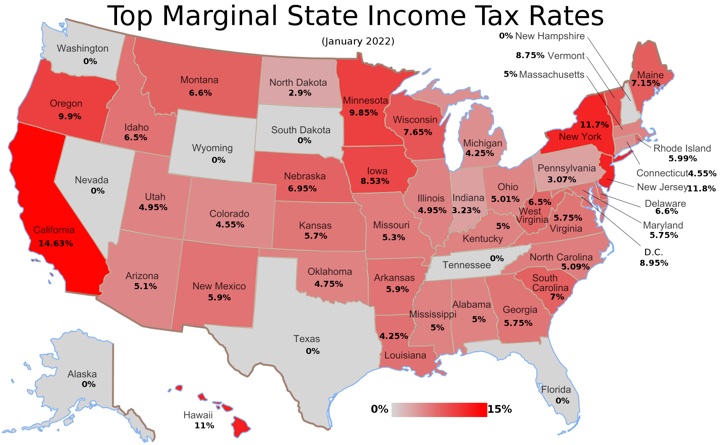

I’ve mentioned this before, but here’s a quick reminder as the tax-equivalent yields are now at 6% APY in most states with income taxes (anything 5% and up, see above graphic). Due especially to high state income taxes, my cash is mostly held in Treasury bills and money market funds that contain 90%+ treasury bills. Both can be owned within most major brokerage accounts that allow the purchase of individual bonds from either auction or secondary markets. (Treasury Direct allows purchase at auction, but I don’t like the user interface or customer service.)

So while I enjoy keeping track of new fintech apps, unless there is a good upfront bonus, it’s hard for me to justify another application at current rates. I skipped Milli when it hit 5.25% APY in August 2023. I skipped Elevault when it hit 5.50% APY in October 2023. I will likely skip Domain Money at 6% APY.

Treasury bond interest is exempt from state incomes taxes, which gives them a comparative boost over interest from banks. If you are subject to state income taxes, use a tax-equivalent yield calculator to compare Treasury bill/bond yields with interest rates from bank accounts and other bonds.

For example, if you are single with $70,000+ taxable income in California, your marginal state income tax rate is at least 9.3%. That means the 5.57% interest from a 4-week Treasury bill is equivalent to a bank account paying 6.42% interest or higher!

Be sure to check and make sure your “Treasury” money market fund is holding 90%+ Treasuries and not repurchase agreements. I’ve noticed that Vanguard Treasury Money Market Fund is now back to 94% Treasuries and only 4% repos, but that could change again in the future, so I’m keeping an eye on it.

Finally, at tax time be sure to look up the appropriate U.S. government obligations income information and use it when filing your state income taxes. You may need to nudge your accountant along with supplying this information.

[Top image credit – Wikipedia]

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I built a ladder on 3 month bills through treasury direct. Jonathan, it’s good you pointing out the equivalent rate based on state taxes. It’s easy money right now

Good Article. Where are everyone finding 5.57 yield 4 weeks bonds? i use fidelity and when searching new issue treasury bonds I have yet to see anything over 5.3%.

I usually use this bookmark to track rates:

https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_yield_curve&field_tdr_date_value_month=202310

Does Fidelity have a Treasury fund similar to the Vanguard Treasury MM fund with a high percent of Treasuries vs repos.

Yes look up FDLXX

Thank you for the FDLXX suggestion! That fund is about 91% treasuries.

Also, I am using the Fidelity tax equivalent calculator linked in your post. Which column gives me a comparison for a Savings account? Would it be CDs?

CDs would be the a bank account comparable, as bonds are usually for a fixed term as well. So a 1-month T-bill would be like a 1-month CD, close to a savings account.

Do you recommend buying on directly from IRS or from vanguard? On vanguard I don’t see this high rate.

VUSXX, on 10/29/23, has a 7-day yield of 5.32% with an expense ratio of 0.09%. But note that 3.7% of the fund is state-taxable repurchase agreements. So slightly worse return than laddering T-Bills with TreasuryDirect, but more convenient in terms of liquidity and management.

Still trying to wrap my head around this…

I have a Cash Management account at Fidelity and hold funds in SPAXX. If I trade it for FDLXX (which has nearly identical performance), I could potentially save on my Wisconsin Income tax?

Possibly, depending on the rate differential and the amount of Treasuries/Repos held in each respective fund.