An important tenet of portfolio construction is diversifying between stocks and bonds. While poking around on Morningstar, I stumbled across a quick real-world example of how this works.

Let’s say you had $10,000 back on January 1st, 1993. Now, let’s see how that money would have grown over time until today (August 9, 2013) depending on what you invested it in. That’s means holding over a 20-year period – that’s 20 years of bubbles, crashes, euphoria, fear, and a constant flow of bold predictions and catchy newspaper headlines.

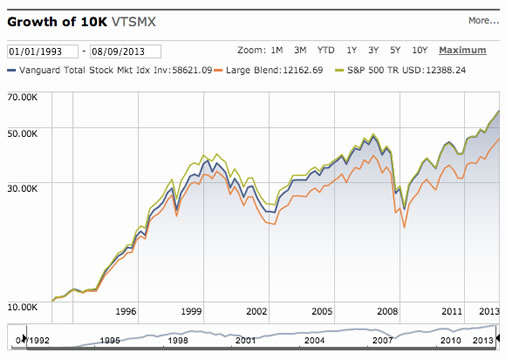

1. Vanguard Total Stock Market Index Fund, Investor Shares (VTSMX).

Let’s say you invested in this huge, popular index fund that passively tracks the entire US stock market. (See What’s Inside the Vanguard Total Stock Market Index Fund?) From afar, you may be happy with this chart. But having lived through it, I can say that it was quite a wild ride. People tend to remember the highest value of their portfolio. Your money would have grown to $37,000, only to fall all the way back to $23,000 in the Tech Bubble Crash (a 38% drop). Later, your $46,000 would have dropped 50% all the way to $23,000 during the Housing Bubble Crash. So between 2003 and 2009, your money would have gone nowhere even as inflation rose. Many people went to cash. But if you stuck it out, today you’d be sitting on a balance of $58,621.

2. Vanguard Total Bond Market Index Fund, Investor Shares (VBMFX)

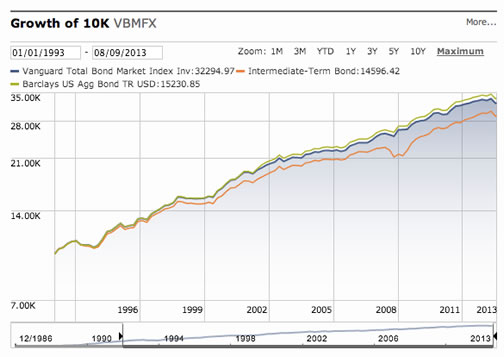

Now, what if you invested in this fund that tracks the overall US bond market?

(See What’s Inside the Vanguard Total Bond Index Fund?) As you can see, your money would have grown rather steadily with no major hiccups. You’d just have to sit back and collect those interest payments, even though from time to time the stock market would be zooming upwards. From 1993 to 2013, your $10,000 grew to a balance of $32,295 today.

3. Vanguard Balanced Index Fund, Investor Shares (VBINX)

Here’s another simple yet elegant creation of Jack Bogle, founder of Vanguard. This fund essentially holds 60% Total US Stock and 40% Total US Bond. Rebalanced regularly. 60% Stocks. 40% Bonds. No active management, no market timing, just 60/40 all the time.

As you might expect, the performance is a mix of the two funds above. From 2000-2003, your balance would have dropped from $26,500 to $22,000 (~17% drop). From 2007-2009, your balance would have dropped from $37,000 to $26,000 (~30% drop). Those are some scary drops, but definitely not as bad as holding 100% stocks. Hopefully, having those valleys smoothed out a bit would make it less likely you bailed out at the bottom. Now, this means the peaks were also smoothed out, but today you’d still have a balance of $49,167.

Bottom line. Over the last 20 years, if you bought 100% stocks and held on through it all, you’d have ~$60,000. 100% bonds, ~$30,000. By going with a 60/40 Stock/Bond split and rebalancing regularly, you would have ended up with about $50,000. I think that’s a pretty good trade-off. Hopefully, the milder swings would have kept you in the game.

There will always be predictions about the future. Interest rates may rise quickly, rise slowly, or even drop further for a while. This bull market in stocks may keep on going. Or stocks could drop 50% this year again. Nobody knows the future, even if they sound confident. Honestly, right now neither stocks nor bonds look all that promising to me. But I keep thinking long-term and remember the benefit of holding a balance of stocks and bonds (currently about 70/30 stocks/bonds).

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Good analysis. However, since I myself or anyone I know just do a US stock-US bond split I was wondering if you could do the same thing for something closer to the following (very similar to your own portfolio):

US-Stock

US-Bond

REIT

Int’l

Emerging

Small Cap

Basically, I just want to know if the above would have beaten the total US-Stock during that same period. Thanks in advance.

Hi Jonathan, can you comment if you think there are any difference re: fees for holding the Shares + Bond Indexes separately vs the Balanced Fund? Trying to work out why we would not go with Retirement Target Funds or Vanguard Balance Funds?

I can’t find much information from the books I’ve read either.

Thanks!

Amy

Following up from Amy, I’m also curious about the same $10,000 over the same time period but with 60% in Total Stocks and 40% in Total Bonds. As far as I can tell, the (current) expense ratios are as follows:

VTSMX 0.17%

VBMFX 0.20%

VBINX 0.24%

Rather than looking at one of the retirement target funds (higher expense ratio), I’ve mirrored their approach using a variety of index funds (lower individual expense ratios).

Ethan, I think for the “work” of not rebalancing once or twice a yr for 2-3hrs, would the higher fee be justified so we don’t get into any human errors/self control issues? Are the returns the same just less fees (granted the Balance Fund has other Asset Class holdings too right?)

I believe a lot of the value of going with a balanced fund or target date fund comes from the regular rebalancing. Unfortunately, most people do not have the fortitude to do the right thing and rebalance how and when they should (if they do at all).

So, I think if one pays a few extra basis points for that feature it will likely pay for itself several times over for the majority of investors. Another case for being penny wise and pound foolish IMHO.

@Amy – Balanced fund is older than Target funds, so easier for this analysis. But the Target funds are another form of a balanced fund, with the unique characteristic that the asset allocation shift over time according to a set schedule “glide path”. It’s still not certain that a glide path is all that much better than simply 60/40 all the time, but I’m okay with it. I directed my parents to hold their Rollover IRA in a Vanguard Target fund.

@Ethan – It would be slightly cheaper to split it up, but you do lose the automatic rebalancing. I split things up myself because of the tax differences between stocks and bonds.

@Amy – Balanced fund is almost mirrors exactly 60% VTSMX/VTI and 40% VBMFX/BND, so if you rebalanced monthly or quarterly on your own you’d probably get the same overall return. 60% of $58,261 plus 40% of $32295 is $48,091 so even if you didn’t rebalance you’d be close. There appears to have been a slight “rebalancing bonus” during this period to get the $49,167 number.

@Jack – I would agree that if having a balanced fund keeps you from tinkering or market timing, that’s a definite benefit. If I had all my money in an IRA/401k, then I’d be much more inclined to hold everything in a balanced-type fund. But I like taking advantage of the inherent tax efficiency of VTSMX in a taxable fund and leaving my bonds in tax-sheltered status given my high tax bracket.

Hi Jonathan, can you elaborate on tax-sheltered bonds? Didn’t realize there were tax consequences on separate index funds va balance funds.

You can have your $50,000. I’ll stick with my $60,000.

I have very little in bonds and only because my work gets me into some portfolio that some “geniuses” at MSDW manage for millionaires and is supposed to be great. Fine, I decided to play back then. HOWEVER….

If the old adage that bonds are great as interest rates dive, then how in the world can bonds be worth much of anything going forward VERSUS something like any other interest – critical investment (CD’s, annuities, etc) that will follow the rate trend UPWARD!!

I just don’t see bonds being worth much for the next decade or longer.

I believe the investment performance of these portfolios support the point David Swensen made in Pioneering Portfolio Management that a balanced portfolio’s main purpose is psychological: to smooth out volatility, it won’t get you the highest performance. Over the long run, equities provide the greatest probability to achieve the highest returns. It’s just a matter of staying disciplined when equities are tanking.

REd : You’re right that bonds will lose some value when interest rates rise. However thats offset by the yield from the bonds. And shorter term bonds are not going to be hit as hard so you can minimize the problem there. Its not like a total loss and bonds won’t just plummet. But I think a lot of the reason to have bonds in the mix is to keep an asset blend that is balanced. That lets you shift to buying some stocks when they’re down and selling them when they’re up.

I was one of those people who transfered their 401 k plan into liquid cash savings during the melt down.

I haven’t done the exact math but i can tell you that my co-worker, who did stick to the advice that “I” had given him and kept making contributions to whatever funds that he had picked before throughout the meltdown, has approximately at least $30,000 more in his account than mine. We entered the job at the same time and I believe he contributes less than I do per paycheck. I tried to stick to my own advice but fear got the better of me. Even though I only pulled out for a little less than a year, it had a noticeable impact. I won’t be making that mistake again.

Jonathan, is it the case that during a different time period, namely 1982 – 1999, the correlation between Stock and Bond markets was different to the correlation from 1998 to present? Therefore the analyses changes if the time period is extended?