The hot buzzword right now is “FinTech”, where technology will help us manage our finances more and efficiently than before. But I’ve also been tracking the reasons why working with a human advisor can be worth the money and time spent. As I’ve mentioned, the strength of the book The One-Page Financial Plan by Carl Richards is that you’re hearing the voice of an experienced financial planner who also has the skill of distilling his experiences down to a sketch. Here’s how he puts it:

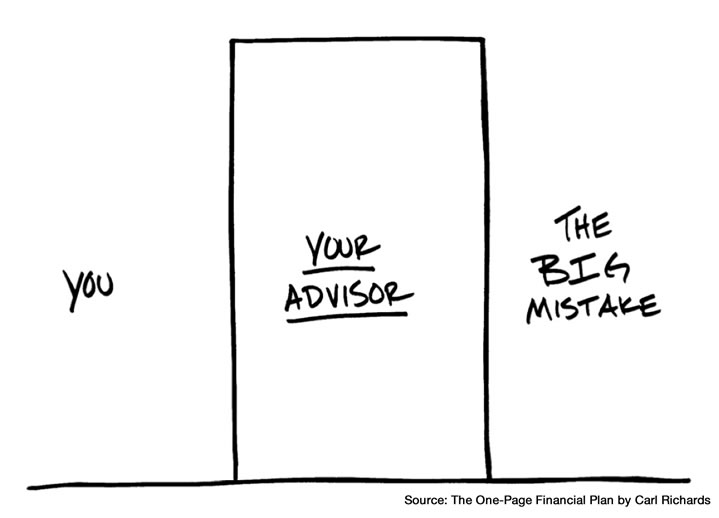

Takeaway: A good financial advisor keeps you from making The Big Mistake that derails your plans.

The big institution Vanguard says that a good financial advisor should be able to improve the performance of a “average” client’s portfolio by about three percentage points in the following ways. Take note of which one factor makes up half of that 3%:

Takeaway: The biggest “value add” from good advisors is their “behavioral coaching”.

Here’s more incisive commentary by Josh Brown of The Reformed Broker, called When the flood comes:

When the flood comes, all of the bullshit arguments among the financial commentariat will come to an end. This will be my third time through. Believe me. We will not be arguing about how many basis points an advisor charges versus another advisor or a software program.

The people who are there for their clients and keep a cool head in public will come through okay. More than okay – they’ll actually raise assets from new and existing households who realize what a mistake they’ve made with their previous advisor or solution.

Takeaway: A good client advisor will help you keep your cool when the next disaster comes.

I’m sure you’ve caught onto the theme by now.

The value in a financial advisor arrives when they help you maintain your plan through both the good times and bad. They will prevent you from participating in the mania during the next bubble, and they will keep you from bailing out during the next crisis.

The problem is, how do you find this “good” financial advisor amongst a sea of average to downright dangerous ones? Here’s some advice from The One-Page Financial Plan:

To a certain extent, the process of finding a real financial advisor is a qualitative experience. It boils down to the question “Can I see this person getting to know me well enough so that I can trust him to help me behave for the next twenty years of my life?” Yes, you should verify that they’re properly registered. Do a Google search of their regulatory record. I’m not talking about blind trust here— the kind that would allow someone to steal your money. I’m talking about finding someone who’s willing to get to know your goals and values well enough to help you stick with your plan. Remember, your financial advisor is the only one standing between you and the Big Mistake of buying high and selling low. You’re hiring them to do what you can’t: make unemotional decisions about your portfolio. If they can’t do that, why pay them?

Now, I still don’t see myself hiring an outside advisor. But I do keep my portfolio conservative enough that my portfolio “boat” stays relatively stable even in rough weather. We’ll see if I can remain unemotional during the next flood, as it is not a matter of “if” but “when” the next one comes along.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

It is hard to find a good advisor thats why people are relying on self education through blogs like this one.

Yes, that has always been the riddle in all of this.

I met Chris Farrell a few years ago – Chris once hosted APM’s “Marketplace Money” and still contributes, writes for the Minneapolis Star-Trib, books, etc. He advocates low-cost, indexed funds and never using a financial planner who makes commissions, advising people interested in financial advise to use fee-based advice only.

When I pressed him about how to vet a planner – separate the ethical professionals from the flaks – he advised first checking the National Association of Personal Financial Planners (http://www.napfa.org) and the Garrett Network (http://garrettplanningnetwork.com), as these folks all are Certified Financial Planners and then some.

But, he cautioned, just having that list is not enough. You still need to do your homework: cull those lists and then try to find your own references (friends, family, etc.) who have worked with some of them; search online for news stories; understand what you want to accomplish before you meet with them (buy a home, save for financial independence, fund a business start-up, etc.) and then meet with them for an introduction, to see if they have worked with others with similar goals and get an idea of how they work.

That won’t guarantee success, but helps your odds greatly. If someone is good and ethical, their clients will sing their praises – that seems a rare character trait in any profession these days.

Yeah, I wrote a blog piece about a reader who was rejected by a Garrett member because she didn’t take hourly fees! Garrett rep was appalled by this financial adviser unprofessional conduct of a Garrett member. Here is the story: http://latebloomerwealth.com/2014/09/12/did-garrett-planning-network-pass-the-smell-test/

Thank you for posting, Steve.

More importantly, thank you for checking further into the story, talking with the planner and then talking with Garrett. Clearly, this planner is not the type of person they would want to refer, given their stated mission.

Which prompts the question, is she still on their recommended planner list?

Hi Ron,

Your welcome. That piece has generated a lot of views. Unfortunately, that “adviser” is still on the Garrett list. The offended party never contacted Garrett to issue a formal complaint.

This issue is that that adviser will never sell a commissioned product which is I think the primary policy of a Garrett member, even though Garrett rep says that a client can see a Garrett adviser for the hourly fee only.

It gets complicated. I get the gut feeling Garrett and NAPFA allow some unwritten or unspoken leeway about their advisers to use AUM, as long as they never sell product.

I don’t like AUM fees and I shutter to think how many Garrett advisers charge 1.0% or more for those clients who just bring their paperwork dump it on the adviser’s desk and tell the adviser, “OK, you do this” and leave. But that’s another issue.

This is the other complication: by the time a client knows enough to properly evaluate a fee only adviser, the client knows how to be a DIY. That’s is exactly what happened to the client in my article.

I have thought long and hard about this and there are no easy answers. The problem is that even for a fee only financial adviser, charging the AUM stresses the system. The overall stock market returns about 9.5% annually for decades. By the time you take into account inflation, ordinary income taxes, AUM, hourly fee, and investment costs, after four decades of working, that client has paid dearly for a fee only financial adviser. Yeah, the client has gotten good advice by a trained investment professional, but I think its too expensive because the “system” does return enough to cover all of the potential costs and keep pace or beat inflation.

Any comments?

I agree with Jonathan – I can’t see using an adviser simply to protect me from myself at a cost of at least 100 basis points per year. And I’ve found few of the advisers I’ve encountered are all that sharp – even if they write a book (The author of the book mentioned in this post, Mr. Richards, has been very open about how he walked away from a mortgage in Las Vegas due to financial problems…hmm). Diversification, low costs, and a calm historical perspective are more valuable than some “genius” dispensing advise.

No financial advisor for me. I’m figuring it out from the Bogleheads forum and you.

I’m approaching a point in my life where I can say — and not to brag — that I have reached a degree of financial success, and financial independence is visible on the horizon. That is largely due to my own study and research — at sites such as this one and many others. But in having reached this point, I do find myself wishing I had a relationship with someone that I could bounce ideas off on, solicit suggestions from, and perhaps hear some new investment ideas. Unfortunately I’ve found that most advisors, planners, etc. that claim to be independent and unbiased are never quite what they seem. When I start digging into the details on their websites or printed materials I inevitably find there is some affiliation or cross-ownership with a brokerage firm, and — despite the upfront promotion of fee-only or hourly rate pricing structures — I will find the term “commission” somewhere in the fine print.

I wonder what Tim Duncan has to say on the topic.

http://bleacherreport.com/articles/2499763-tim-duncan-comments-on-losing-more-than-20m-due-to-financial-adviser

I 100% agree with this article. If you let the darn mutual fund do it’s job, you’ll do just fine. We get in the way of ourselves. Aside from dollar cost averaging and portfolio balancing in qualified accounts, leave it alone. You’ll most likely get those high returns. Another big investment firm just came out with another observation and it was that the investors who received the best returns in their accounts were the ones who forgot they had an account. It’s like dieting, pretty much every diet plan works as long as you stick with the plan and not act on your emotions.

I am very lucky to have earned the DIY status. I had to go through the learning curve by enduring massive mistakes later in life and still come out with a comfortable next egg, despite going through two of the biggest stock market crashes in history.

My degrees in psychology and Buddhist teachings helped keep the cool during bear markets. I only pay 13 bsp in costs with all my money in Vanguard.

A very late update.

That planner in my story posted above was FINALLY removed by Garrett Planning Network. But it would not have happened had the client contacted me and then I called that “adviser” and I contacted Garrett to complain. We have to report these people, even if they are fee-only “fiduciaries” listed on NAPFA and Garrett, unfortunately.

Steve