Updated May 2016. WiseBanyan has made some changes to their product. The highlights:

- New logo, mobile-responsive site design, and smartphone apps.

- Tax-loss harvesting now available as paid feature. WiseHarvesting is their first premium add-on feature, running 0.25% of assets annually with a $20/month cap.

- Now accepting IRA, Roth IRA, and 401(k) rollovers.

- Free financial planning software called Milestones. More thoughts below.

WiseBanyan is an online portfolio advisory service similar to better-known competitors like Betterment and Wealthfront. Differentiating feature: WiseBanyan charges no advisory fees, no trading commissions, and no minimum opening deposit. They will design, buy, hold, and rebalance a basket of low-cost ETFs for free, and all you are left with are the ETF expense ratios which you’d have to pay anyway if you DIY’ed.

Thanks in part to your interest as readers, I was able to get off their waitlist and open an account with $10,000 of my own money back in March 2014. As of May 2016, there is currently no longer a waitlist. Here is my review as an actual user for roughly a year; I have since liquidated my holdings in all robo-advisor platforms.

Application process. The account opening process was similar to other discount brokers and online portfolio managers. You must provide your personal information including Social Security number, net worth, income, investing experience, etc. No credit check. They do check identity, so they may ask for supporting documents if you just moved or something.

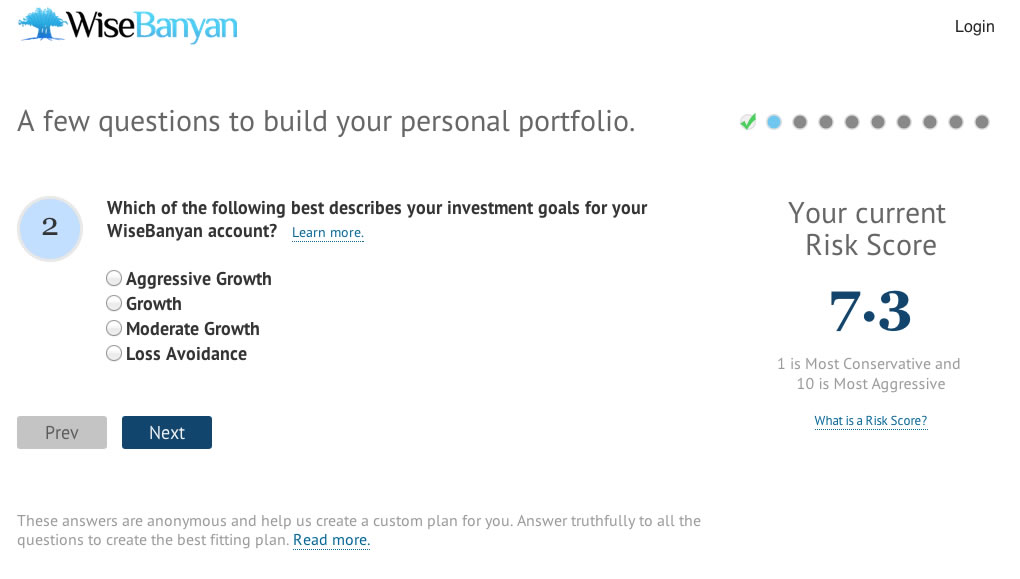

There is then a risk questionnaire. The questions can seem mundane but take it seriously, as the 10 answers you provide will directly determine the portfolio asset allocation that they choose for you. There will be no follow-up surveys, e-mails, or phone calls. Here is a screenshot and example question (old interface):

Funding. You can fund your deposit electronically, using your bank routing and account number. (They only accept bank wires as an alternative, no paper checks.) The money gets sucked from your bank and the portfolio is bought immediately when they get the money.

Fractional shares. WiseBanyan uses FolioFN as their broker-dealer (separate company that hold your assets in the background) which means they can use their ability to keep track of fractional shares. Most discount brokers and other online portfolio managers require you to own whole shares, so you’ll often have something like $57 sitting in cash.

Recall that WiseBanyan has no required minimum deposit or portfolio balance. If you really did open account with $100, they will actually buy less than one share of several low-cost diversified ETFs and you’ll own tiny, tiny portions of thousands of companies with no idle cash. With a normal discount brokerage, that might not even buy you one share of anything (VTI is over $100 a share on its own).

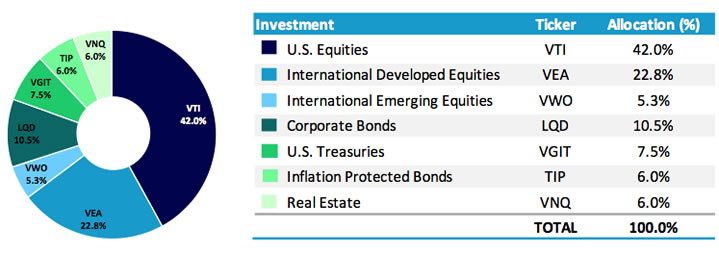

Portfolio asset allocation. I was assigned a portfolio risk score of 7.7, which corresponded to a stocks/bond ratio of 70%/30%. Screenshot from the old interface:

Here is the target asset allocation that I was assigned:

My portfolio was constructed using the following seven ETFs:

- Vanguard Total Stock Market ETF (VTI)

- Vanguard FTSE Developed Markets ETF (VEA)

- Vanguard FTSE Emerging Markets ETF (VWO)

- iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD)

- Vanguard Intermediate-Term Government Bond ETF (VGIT)

- Vanguard REIT ETF (VNQ)

- iShares TIPS Bond ETF (TIP)

My general opinion is that the ETF allocations from all “robo-advisors” are at least 80% the same, and with the remaining 20% you can’t really tell who’s going to win performance-wise anyway. They are all backtested using some form of Mean-Variance Optimization (MVO) and Modern Portfolio Theory (MPT).

While not exactly what I would have chosen for myself, I personally think the portfolios they create are fine. The ETFs have low costs and come from large, respected providers in Vanguard and iShares. All of the major asset classes are covered. There are no commodities futures or natural resource ETFs, which some experts think are useful and other experts think are useless. Note that REITs are considered to be in the bond category.

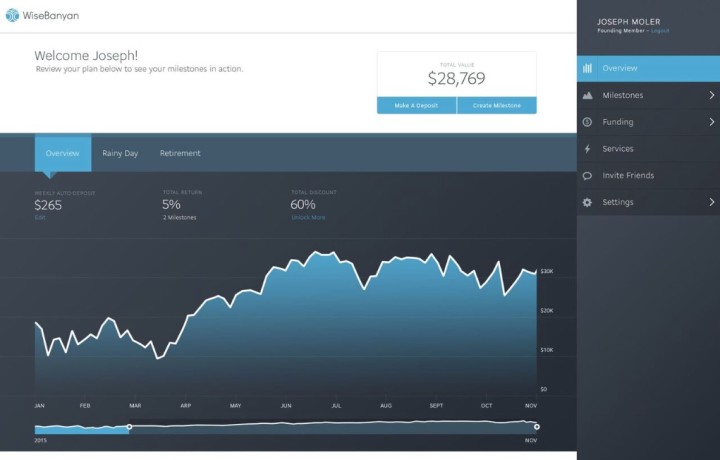

Website user interface and smartphone apps. The interface has been updated to essentially look like everyone else. It is simple, clean, and mobile-responsive. I like it. There are also companion iOS and Android apps. User reviews for both apps are overall positive. Screenshot from new interface:

Statements and ongoing communication. Electronic statements are free, but paper statements will cost $5 each and paper trade confirmations $2 each.

New Milestones feature. WiseBanyan has a new service called Milestones which helps you direct your investments into specific goals like retirement, emergency funds, college, or vacations. Works in desktop and mobile. You can give a target number and timeframe, and it will recommend a portfolio and a monthly savings amount that theoretically should reach your goal. It will initiate recurring deposits so that things are automated. While I think such basic guidance can be helpful to get you a ballpark figure, I would also be careful on relying too closely on the forecasts as nobody really knows what the stock or bond market will return in the short-term. Screenshot from new interface:

Free is nice, but how will they make money? Future concerns? According to various sources, the demographics of the average WiseBanyan client is both younger and of more modest means (opening balances under $10,000) than their competitors. They plan on offsetting the costs of maintaining free accounts with their premium add-on features, but will it work? Will enough people pay up for tax-loss harvesting? It remains to be seen if the “Freemium” model can work in this environment.

Bottom line. WiseBanyan is fully functional and delivers on its promise of free automated portfolio management. I joined them in early 2014 when they were still working out some minor kinks, but two years later they are offering a much more polished product. I would even say that their aggressive pricing has helped “nudge” many of their competitors to lower their starting minimums as well.

The main thing that would worry me is that their path to sustainable profitability is not clear. If WiseBanyan is eventually taken over in the event of a merger or takeover, a new owner may charger much higher fees. If you leave for another robo-advisor, there may also be tax consequences. On the positive side, WiseBanyan is not affiliated with any ETF sponsor and can thus invest in the “best-in-class” ETFs without conflict of interest. In the current group of robo-advisors, I would classify them as plucky underdogs.

I wouldn’t let a small sign-up incentive convince you to choose one robo-advisor over another, but new users can get a $20 bonus if they open an account with my referral link. Thanks if you use it.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

So how are they making money?

I’m almost scared to respond to this as Jonothan points out that we sometimes respond to questions ourselves!

We will be rolling out additional products and services on WiseBanyan in the coming months. They will be paid services that clients can opt into, but the diversified portfolio that Jonathon has written about will always be free.

“I’m almost scared to respond to this as Jonothan points out that we sometimes respond to questions ourselves!”

As a web developer who works for a startup, I’ve actually always appreciated working with “lean” companies who have founders and managers that take part in customer support and outreach. It’s important to me that everyone takes customer service seriously and truly cares about their product, not just a bunch of suits that think of customer support as an afterthought and are more interested in comparing business cards with the other executives than staying engaged and humbled. This is why I work with companies like Stripe over, say, PayPal.

Keep up the great work. I find that refreshing in the investment industry and for that reason, I’ve requested a spot with your site 🙂

David,

Thanks very much! I also feel the same way about other services in different industries. I really appreciate the thumbs up!

All the best,

Herbert

How is this different than just going through say vanguard themselves? Aren’t the only fees there the fund expense ration, or EFT expense?

Wisebanyan will auto rebalance.

A value proposition of most automated portfolio managers is that they will buy and rebalance for you. You send them $100, $1,000 whatever a month and they will buy and manage the portfolio for you. I prefer DIY investing myself but I still admit that rebalancing without emotion is much easier in theory than in practice.

You mention in the article that you have liquidated all your holdings in robo-advisors.

I assume that’s because, as you said, you prefer DIY investing yourself.

Is it mostly a desire to hand pick specific ETFs, funds, or other assets rather than use the ones selected by the robo-advisor?

Or is it more a desire to select your own allocation and make adjustments at different times?

I’m not sure what the smallest amount is that you can invest at Vanguard, but with WB, I think it’s only $10. At least that’s what I started with a long time ago. If you sign up with a referral link (like the one below), they give you $15 to start:

https://www.wisebanyan.com/referral/LipUgmOHu

Lets assume the following:

1. Investor wants to spend as little time as possible managing money.

2. Investor has to invest in a taxable account

3. Investor has somewhere between 100-5000 to invest monthly

4. Investments are currently in Vanguard target retirement funds.

5. No time horizon to use the money. It’s indefinite.

Would Wisebanyan be a good fit or something else?

Obviously I’m highly biased here, but the short answer is yes!

Our full automation means that you can simply “set it and forget it” – sit back while WiseBanyan takes care of the nitty gritty. The tax benefits of ETFs make them the right choice for a taxable account with a long time horizon, and we make sure to construct a portfolio that is tailored to your investment goals. The automation and our cost structure also bring a great deal of value: even entering 5 trades a month at $10 per trade to invest your contribution would be very costly over the long term for even mid sized accounts (think somewhere in the neighborhood of $500 per year). Finally, for a smaller contribution of say $100 per month our ability to offer fractional shares means that we can perfectly allocate your funds.

When are the trades made? How often do they rebalance? Do they use new deposits or dividends to rebalance rather than selling?

The trades are made 1-2 business days after your money arrives. I forget the rebalancing schedule right now as I am traveling and don’t have the opportunity to look it up. I am pretty sure they don’t instantly reinvest dividends, however. The dividends collect until the next investment date.

First off, great post, and thank you for being a WiseBanyan client!

We’ve made several new releases and now dividends are re-invested – because we use fractional shares, they are invested right down to the last penny. Efficiency 🙂

Prior to August 1 we re-invested any cash balances above $5.

Look like there is a wait list to join. I’m # 57xx on the list. Is there a way to join asap? Thanks Jonathan.

Danh, after five referrals of any kind who simply plug in an email address to similarly go on the wait list, you’re in.

Don’t believe I have ever seen any one of these advisory services/custodians consider REITS to be in the bond category. In fact just the opposite, as part of the equity portion. Which is as it should be with the volatility of stocks. Perhaps it can be considered in the “alts” category as REITS do not always move in unison with other stocks, but bonds…I think not.

For anyone considering there bond portfolio to be in “safer” investments, I find this quite interesting/questionable; especially here where it represents 20 percent of the “bond” portion of a portfolio.

Jonathan: Great review. I ran across your blog researching WiseBanyan and I added it to my favorites. I think I’m go to try WB out.

While everyone is positively positive, there are a few security concerns with this firm. I first received an from Folio Client that my email had changed. That’s weird because I don’t have an account with that company. And today, I see a withdraw from my bank account to Reich & Tang, no idea who that is either as I don’t do business with them either. Turns out they are both related to opening an account with Wisebanyan. Going over the welcome email, it does state these companies will do what happened. It is quite alarming to do business in this day and age when everyone is buying and selling your information for a new firm to farm out parts of their business to other firms and then watch as those firms start making financial transactions with little description back to their reasons to be using your information in the first place.

This all has left a foul taste in my mouth. I will probably close this account due to these tricks.

From what I was able to figure out WiseBanyan as expected uses a third party to hold the assets. Which is Folio and they ‘change emails’ to get authorization to access your Folio account that they created. Essentially Wisebanayn is just software that manages the assets in the Folio account. Which certainly has the advantage that your assets are in a account that is much more trusted than some random startup.

Shane, you are absolutely correct in that we use Folio Institutional to custody client assets. This is similar to the vast majority of investment advisors, and we do it for the safety of our clients. It is never a good idea to self custody assets, and indeed it is considered best practice to use an external custodian.

Michael, in regards to your specific questions about the emails from Folio: This happens when WiseBanyan’s system opens your brokerage account with Folio. We also provide you with instructions on how to login to your Folio account. Again, this is all for the security of the client – if you ever want to double check positions or trades, you can verify them directly on Folio’s site. Reich & Tang is a transfer agent that we and Folio use to process client additions and withdrawals. We try to proactively message our clients, and we are working diligently to have the transfers marked as “WiseBanyan” rather than “Reich & Tang.” It is worth noting that the vast majority of online advisors, brokers, and other asset managers use external funds transfer systems, although their name may displayed on the transfer confirmation. (Some so called money sending services even use other transfer agents) This mostly has to do with integration with broker dealers and regulations surrounding becoming a money transfer agent.

I am sorry to hear that this left a negative impression with you, and if you ever want a more detailed explanation of any part of this, please email us at support@wisebanyan.com. I am glad that you decided to give WiseBanyan a try!

All the best,

Herbert Moore

Co-founder & CEO, WiseBanyan

You idiots should say WiseBanyon when taking money out. I had money taken out of my checking account week ago and I had to contact my bank because I didn’t know what is “Reich Tang”

It is clear you did not carefully read the site and understand this would happen. It, as they say, is common in the industry. I use Fidelity cash management account because I choose not to use a physical bank because of my travels. They use UMB for their checking. Even though it is a Fidelity account, the monies are held in many financial institutions, eg. Wells Fargo, Sun Trust, Fifth Third…ACH’s to other institutions state UMB. There are some months I gain interest from 5-6 banks in the account. This does not make them “IDIOTS”. I understood this before I opened the account by doing my due diligence to understand what I was signing up for. I also understood that a withdrawal from Wisebanyan would say Reich Tang on the statement because they tell me this on their web site. Due diligence is everyone’s responsibility.

These are not at all “tricks”. As you admit yourself, they told you everything that would happen ahead of time. How can that make it a trick? Nearly all advisors use a third-party called a custodian to hold your money. You *want* that to happen. It’s actually *safer* that way for you than them holding it themselves.

Mostly, this is a result of Wisebanyan’s pricing model attracting clients that are not used to the industry and their standards. So perhaps WiseBanyan needs to be even more blunt and specific about communicating expectations (even though again they did tell you what was going to happen).

This raised security concerns to me that I think are well founded.

If a person has quite a few transactions, things like this jump out in your statements; as it did to me. I had to go back and recheck correspondence to verify who was doing what. I don’t necessarily think I’m the only one that would ever get confused by this process.

Here is a link to sign up with no wait (from me, a founding member):

https://www.wisebanyan.com/referral/LipUgmOHu

Hey Jon great post. Heard about this earlier today and was really thinking about going with it, Pretty young thinking about all of this investing stuff (only 23) so thanks for sharing your thoughts! Great blog!

Does WiseBanyan allow you to invest multiple “buckets” of funds at different risk ratios to align with different investment horizons?

You can create multiple accounts under a single login, and each has it’s own risk ratio. You can’t currently split one “Roth IRA” into multiple buckets, but perhaps you could open multiple Roth IRAs as long as the total contributions for the year were less than the annual total maximum. You can also change your risk ratio whenever you like.

My invite link to skip the wait list:

https://www.wisebanyan.com/referral/Dy0oi9j2R

I opened a Betterment account and used it for the free 2 month period, to compare it against WiseBanyan which I also opened around the same time. WiseBanyan did better in actual returns (and continues to grow better this year), I like their allocation and simplicity. WiseBanyan definitely feels more beta in their design and lack of iOS app, but I don’t have much to invest currently and I am comfortable growing my investments with them with minimal fuss and no fees. I will be interested to see how WiseBanyan keeps improving and how much they decide to charge for tax-loss harvesting (and if it makes any difference to me) or other extra services in the future. Then I may re-evaluate where to keep my investments.

To skip their waitlist, here is my referral for anyone interested https://wisebanyan.com?ref=tH92EW

The difference in returns is probably due to a more aggressive asset allocation. That cuts both ways. I wouldn’t put too much weight on a short period of outperformance by any robo-advisor.

Just signed up for my shiny new WiseBanyan account thanks to Jonathan’s referral link. I was surprised that the link had not been over used and still gave me access to an account.

I am a Vanguard user myself but one thing I find unique and useful with services like WiseBanyan and Acorns is the ability to buy fractional ETFs. This feature is not advertised as heavily as it should. As Jonathan said 1 share of VTI is upwards of $100 and you cannot start with $100 at Vanguard (or Schwab or Fidelity for that matter) This new wave of online investment options is invigorating. You might not become a millionaire using this (or you might) but this is definitely a good start. WiseBanyan’s no-fee schedule sounds much better than Acorns $1/month + 0.25%/year fee schedule. Definitely going to give it a try.

My link in case anybody wants to sign up:

https://www.wisebanyan.com/referral/QP24nv1Gx

Here is my link to skip the wait list:

https://www.wisebanyan.com/referral/w8x0isUnh

Here is another referral if anyone wants to use it – https://www.wisebanyan.com/referral/GNtGn8Vb7

Would be interesting to see a follow-up review here, one year later, as from my perspective this service has been a huge disappointment. WiseBanyan doesn’t provide its customers with proper tools for comparison, but I think their managers have vastly under-performed in comparison to the market, given the dramatic rise and minor fall over the past year. Such a review would also be instructive in terms of comparing the value gained from fee-free funds management, to the ultimately loss from poor funds management in comparison to high-tier, longer-established companies than WiseBanyan. (I write this as someone who put in just $10k as a test run, and it never made much more than a few hundred dollars; now I’m down by $500 at a net loss — and this after a catapulting year of gains.)

How much money did you put in and when? Depending on your start date, I’m not surprised at all with a net loss. Stock markets haven’t been too hot, especially international stocks which you don’t see as much coverage on CNN, CNBC, WSJ, etc.

I had written how much already in the comment you’re replying to. As to where, 54% stocks, 46% bonds. Again, the idea here is that they underperformed compared to other fund managers even at the very peak of the market (setting aside the recent downturn). Since your recommendation to try out WiseBanyan did inspire my test along with many others, it’s an organic follow-up to see whether WiseBanyan is actually a Wise choice in the long run.

Unless convinced otherwise, once my balance gets back to what I put in, I’m withdrawing from WiseBanyan and never looking back. Big disappointment. (As an aside, their customer service hardly exists; I’ve pointed out twice to them that there’s no contact link when you’re logged in; they’ve evaded thrice.)

I’m not really sure what you’re looking for. WiseBanyan isn’t picking the “good” funds over “bad” funds, their asset allocation is done with index fund and very similar to other robo-advisors. Compare with Vanguard LifeStrategy Moderate Growth Fund (VSMGX) which is 60% stocks and 40% bonds, the YTD return as of 9/28/15 is -4.3% and 1-year return is -1.39%. I don’t have your exact cashflow amount and corresponding dates, but putting your money there would have most likely lost you money too.

https://investor.vanguard.com/mutual-funds/lifestrategy/#/mini/overview/0914

I’m not here to convince you either way, but your criticisms other than customer service response just seem based on recent performance. I’m just pointing out that similar robos have had similar performance.

Simply put, when the market for stocks and bonds was at its peak, my WiseBanyan holdings barely broke even. I’ve already clarified twice that I’m not looking at recent performance. I doubt that every single so-called “robo-advisor” operates identically. Humans piece together combinations of assets.

Your 1st and 2nd sentences contradict each other. You’re looking for a robo that did better in the past year while “stocks and bonds were at their peak”. I’m sure there are some who did a little better. I’m afraid I can’t help you find them. I hope you find a service that works for you.

Misunderstood; put together with my prior comments, again I’m saying that after putting in $10k when the market was in bargain low territory, the account barely nudged up when the market peaked. Also again, so-called “robo-advisors” get programmed with algorithms.

As a quasi-journalist, I had thought you’d be intrigued (or feel a sense of responsibility) by possible flaws in WiseBanyan’s performance vis-a-vis fee-based managers. The defense is suspicious.

Algorithms? That’s not how they work. It’s just a basket of ETFs in set ratios, rebalanced periodically, as noted in the review above. Seriously, look in your account statement and tell me what trades they made that weren’t just keeping you in their stated asset allocation. Share screenshots of your transaction history, or send them to me, and I will look at them.

I get no benefit if you or a billion people sign up for WiseBanyan as I have no money invested in WiseBanyan; I concluded my test with them already. I’m not even recommending them over Betterment or Wealthfront or other competitors. I’m just confused by your claims and don’t want other readers to be confused by them. There is no secret sauce.

Here is an update on my WiseBanyan account. I started with the minimum opening balance and have deposited the minimum amount each month since Sept. 2015. I don’t know much about this stuff and didn’t want to lose any large sums of money. I’m happy to report so far it has had a return of over 5%. Its not perfect, but when there are no management fees it’s not bad. If your interested give it a try. Here is a link that will get you a free $15.00

https://www.wisebanyan.com/referral/mezZCqT54

Great review! I have been using WB to do taxable investment since the start of the year. It has a very clean interface and am up 3.0%. Things I love: 1. Ability to invest small dollar sums each month 2. Avoiding the higher $ threshold’s to get invested in mutual funds like the $3k minimums at Vanguard. 3. The clean interface that lets you know your rate of return. Things that could be done better – 1. Opting out of Bonds and REIT – I keep mine at the minimum percentage allowed. For tax efficiency, I’d rather have just stocks. 2. Quicker execution of trades. There is a two day turn around after funds leave your account. Overall, I am very happy with my experience with WiseBanyan. I hope that they are sustainable in the long run.

I’ve been depositing $100 per month and I have been impressed with the service provided. So far holding a 6.6% ROR, I know it will go up and down, but it being fee-free (minus the vanguard fund fees) really will allow the IRA to grow that much faster.

Get $15 when you sign up with Wise Banyan, a free robo investor. Check it out. 🙂 https://www.wisebanyan.com/referral/y5FUts0ff

Paul seems a bit testy but i do agree with the premise that these robo advisors underperform. I’ve had a significant amount of money with Betterment for about 2 years and the returns are abysmal compared to my other diy 4 ETF portfolios (bonds, staples, treasuries, and real estate).

When the market goes down the betterment portfolios fall faster than the s&p and when the go up they don’t go up by as much. And that’s at ratios of 60/40 and 70/30. They also don’t allocate any $ to real estate. The NAREIT index has virtually outperformed the market for 30 years.

I think that is ridiculous.

In the above example Wise Banyan allocates 6% to Real Estate…

Grabola,

Robo Advisors underperform whom? These aren’t active management strategies that are changing allocations in response to changes in the market. All Robo-Advisors just use a set allocation to various index funds.

The only way a robo advisor can underperform is if

A: They have higher fees than another strategy or

B: They have a different asset allocation.

If the answer is B, the problem isn’t the robo-advisor, but the asset allocation chosen. A lot of times a robo advisor will underperform the s&P 500 for example because it has exposure to less risky asset classes like bonds.

Really, by definition, since Wise Banyan has no fees, they will always perform exactly in line with their underlying indexes. (In contrast to active managers who charge fees to pick stocks.)

Here’s my referral link! https://wisebanyan.com/r/f8cwC1EHD

I see a lot of people here are saying the sign-up bonus is $15. Well, now, it is $20. And it’s very easy. Just open an account and fund it with as little as $1 and $0 auto-deposit and then in 2 weeks time you’ll get $20 added to your account. Keep your account open at least 6 months in order to keep the $20 bonus. Otherwise, WiseBanyan will withdraw it out if you try to close your account before the 6 months is over.

Here’s my link if you’d like to give it a shot: https://wisebanyan.com/r/jBxQls8pf

I think the biggest risk is that they won’t be around. The tax package feature (wiseharvesting) is appropriately priced at $240 a year (maximum!), but I am not sure what other premium features I would pay for, and do not know if they can survive on a maximum $240 a year per investor.

I wish that they had an ACATS transfer (to allow in-kind transfers) like Wealthfront has (wealthfront will then hold on to the transferred assets and only liquidate when there are tax losses to net against). However, Wealthfront comes with .25% fees for life, which makes that service come at a premium I don’t wish to pay.

If only Wisebanyan were Schwab, or had billions instead of millions under management. My biggest concern is that in 50 years they will no longer be in business and my wife will have to deal with the hassle of changing robo advisors!

I would like to add some thoughts on how Wisebanyan has changed in the last three years. I was lured with the “free” account. It was easy and performed well. But you get what you pay for. Wisebanyan has multiple premium services that put them in the same fee category, actually more, if you wanted the same services with a bigger player. Wiseharvesting add .25%. Fast Money add 2.50/mo (this one I cant wrap my head around who would be foolish enough to pay for). Portfolio Plus 2.50/mo. Now they actually started fund raising for themselves as well. You can give them 1-10/mo so they can donate 10% and keep the rest themselves. Or as they say “Spread the word”. The day I saw them asking for funding is the day I started transferring and closing my accounts with them. I moved to Wealthfront and with their first 15k managed free and amount of my portfolio over 15K at .25% I am paying less in fees than just having Wiseharvesting with Wisebanyan. All I can say is that for a company that advertising free they have a lot of potential fees and some don’t even make sense or really offer the client anything except the fees. Anyone knows for a company to be around they need to make money. Free cannot last. They added fees for their free ROTH IRA’s this year as well. I now believe that they are running out of venture capitalist money and are in the beginning stages of realizing their idea of free wont last. I don’t think you will see them around in a year or two. As I stated before, you can get the services the offer for less with other providers. They are not a bad company, their services worked average, their customer service was alright, but they will not ever make enough money to sustain themselves.