Vanguard is the one of the biggest providers of defined contribution (DC) plans like 401(k) and 403(b) plans, with more than 3.9 million participants. An optional service they provide for these DC plans is managed account advice, where you pay them an asset-based fee and you cede all portfolio control to them. Vanguard Managed Account Program (VMAP) serves as a fiduciary that sets asset allocations, chooses investments, and monitors/rebalances portfolios on a continuing basis. Fees typically begin at 0.40% on the first $100,000 in assets under management.

Vanguard is the one of the biggest providers of defined contribution (DC) plans like 401(k) and 403(b) plans, with more than 3.9 million participants. An optional service they provide for these DC plans is managed account advice, where you pay them an asset-based fee and you cede all portfolio control to them. Vanguard Managed Account Program (VMAP) serves as a fiduciary that sets asset allocations, chooses investments, and monitors/rebalances portfolios on a continuing basis. Fees typically begin at 0.40% on the first $100,000 in assets under management.

Vanguard published a research paper on the before-and-after results from actual participants called The value of managed account advice [pdf].

Even if you aren’t considering paying for such a service, I figured there would be some worthwhile takeaways from their results. Here are my condensed notes from reading their paper.

Reallocation of company stock. About 12% of participants initially had a concentrated position of 20% or more in employer stock. Holding too much stock in your employer is generally understood to be too risky, so VMAP fixes that. The average allocation to company stock fell from 46% to 4% as a result of managed account advice. This group was probably impacted the most by professional advice.

Personalized advice. Not only do you simply indicate an expected retirement age and desired level of risk, but you can add outside assets to the overall asset allocation evaluation. 35% of all VMAP participants personalized the service in some manner.

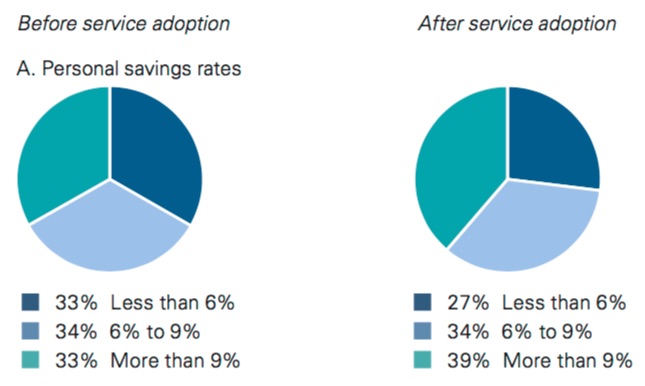

Forcing you to make savings rate decision. When you sit down and start this service, you have to talk about your goals and see some projected numbers. Then you must make a decision as to your savings rate. Overall, people saved more once faced with this situation. Specifically, 1/3rd of participants increased their savings rates, 7% decreased them, and the remaining majority maintained contribution rates at the same level. See chart below:

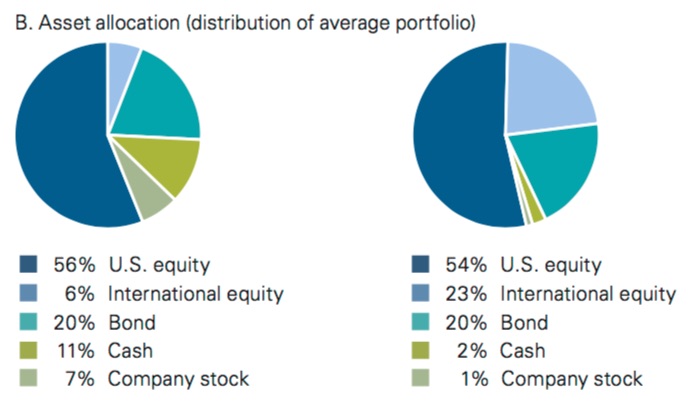

More appropriate asset allocation. In terms of asset allocation, VMAP made things more appropriate and efficient in relation to the need and ability to take risk. Some people got more equity exposure, some people got less. On average, people were told to hold less employer stock, less cash, and more international stocks. See chart below:

Net effect on retirement wealth. Let see. On average, VMAP participants saved more money. On average, expected returns on VMAP-advised portfolio rose. On average, expense ratios on VMAP-advised portfolio were reduced by 0.06%. But everyone also paid advisory fees. What happens when you take all the factors together? In their own words:

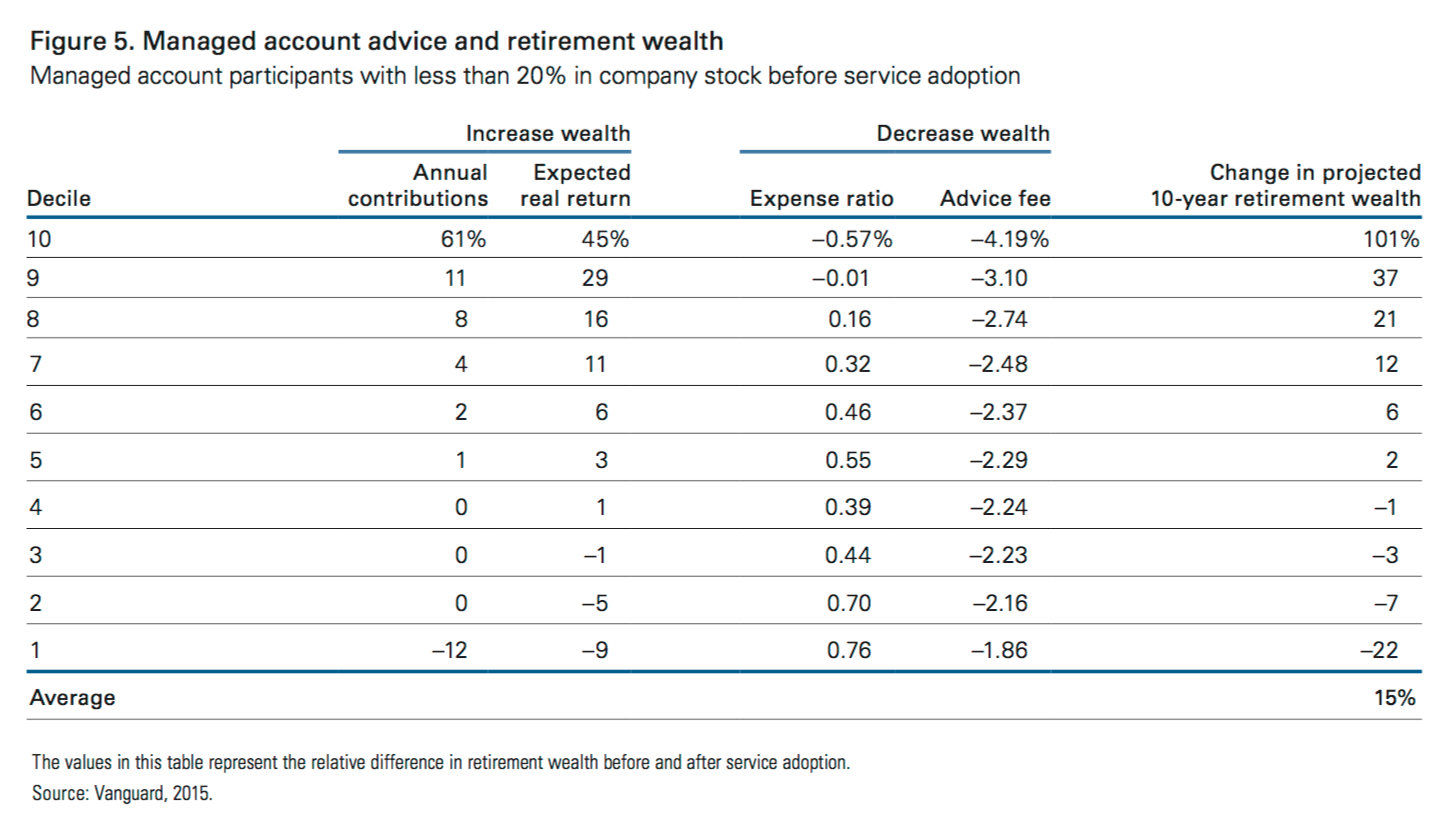

To summarize the interplay of these effects, we used the change in participants’ projected ten-year real retirement wealth as a benchmark for evaluating advice. This allowed us to observe the true effect of managed accounts, independent of the participant’s starting account balance or asset allocation.

On average, managed account participants experienced a relative increase of 15% in projected retirement wealth over 10 years. I’m a little disappointed in “projected” wealth increase vs. actual wealth increase, but I think that’s the best they could do with their limited data set. In order to better see how this works, they broke things into ten equal groups, or deciles, based on the change in retirement wealth. This chart includes the 88% of participants that didn’t have a huge chunk of company stock to start with.

As you can see, the bottom decile is mostly affected by the fact that they simply chose to save less money (lower annual contribution rate) and they lowered their stock exposure (lower expected real return). I can only guess that these folks needed to lower their risk levels to a more appropriate level. The top decile both chose to save more money and increased their stock exposure.

Summary. Each of the factors listed above could all be converted to standard advice, i.e. “Things an Investor Should Do”. You should make sure not to hold too much company stock. You should assess your situation, and increase your savings rate if needed. You should make sure your asset allocation is appropriate for your age and risk requirements. Yes, a DIY investor could certainly do these things for themselves. But have you? Will you?

This part is purely my opinion, but how about a general rule, if you haven’t done these things in the last 3 years, perhaps paying for advice may just be worth it? For example, if you’re holding more than 30% of your portfolio in company stock, and haven’t gotten rid of it in the last 3 years, maybe you need someone to do it for you.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

The advice provided seems valuable and worthwhile, but changing an investor’s asset allocation and savings rate don’t require an ongoing AUM fee. These could be addressed in a one-time hourly fee consuItation session. Maybe the VG paper, which I didn’t read, addresses what ongoing services are provided, but my take is that the AUM fee only serves to spread the cost of an initial consultation over time, likely at a much higher total cost.

Rather than pay a fee for AUM; it would be better if Vanguard had a service where you could pay a fixed fee and have them review your portfolio and plan. I thought they did have this at some point but I can no longer find it on their website 🙁

Vanguard does have a “Financial Plan” service that costs $250 for those with $50k+ assets (Voyager), free for $500k+ (Voyager Select), and $1,000 for under $50k in assets. They will provide a written plan and recommendations, but they won’t take the wheel completely and execute trades on your behalf.

I could not find it on their website. Looks like it is no longer offered (might have been in the past?) and they only offer AUM

I think you are right, looks like they changed it sometime in 2015, sorry for the outdated info. If you reach a certain asset level, you can “consult with a CFP” for free. But for asset management I guess they want folks to pay 0.3% AUM for VPAS:

https://www.mymoneyblog.com/vanguard-personal-advisor-services-review.html

Here is a pertinent Bogleheads forum thread:

https://www.bogleheads.org/forum/viewtopic.php?t=160360

I fear firms like Vanguard and Betterment will be getting an undeserved bad wrap for a while… Most of them bump up the international exposure of portfolios pretty significantly. (Vanguard’s average international allocation jumped from 6% to 23% above.) It just so happens it’s been a horrible market for international the last few years. In 2014, the S&P outperformed the EAFE by 20% and it’s been even worse for emerging markets.

Some pretty bad luck for the robo-advisors as people will likely place the blame for under performance on the technology rather than the cyclical nature of the market.

Any robo-advisor who overweights on int’l and has zero allocation to real estate is worthless imo. Just compare what 10% real estate + 10% LT treasuries does to your portfolio in terms of downside protection, and compare it to the “impact” on the upside. The problem with Betterment is that it underperforms in this type of market on the up, and the down.