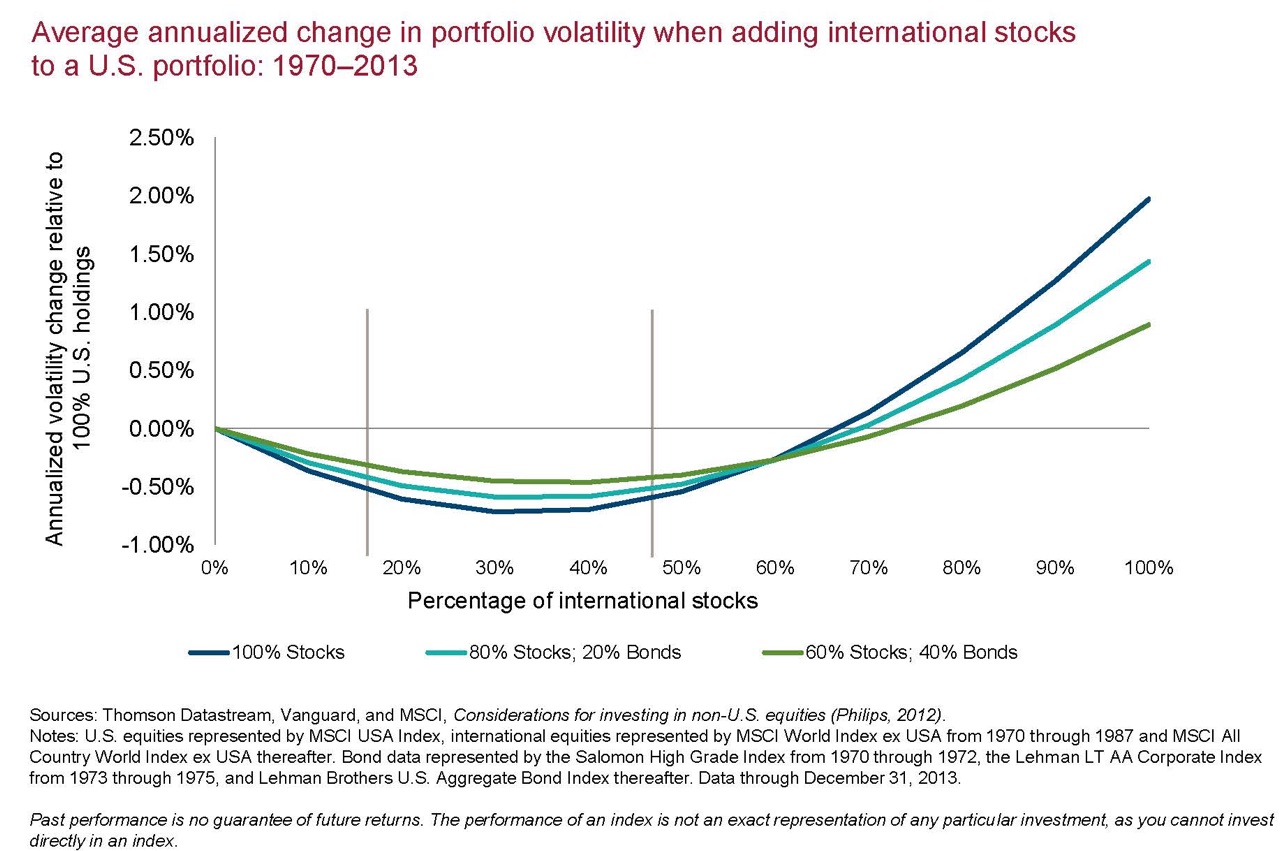

One of the decisions a DIY investor needs to make is how much international stock exposure to add to their portfolio. Recently, the US stock market has had much higher returns than non-US stocks overall, including Emerging Markets. But this Vanguard article reminds us of the diversification benefits of adding international stocks. Somewhere between 20% and 50% is the historical sweet spot:

One of the decisions a DIY investor needs to make is how much international stock exposure to add to their portfolio. Recently, the US stock market has had much higher returns than non-US stocks overall, including Emerging Markets. But this Vanguard article reminds us of the diversification benefits of adding international stocks. Somewhere between 20% and 50% is the historical sweet spot:

Vanguard says 60/40 is best. Over the past year or so, Vanguard has shifted their “ideal” stock asset allocation to 60% US and 40% international. This is the breakdown used for their Target Retirement 20XX funds, their LifeStrategy funds, and also their 529 College Savings Age-Based portfolios. Part of their justification is that the expense ratios for their international funds has dropped as well.

World market cap weighting is at 52/48. What do the global capital markets have to say? The world market cap weighting has shifted to 52% US and 48% non-US, as tracked by the Vanguard Total World Stock ETF (VT). VT tracks the FTSE Global All Cap Index which is a free-float-adjusted, market-capitalization-weighted index.

I like simplicity and symmetry, so I am sticking with 50/50. I’m just one amateur, but I feel the trend is towards a market-cap weighting. 50/50 isn’t all that far from 60/40, especially because my overall asset allocation will soon by 60% stocks and 40% bonds. 50/50 is also really easy to rebalance and makes my portfolio looks nice and symmetrical.

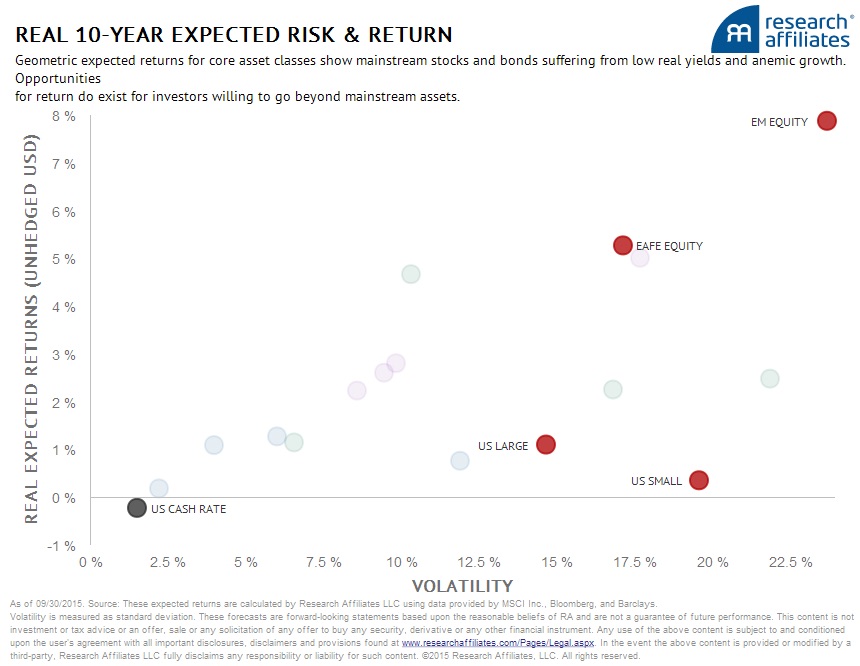

Want some support to own international stocks? If the recent poor performance of international stocks has you down, Research Affiliates recently updated their Expected Returns Chart (mentioned previously) and it shows Developed European, Developed Asian, and Emerging Market stocks having a much better outlook than US stocks:

They use a mix of different historical valuation techniques to make these forecasts, so they aren’t just pulled out of thin air.

Want some support to NOT own international stocks?

While it is hard to argue against the historical diversification benefit of owning some international stocks, I don’t know if it is absolutely necessary. If you bought big chunk of the S&P 500, and a smaller chunk of US Treasuries, and ignored it for 30-40 years, you’d probably come out pretty happy. Some big names would agree:

- Jack Bogle (if you didn’t know, the Founder of Vanguard!) says you don’t need international stocks.

- Warren Buffett’s advised portfolio for his wife’s trustee upon his death… includes no international stocks. It is simply 90% in a low S&P 500 index fund and 10% in short-term government bonds.

One argument is that many US companies already make a huge chunk of their money from their international operations anyway.

So there you have it. I hope you are sufficiently confused.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I stick with 20% directly held in international and I figure the international operations of many of the multinationals traded domestically will get me anything else I need.

I would say that 40%- 50% of S&P 500 company revenues are derived internationally. Therefore, you are already diversified to the whims of the global economy.

By adding foreign stocks you could be overexposing yourself to international diversification, and adding the extra risk of currency fluctuations. The rule of law and property rights in plenty of foreign countries are not as strong as they are in developed countries such as the US, Canada, UK etc. IF expected returns on foreign stocks are similar to those of US stocks, then it makes little sense to add them for the sake of diversification.

I would agree with Bogle that owning no international stocks is fine. If you must have exposure, I would also agree that no more than 20% is possibly the best scenario.

Jonathan-

At the current interest rate level, what justifies to put 40% in bonds? For sure, the interest rate will go up and bond prices will go down. Isn’t?

They are still less volitale than stocks, also, the market is already aware that interest rates will likely go up, so that should be factored into the price of bonds.

There are talks if rate increase since 3 years now. They may go up today, a year from now, or more. No one really knows. I’m sticking to my (age-18)% bond allocation, which means I’ll be under 15% for a couple more years.

How do you decide between developed/emerging within the international portfolio? I know you just buy total international which consists of roughly 18% in emerging.. but what other things do people use to decide?

I think the numbers not just in this posting but in all these expert advice articles on diversification and domestic verses international holdings are meaningless especially in a deflationary world with seven years of 0% interest rates, a strong US dollar, collapsing commodity prices and a US Central Bank that games people to take on more risk (and it doesn’t take too many actively working short term memory brain cells to know how badly that games going to end).

Based on your income or retirement strategy and level of risk aversion you need to seek out investment opportunities where ever they are in the world that you as US citizens with the handicap of FBAR reporting following you around can still invest. And do it in a way that allows you to be nimble enough to unwind the investment when risk parameters change. The ultimate percentages are defined by the opportunities not the other way around.

FWIW, I am also 50/50 US/International for my stock component of my portfolio.

Jeremy Siegel suggests 40% foreign.

There is a difference between owning a US company that does 40% of business overseas and owning a foreign company. According to a recent report, China now has more Billionaire than US. These Chinese got rich doing things in China. China is growing fast.