One of my regular bookmarks is the TIPS real yield page (along with the regular Treasury yields). I noticed that the real yield on the 30-year TIPS has nudged above the 2% mark:

At the same time, the 30-year regular Treasury is at 4.3%, making the break-even annual inflation rate about 2.3%. Over the next 30 years, I’d take the over on that, or at least take some insurance out on the possibility of high inflation.

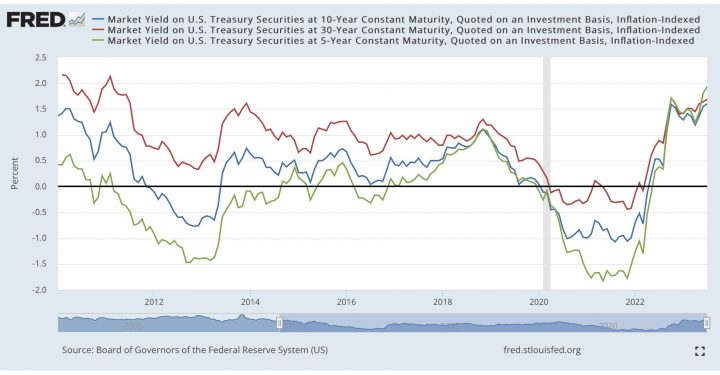

In addition, as David Enna of Tipswatch points out, this is the first time in a long while that all the various maturities (5/10/30 year shown below) are all around 2%.

If you wanted to, you can again construct a ladder of TIPS that will provide you a guaranteed inflation-protected income over the next 30 years (including spending down your principal) of over 4% above inflation (~4.4% as of this writing, as rates are higher today that at the time of writing for that post).

That means if you put $1,000,000 into a 30-year TIPS ladder right now, you can create ~$44,000 income for year 1 and then another ~$44,000 adjusted for inflation (CPI-U) annually for the next 29 years. All fully backed by the US government. No stock market volatility. No chance of annuity insurance company failure. Check out TipsLadder.com and Eyebonds.info if you are ready to get deep into the details.

While I am not looking into investing a lump sum into a TIPS ladder, I do own both regular US Treasuries and TIPS to provide the stable, guaranteed growth portion of my portfolio. (I’m roughly 70% stocks and 30% bonds.) If I’m getting guaranteed 5% growth from US Treasuries and guaranteed 2% + inflation from TIPS, I’m pretty happy with that for the safe part of my portfolio.

I am taking this opportunity rebalance my existing bond holdings and free cash to create an overall longer duration for my TIPS. I want to lock in that 2% real yield across longer maturities while it is available. Real yields might go even higher, but I’m more worried about it going lower than higher.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

You suggest a TIPS ladder. Is it really worth it to keep track of individual bonds, the cost of dealing with the tax implications, the difficulty of dealing with Treasury Direct for purchase and sales, for the average investor?

And then the nightmare your heirs will have trying to deal with this all? No thank you!

You can easily purchase TIPS through auction or the secondary market via any major brokerage (e.g., Vanguard, Fidelity, Schwab, etc.). It’s actually very easy – buy the TIPS, hold it, let it mature, and the funds get deposited into your cash account to spend or reinvest.

I purchase TIPS from Fidelity on the secondary market (easy as buying any stock with a limit order) inside a tax-advantaged account. I have never bought TIPS (via ETF, mutual fund, or individually) from TreasuryDirect nor in a taxable account.

But I agree, I wouldn’t want to buy them in TD and I would try to avoid the tax issues of owning them in taxable.

If an asset allocator holds individual TIPS and commits to holding them to maturity (which “lock in” implies), then at rebalancing time there is an option to use the market value or the inflation-adjusted principal value of the bonds. The former has more volatility than the typically slow steady climb of the latter as it grinds to maturity. I can see an argument for either method.

I’m not sure how other folks do it, but I have part of my TIPS holdings in ETFs and/or mutual funds, so it’s easy to buy and sell in smaller and specific chunks of money. I still hold in tax-sheltered accounts so no tax worries. Over time, I have gotten more comfortable with individual TIPs for more control and lower costs (no ETF expense ratios).

BTW, everyone can still take advantage of these higher yields with a TIPS fund, they are just made of individual TIPS inside, so it’s effectively a ladder too.