturity). Short-term US Treasury bills (“cash”) has had the lowest return but the lowest credit risk and lowest interest rate risk. Personally, I see this chart and am satisfied with my holdings of intermediate-term US Treasury bonds (green line) that keeps the highest credit risk but with effectively a ladder out to a longer average maturity.

But hey, those high-yield bonds still returned a lot more money over the last 20 years instead. Why not just hold those instead? First, don’t forget to step back and look at the bigger picture:

If you’re going to accept big swings, you might prefer one of the highest returning assets in the top-right corner. (I have no idea which one will be the absolute highest in the next 20 years, but I don’t think it’s an accident that all the stocks are grouped together in that top-right corner.) If you can hold on through the scary periods, the gap between stocks and bonds over the long run (~100 years below) is huge:

This is why many will advise you to own more stocks if you want an overall higher risk/potentially higher return profile, as opposed to riskier bonds. But before you get carried away, read this book excerpt Courage Required from William Bernstein. Bleak times will come again. Safe things have value beyond the rate of return.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Hey Jon do you have a post on nontaxable bonds?